October 6, 2025

The Week Ahead

- The government shutdown has now stretched into a week with no clear end in sight, delaying key USDA reports and leaving cotton and other ag markets without their usual data signals. In the meantime, traders are watching harvest progress, export competition, and seasonal strength for direction. While past shutdowns haven’t always weighed on markets, the lack of fresh data adds a layer of uncertainty. With Fed minutes due this week and more rate cuts expected before year-end, macro momentum could keep a floor under risk assets, but volatility may build until Washington resolves the stalemate.

- In addition to cotton’s weekly reports being delayed, the supply and demand update expected this week will also be postponed by the shutdown. Meanwhile, the Marketing Assistance Loan will remain unavailable until the impasse is resolved.

Market Recap

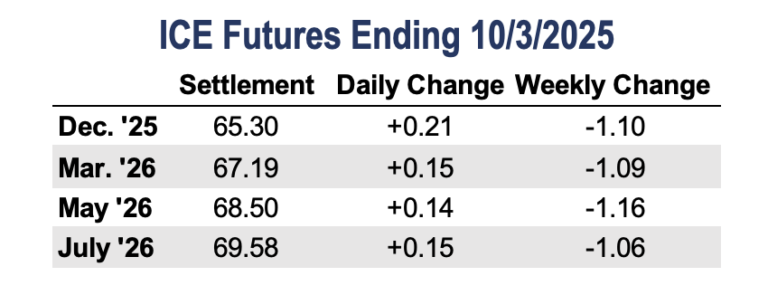

- The government shutdown added pressure on cotton futures this week, with December down 110 points to settle at 65.30 cents. Futures briefly slipped through support near 65 cents before finding some lift from fixation buying and short covering. Specs remain a key driver on the short side, though positioning has been harder to gauge since there was no Commitments of Traders (COT) report due to the shutdown. Rising certified stocks added to the weight, while harvest progress and outside markets offered little fresh direction. The technicals still lean bearish, but seasonal strength and bits of new business helped keep the market from breaking down further.

- Trading volumes were active alongside the technical breakdown, with open interest rising 5,436 contracts to 277,365. Certificated stocks also increased, up 2,749 to 17,891 bales.

Economic and Policy Outlook

- With the government shutdown, traders missed several key data points last week, including the jobs report on Friday, and the same looks true for this week. That has left markets relying more on headlines and outside signals. Oil grabbed attention with a sharp weekly decline on oversupply concerns, followed by a modest rebound after OPEC+ announced a smaller-than-expected production increase. Cotton’s direct correlation to energy prices is relatively small, though swings in crude can shape broader commodity sentiment. Higher oil prices can also lend indirect support to cotton by making manmade fibers more expensive. Crude is still well below past highs, but it remains a factor worth watching.

- There is talk that an aid package for farmers, potentially between $10-$14 billion, could be announced as soon as this week, though the rollout is unlikely to be immediate. With all the attention on soybeans, they seem certain to be included, but farm groups and lawmakers are pushing to widen the scope to cotton and other row crops. If the package is narrower or delayed, producers across multiple commodities may still face export-driven losses in the near term. Even if announced, the support may fall short of offsetting the broader financial strain, leaving uncertainty elevated across agriculture.

