Cotton futures traded on both sides of the market but ultimately settled lower for the week.

Cotton Market Weekly June 7, 2024

Since last week’s close, July futures gave up 232 points, settling at 75.44 cents per pound.

The focus has started to shift to the December futures contract, which is the lead contract based on open interest. December futures settled at 73.60 cents per pound, 291 points lower than last week.

July futures dropped as low as 72.26 cents per pound but eventually found support on a slightly oversold market and speculators rolling positions forward. There are concerns that prices could continue to fall.

Daily volume traded remained relatively strong this week. Total open interest was increased by 2,548 contracts to 231,839.

Bales eligible for delivery against futures decreased by 4,302 bales, bringing total certificated stock to 129,146 bales.

The stock market had a strong week, with the NASDAQ and S&P 500 posting new highs.

The European Central Bank and the Bank of Canada lowered interest rates this week for the first time since 2019, becoming the first major central banks to cut interest rates.

Crude oil prices fell early in the week on news that OPEC would restore some production. Prices managed to recover some losses by the week’s end.

The U.S. ISM Manufacturing PMI was weaker than expected, registering at 48.7% and contracting for the second consecutive month.

U.S. employers added 272,000 jobs in May, an unexpectedly strong number given the concerns about high interest rates and the slowdown in consumer spending. However, the unemployment rate rose to 4.0% from 3.9%. Data out Wednesday from the BLS suggested payrolls might have grown at a much slower monthly pace on average last year than initially reported.

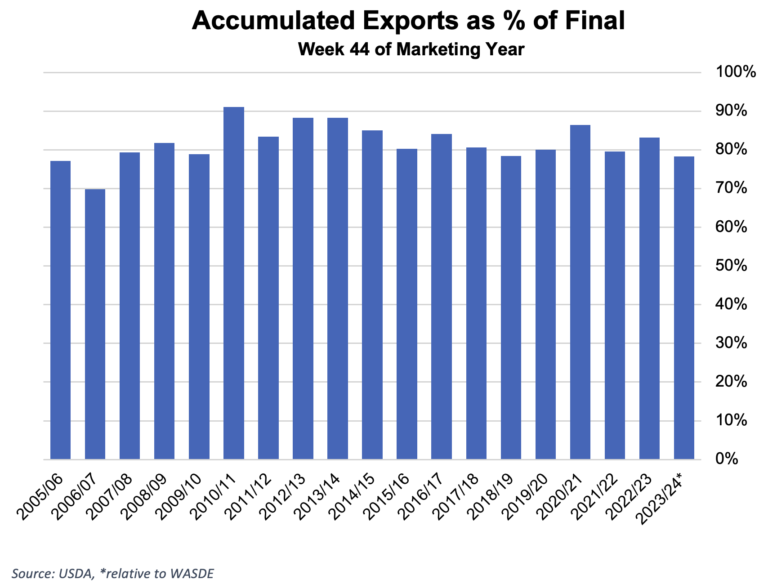

Despite decent export sales for the week ending May 30, shipments need to average 250,000 bales per week to reach USDA’s 12.3 million bale estimate.

Exporters sold a net total of 138,700 Upland bales for this crop year and 54,100 bales for the next marketing year, typical for this point in the year.

Shipments of 157,000 bales slowed significantly from recent weeks. Total exports are below normal for this point in the marketing year.

A net total of 2,000 Pima bales were sold, and an impressive 8,100 bales were shipped.

The Week Ahead

Next week, nothing matters more than the June 12 release of the World Agricultural Supply and Demand Estimates (WASDE) report.

The Goldman Sachs Commodity Index Roll has begun, and July options are expiring. Traders will be active as they exit their July positions and reestablish them in December. July First Notice Day is on June 24.

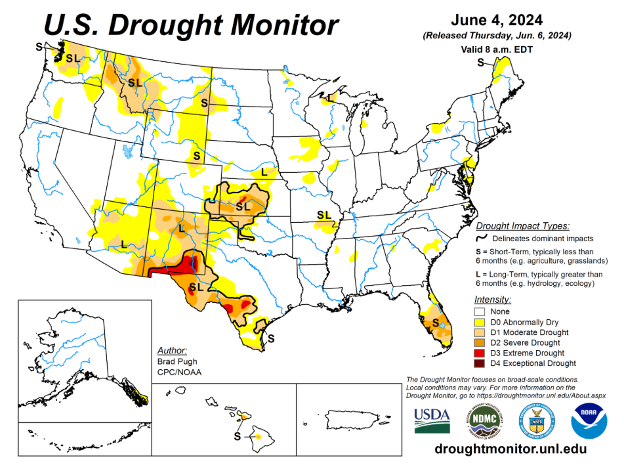

According to this week’s Crop Progress report, U.S. farmers have planted 70% of expected cotton acreage, and 9% is squaring. Precipitation concerns are building in parts of South Texas, and dryland planting is progressing rapidly in West Texas, Oklahoma, and Kansas.