December 6, 2024

Activity in the cotton market was subdued following the Thanksgiving holiday, while global events and economic reports kept the stock market elevated. With data-heavy days ahead, how will these developments affect cotton prices in the coming weeks? Get QuickTake’s read on the week’s events in five minutes.

Cotton futures were range-bound after the holiday-shortened trade week.

- Due to the Thanksgiving holiday last week, the weekly change in price and total open interest will be calculated based on the close of Wednesday, November 27.

- The March contract closed at 71.10 cents per pound, down 65 points for the week.

- This week’s news in the cotton market was lackluster. Futures prices were range-bound, and the daily volume traded was modest.

- Total open interest increased by 1,487 contracts, bringing the overall open interest to 233,210.

- Certificated stocks remain unchanged at 13,274 bales.

Stock markets ended November on a high and continued to climb to new records, starting December off strong.

- Markets remained strong this week despite challenges overseas. Politically, South Korea’s president may face impeachment after briefly enacting martial law, while France’s prime minister was ousted following a no-confidence vote.

- ISM manufacturing prices paid were expected to be 55 but were reported at 50.3, a pleasant surprise for markets and a signal of minimal inflation.

- Fed Chairman Powell commented that the economy looks stronger now, allowing the Fed to take a more cautious approach to interest rates. Markets are pricing in nearly a 75% chance of a rate cut at the next Federal Open Market Committee (FOMC) meeting on December 17-18.

- OPEC+ delayed plans to increase oil output until April, as crude oil prices have been struggling recently. The group is concerned that higher production amid weak demand would put additional pressure on prices.

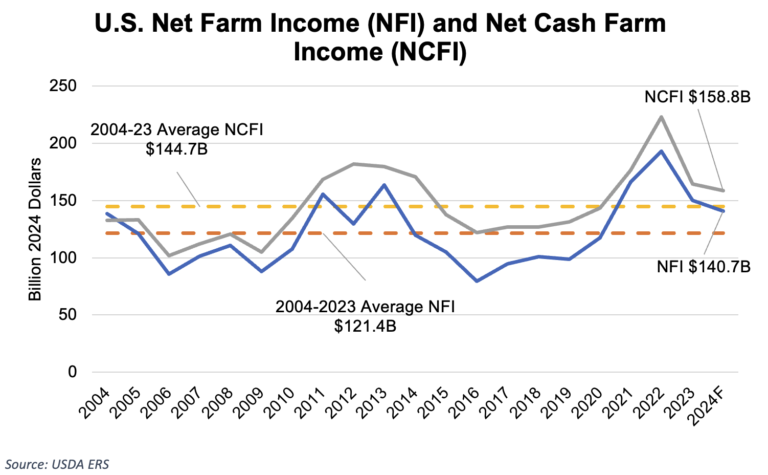

- This week, USDA released an update on net farm income, forecasting a decline compared to last year. Net cash farm income is forecast at $158.8 billion, and net farm income is forecast at $144.7 billion. The decline is primarily due to lower cash receipts from commodities.

- The U.S. added 227,000 jobs in November, slightly surpassing analysts’ expectations. However, the unemployment rate increased to 4.2%.

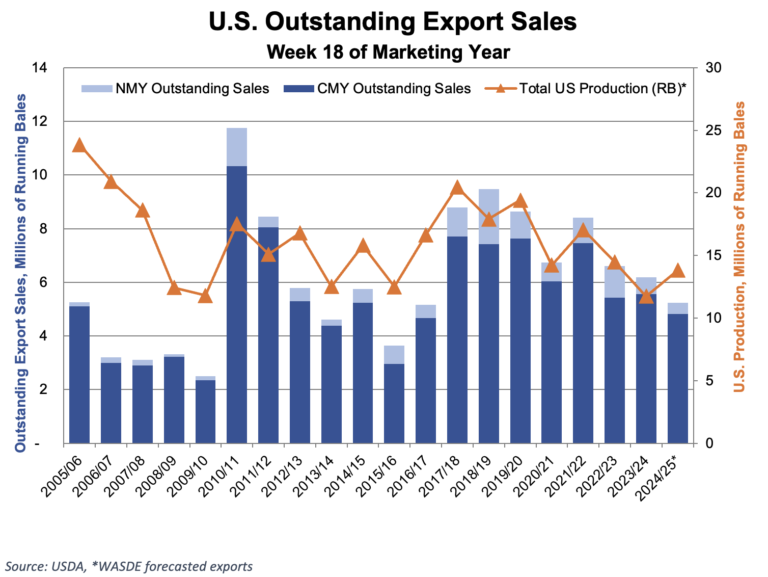

The U.S. export sales report for the week ending November 28 met lower expectations, with sales and shipments falling below average.

- For the 2024/25 marketing year, U.S. merchants sold 170,700 Upland bales and shipped 157,500 bales. Shipments need to average close to 250,000 bales per week, meaning they are still far behind the pace required to meet the USDA’s forecast of 11.3 million bales.

- Expectations of sales were lower this week, given that much of the business done at the Cotton USA Sourcing Summit has already been reported.

- Pima merchandisers sold 3,700 bales and exported 5,700 bales.

The Week Ahead

- Next week will be data-heavy for markets. For cotton, the most important event will be the release of the World Agricultural Supply and Demand Estimates (WASDE) Report, scheduled for Tuesday, December 8, at 11 A.M. CST.

- In addition, the November Consumer Price Index (CPI) and Producer Price Index (PPI) will be reported on Wednesday and Thursday, respectively.

The Seam

As of Thursday afternoon, grower offers totaled 116,605 bales. There were 19,299 bales that traded on G2B platform with an average price of 67.37 cents per lb. The average loan was 52.49 which resulted in a premium of 14.88 cents per lb. over the loan.