April 13, 2026

The Week Ahead

Peace talks between the U.S. and Iran didn’t go well, and crude oil is rising as a result. Markets are opening the week with a more cautious tone.

- Crude oil will continue to set the tone, with the news flow from the Middle East likely to drive short-term direction. Look for increased volatility ahead.

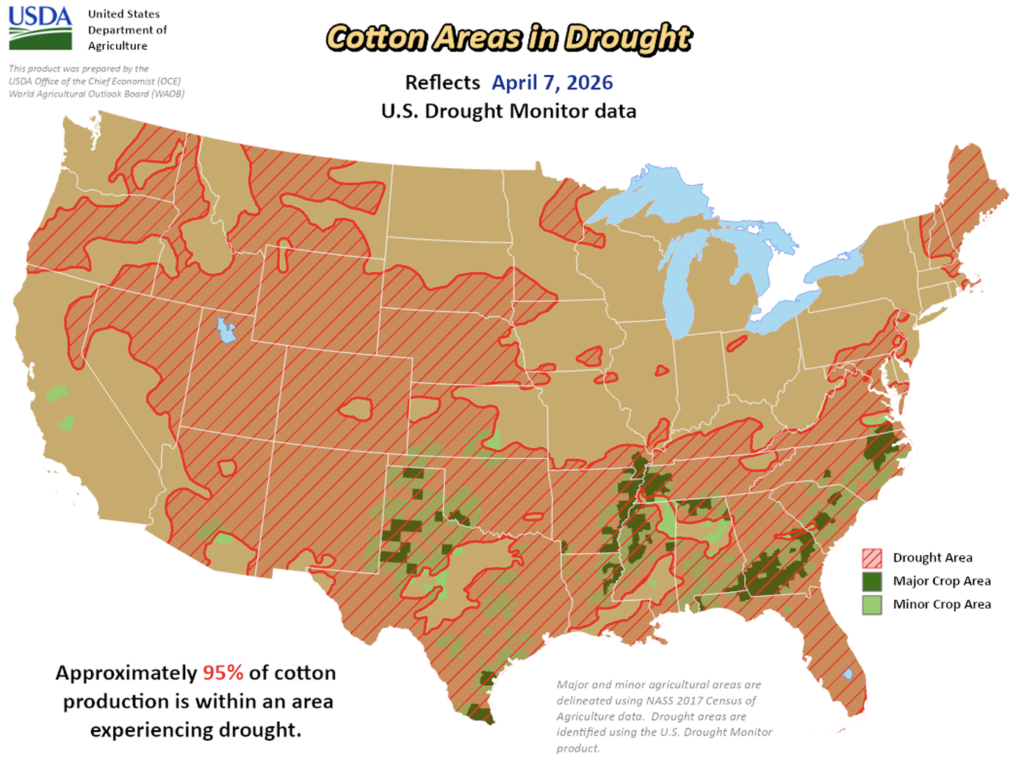

- On the cotton side, focus shifts back to the weekly export sales report, with underlying support tied to firm energy markets and seasonal strength. Rains over the weekend offered some relief across parts of the Southwest, but more will be needed as planting ramps up, especially with roughly 95% of the Cotton Belt still experiencing some level of drought.

- Looking ahead, direction in the cotton market will likely hinge more on macro developments and outside markets than any single data point, especially as commodity index roll flows begin to wind down and focus shifts toward planting progress and weather.

Market Recap

- Cotton futures trended higher through most of last week, with May pushing past 73 cents and marking another weekly gain as continued buying interest and supportive technicals carried the market higher.

- May futures settled at 73.22 cents per pound, up 230 points on the week. With July open interest overtaking May ahead of First Notice Day, focus now shifts to the July contract, which also posted a strong performance, settling 228 points higher at 75.33 cents per pound.

- Strength was underpinned by steady demand and improving positioning, though price action remained highly sensitive to outside markets. Shifting U.S.-Iran headlines drove moves in crude oil and broader risk sentiment. Technicals remain supportive, with trend-following buyers likely to step in on pullbacks. Any short-term selling is expected to be limited and to fade quickly. The April World Agricultural Supply and Demand Estimates (WASDE) came and went with limited impact and few meaningful changes, while May options expiration on Friday added to late-week activity.

