September 24, 2021

- Open Interest Down 10,601 Contracts from Last Week

- Jobless Claims Higher Than Expected

- Net Upland Sales Total 345,400 Bales

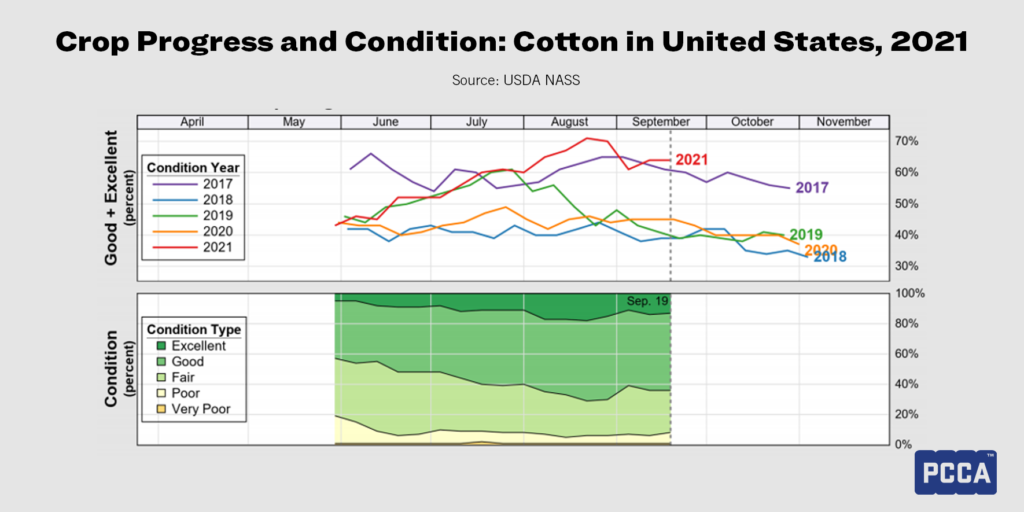

- Share of Crop in Good or Excellent Condition Higher Than the Last Four Years

It was a rollercoaster of a week. On Monday, December futures spiked down to 88.95 cents per pound, touching the lowest level since July 30. The sharp drop was driven by outside market forces which saw similar declines in all risk assets. Despite the worst single-day decline in months, futures were able to recoup losses over the next three days. By Thursday’s close, December had rallied back to 92.46 cents, down just five points for the week. Given Monday’s drop it is not surprising that average daily trading volume was high. Open interest also declined 8,727 contracts after Monday, showing that long liquidation was the central driver of the action that day. Open interest finished the week at 262,785, down 10,601 contracts from a week ago.

Outside Markets

Although stocks had already been trending lower for several days, an imminent default from Evergrande, one of China’s (and the world’s) largest property developers, seemed to be the straw that broke the camel’s back on Monday. Few risk assets avoided the panic selling as major indices touched their lowest levels in a few months. Prices seemed to stabilize on Tuesday as the company assured it could meet its bond payment today and the house of representatives moved forward a continuing resolution to prevent a Federal shutdown. The Federal Reserve’s decision to hold rates steady on Wednesday also cheered markets, although there is some trepidation surrounding potential acceleration of the tapering. There was some concern about tapering until higher-than-expected jobless claims came in Thursday morning, which seemed to convince investors that the Federal Reserve would not be so quick to draw down support. Major indices finished Thursday with gains for the week.

Export Sales

The Export Sales Report revealed that there was healthy demand in the week ending September 16. Net upland sales totaled 345,400 bales. Although China was once again the driving force with 219,800 bales, 17 other destinations were also buying both Upland and Pima. Turkey was the second largest destination (52,700 bales), and Pakistan was third (36,200). Pima sales totaled 23,500 bales with India ordering 16,000 of those. Combined shipments were 180,600 bales, which is more than average at this time of year. Price has not yet proved to be an impediment to new orders for cotton.

Crop Progress and Weather

As of last Sunday, U.S. crop conditions slipped slightly in the Southeast and Mid-South, but the share of the whole crop in “Good” or “Excellent” condition remains higher than at this time in the last four years. Unfortunately, increasingly unwanted rainfall has continued over much of the Delta and Southeast crop areas, and there could be some quality or yield loss in spots that received particularly heavy precipitation. Here in the Southwest, warmth and sunshine have helped to bring the crop up to speed. Sadly, places where prior rains had been “just enough” or “too little” have not suffered the heat as well. Dryland abandonment should still be low, but fewer are hoping for exceptionally high yields than were at the beginning of September.

The Week Ahead

While the eastern half of the Cotton Belt should mostly get a chance to dry out this week, traders will be keeping an eye on a hurricane that could potentially impact the United States in the second week from now. Weather in the Southwest is also getting some attention as there are increasing chances of rainfall over West Texas where rain is no longer helpful. Otherwise, traders will be looking at crop conditions on Monday, daily classing reports, and Thursday’s Export Sales Report to see if this week’s lower prices were able to drum up any business.

In the Week Ahead:

- Friday at 2:30 p.m. Central – Commitments of Traders

- Monday at 3:00 p.m. Central – Crop Progress and Condition

- Thursday at 7:30 a.m. Central – Export Sales Report

- Thursday at 2:30 p.m. Central – Cotton-On-Call