Weather and Crop Watch

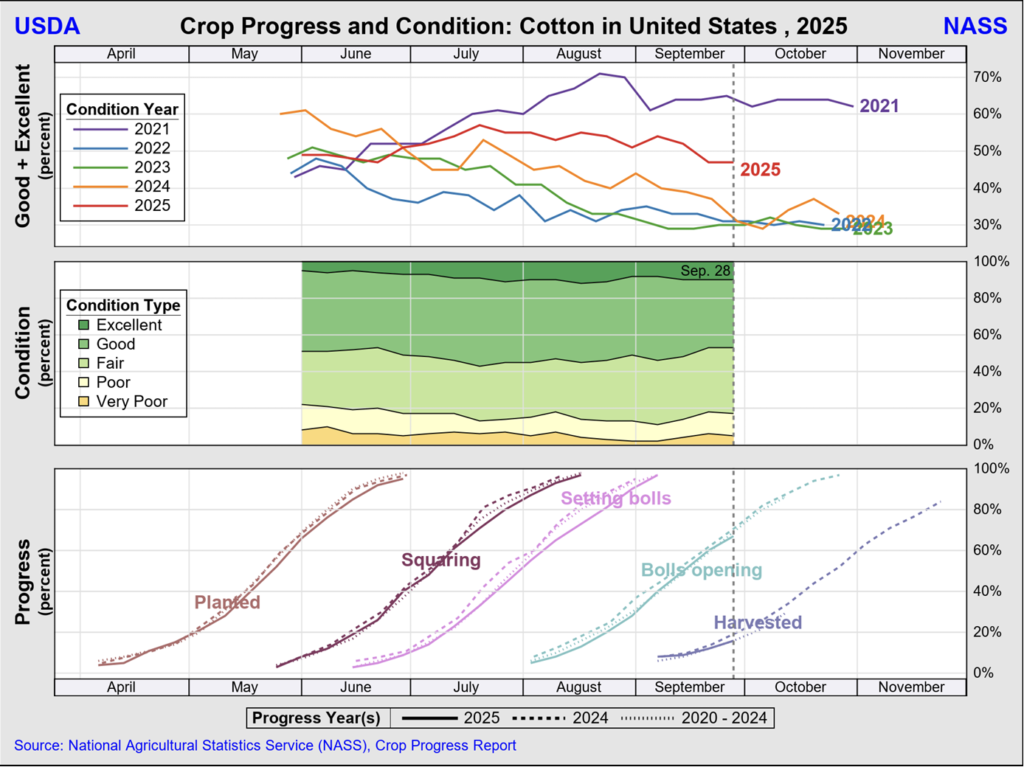

- Southwest crop conditions remain mostly favorable. For the week ending September 28, Oklahoma was the only state to see improvement, rising to 71% good to excellent, while Texas held at 41% and Kansas slipped to 50%. Boll opening has advanced to 57% in Texas, 70% in Oklahoma, and 26% in Kansas. Harvest is winding down in South Texas, bringing the statewide total to 26%. Although no updated Crop Progress and Condition Report will be released this week, harvest is underway in West Texas and Oklahoma, with Kansas not far behind.

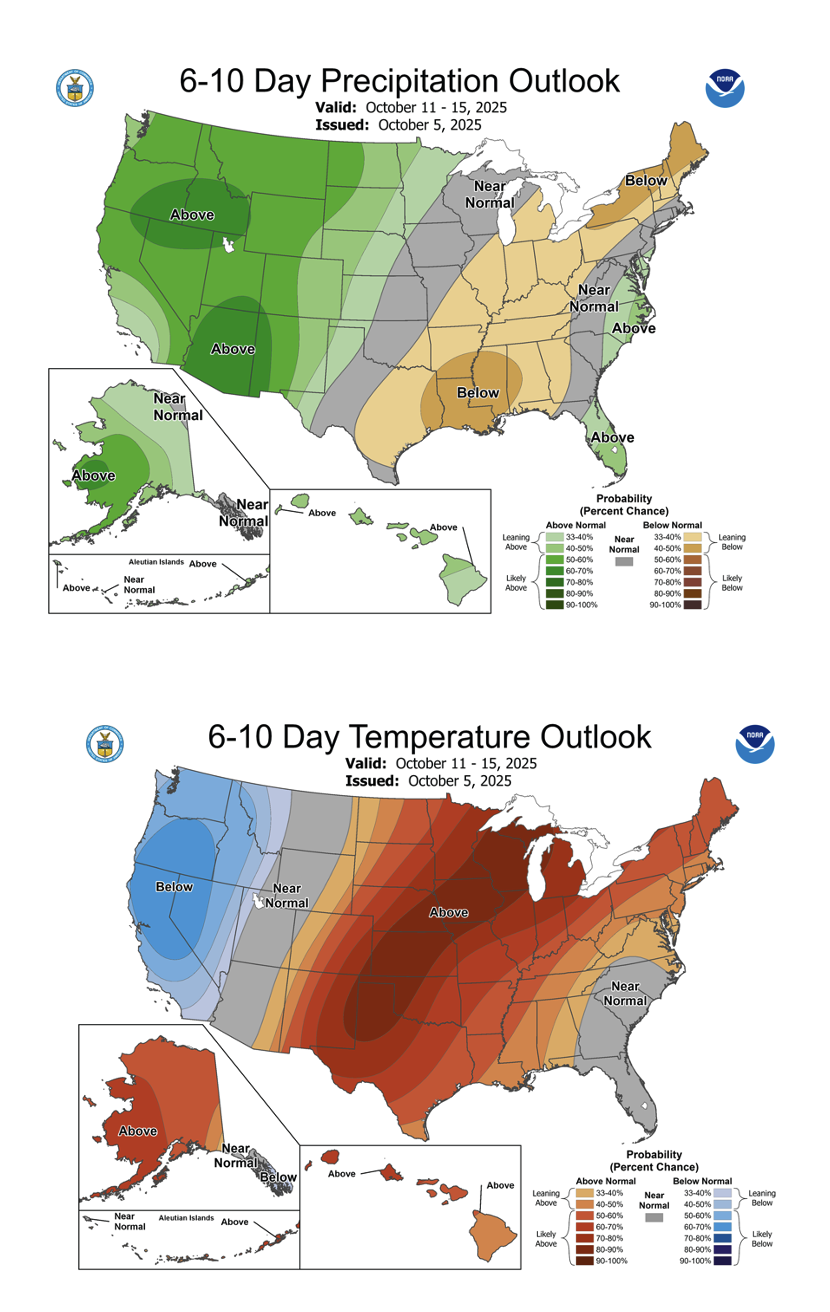

- Warm, mostly dry weather supported crop maturation and harvest progress across the Southern Plains over the weekend, with only spotty showers in a few areas. Forecasts suggest conditions will stay largely favorable, though occasional rainfall may bring brief interruptions. In South Texas, harvest is nearly complete, with most fields cleared and gins finishing out remaining modules and bales. While scattered showers caused minor delays, the bigger focus now is on soil moisture recovery, as much of the region remains abnormally dry even as the Valley shows drought-free conditions.

The Seam

- As of Thursday afternoon, grower offers totaled 27,911 bales. There were 3,552 bales that traded on the G2B platform that received an average price of 62.57 cents per pound. The average loan for these bales was 55.71, bringing the average premium received to 6.86 cents per pound.