November 8, 2024

Cotton futures found support amid a week of significant market-moving events, including the U.S. presidential election and the Fed’s interest rate cut. The World Agricultural Supply and Demand Estimates (WASDE) Report was on par with expectations, and export sales and shipments remained steady. How have these events influenced the market? Get QuickTake’s read on the week’s events in five minutes.

- After a week full of fluctuations, front-month futures eventually settled 148 points higher at 71.05 cents per pound.

- This week saw a flurry of activity in the cotton market. Key events such as the presidential election, the expiration of December options, the Federal Reserve’s interest rate decision, the rolling of the Goldman Sachs Commodity Index Fund (GSCI), and the November WASDE did not fail to provide the market with news. Ultimately, strength in broader markets and solid export sales supported cotton, helping futures prices close higher for the week.

- Rain and cooler weather hindered the advancement of harvest. The rain is welcome for the soil but could impact the quality of the cotton still in the field.

- Daily volume traded increased compared to prior weeks. Contracts were steadily added to open interest, boosting the total number of open contracts by 3,191 to 269,352.

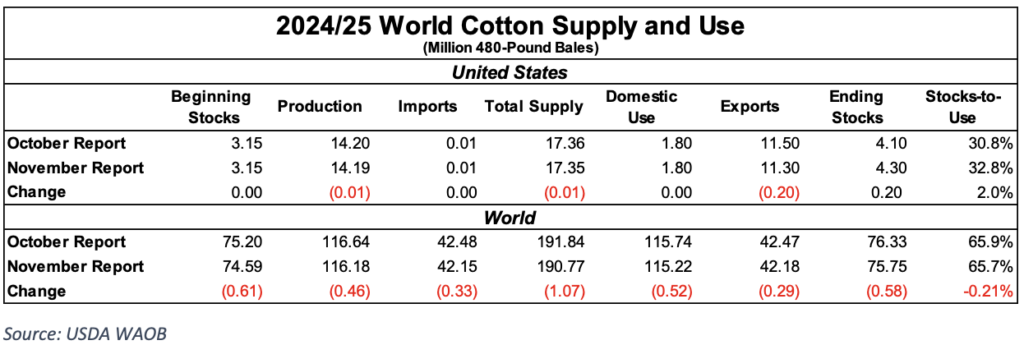

The November World Agricultural Supply and Demand Estimates (WASDE) Report came in as expected.

- U.S. production was lowered 10,000 bales to 14.19 million bales, while exports were lowered 200,000 bales to 11.3 million bales.

- U.S. ending stocks increased 200,000 bales to 4.3 million bales, raising the Stocks-to-Use ratio to 32.8%.

- Total Texas production was revised down by 205,000 bales to 4.24 million bales. Oklahoma’s production increased by 10,000 bales to 300,000 bales, while Kansas production remained unchanged at 190,000 bales, bringing total Southwest production to 4.73 million bales.

- Meanwhile, the crop in the Mid-South and Southeast fared better than initially expected following the hurricane, with a combined increase of 220,000 bales, offsetting the decline in the Southwest.

- Global consumption was revised down by 520,000 bales to 115.22 million bales, while ending stocks were reduced by 580,000 bales to 75.75 million bales. No significant changes were reported from importing or competing countries.

The stock market had its biggest post-election rally after Tuesday’s presidential election.