- Trading activity was elevated throughout the week, driven by commodity index roll flows and May option expiration, which contributed to heavier volume and active spread trading. Positioning continued to improve, with the latest Commitments of Traders report reflecting ongoing buying interest and a continued move away from the heavy net short seen earlier this year, while on-call activity extended its trend of narrowing imbalances. Open interest increased marginally by 402 contracts to 340,990, and certificated stocks increased by 30,970 bales to 144,211.

Economic and Policy Outlook

- Geopolitical tensions ramped up over the weekend following failed U.S.-Iran talks, shifting the narrative back toward escalation and putting the Strait of Hormuz front and center.

- Macroeconomics felt the weight immediately, with higher energy prices adding to inflation concerns and creating a more cautious feel overall. For ag, the impact isn’t direct, but it shows up through higher input costs and more uncertainty around global trade flows.

- Inflation picked up in March, with CPI rising 0.9% month-over-month and 3.3% year-over-year, driven largely by higher energy costs tied to the ongoing Iran conflict. Core inflation remained more contained. February PCE data showed inflation was already firm heading into this, coming in at 0.4% on the month and 2.8% year-over-year. Consumer spending remains soft, with real spending up just 0.1% in February, signaling a bit of caution at retail. With higher fuel costs beginning to work through the system, demand shows early signs of slowing.

Supply and Demand Overview

- U.S. export sales softened slightly in the week ending April 2, with net upland sales totaling 319,600 bales, down from the previous week but still above the prior four-week average, led by Vietnam, Turkey, and Pakistan. New crop sales came in at 14,100 bales, with Costa Rica, Indonesia, and South Korea among the top buyers, while Pima sales were lighter at 6,500 bales.

- Shipments remained solid at 342,700 bales, just below the recent pace, with strong movement to Vietnam, China, and India, while Pima shipments improved to 10,600 bales. Looking ahead, shipments will still need to average just under 300,000 bales per week to reach USDA’s 12 million bale export estimate. Overall, it was a steady report, with demand holding together despite some week-over-week softness.

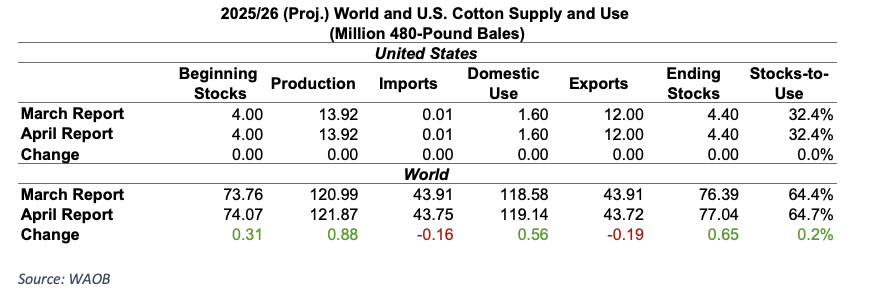

- The April supply and demand update offered little change on the U.S. side, with the balance sheet left unchanged. Globally, production was raised by nearly 900,000 bales, primarily in China, India, and Pakistan, while consumption also increased, led by stronger mill use in China and India. As a result, global ending stocks were revised modestly higher, pointing to a slightly looser balance sheet but not a major shift in the overall outlook.

- April is typically a quieter update, and that held true this month, with the market likely looking ahead to May when the first official look at the 2026/27 crop will be introduced and provide a clearer direction moving forward.

The Seam®

- As of Thursday afternoon, grower offers totaled 5,979 bales. The past week, 8,558 bales traded on the G2B platform received an average price of 68.70 cents per pound. The average loan redemption rate (LRR) was 53.90, bringing the average premium over the LRR to 14.80 cents per pound.

- Note: The Loan Redemption Rate (LRR) is the loan rate minus the current Loan Deficiency Payment (LDP).