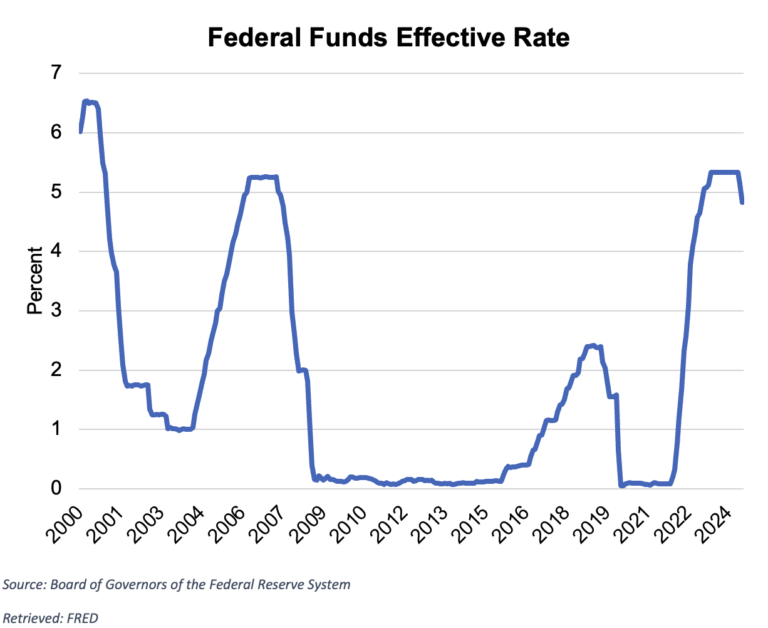

- It was a big week for markets, between the 2024 U.S. election and the Federal Open Market Committee (FOMC) meeting.

- All eyes were on Tuesday’s election day. Donald Trump was elected as the next president of the U.S., Republicans took control of the Senate, and it appears will also keep control of the House of Representatives.

- Federal Reserve officials cut interest rates by 25 basis points, bringing the benchmark target range to 4.5%–4.75%, marking the second consecutive reduction. Chairman Powell signaled that additional easing could be expected.

- The Bank of England also cut interest rates and forecast that inflation will fall to its target by early 2027. However, uncertainty surrounding the new U.S. president-elect was noted, as it could alter the global economic outlook.

- China announced a five-year stimulus package totaling 10 trillion yuan to help local government debt problems, which is equivalent to $1.4 trillion USD. Investors had anticipated more consumer support and were disappointed by the announcement.

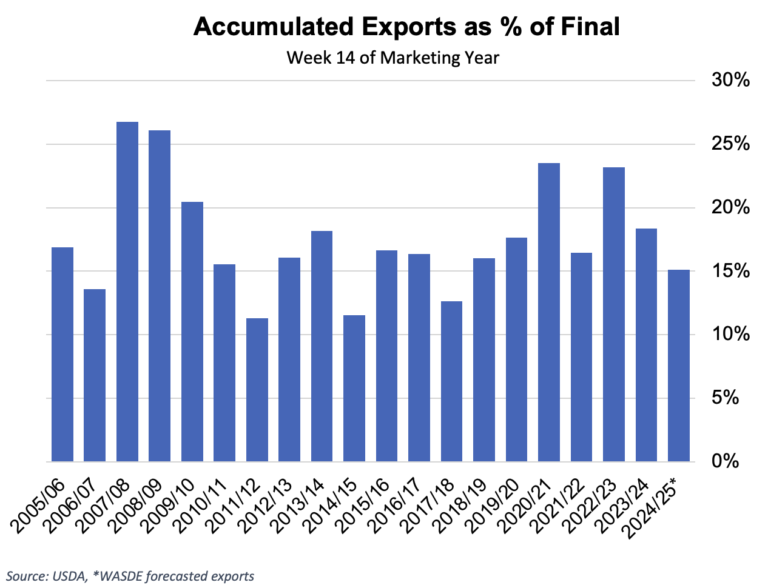

Respectable export sales and shipments were reported for the week ending October 31.

- For the 2024/25 marketing year, 229,000 Upland bales were sold.

- Inquiries into U.S. cotton have remained steady over the past week; however, mill demand still seems to be hand-to-mouth.

- A total of 145,800 Upland bales were exported during the week. Shipments have steadily increased each week, although they remain close to the average.

- Solid sales and shipments of U.S. Pima cotton were reported for the week. Pima merchandisers sold 12,300 bales and exported 7,500 bales.

The Week Ahead

- Next week should be a little quieter news-wise. We will get more inflation data as the Consumer Price Index (CPI) and Producer Price Index (PPI) will be reported on Wednesday and Thursday.

- Due to Veterans Day, the Export Sales Report will be delayed until Friday, but markets will be open.

The Seam

As of Thursday afternoon, grower offers totaled 54,727 bales. There were 9,075 bales that traded on G2B platform with an average price of 68.28 cents per lb. The average loan was 53.93 which resulted in a premium of 14.35 cents per lb. over the loan.