December 13, 2024

Cotton futures remained rangebound this week due to a lackluster WASDE report and ongoing weak demand. Inflation data has led investors to expect a 25-basis point interest rate cut at next week’s Fed meeting. With another data-heavy week ahead, how will these factors affect cotton prices? Get QuickTake’s read on the week’s events in five minutes.

March futures remained rangebound on weak demand and a WASDE report that failed to generate much excitement.

- The March contract closed at 70.09 cents per pound, down 101 points for the week.

- Cotton futures traded sideways throughout the week. Prices weakened heading into the weekend, likely due to a combination of technical and grower selling. A brief price boost followed China’s announcement about increased stimulus in 2025, but the details were vague. The WASDE report released on Tuesday failed to generate much excitement, reiterating what we already know: there is an oversupply of cotton worldwide and insufficient demand to consume it.

- Lawmakers are working on a deal to secure much-needed economic assistance attached to a 2018 Farm Bill extension. A full reauthorization is not expected until next year when Republicans will have the trifecta.

- Open interest increased by 1,374 contracts, bringing total open interest to 234,584.

- Certificated stocks increased 6,839 bales to 13,274 bales.

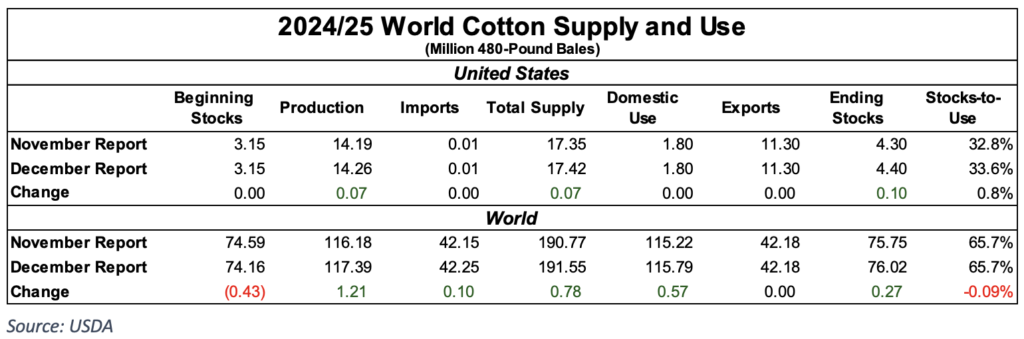

The December World Agricultural Supply and Demand Estimates (WASDE) Report indicated a larger U.S. crop and higher ending stocks.

- U.S. production increased by 70,000 bales to reach 14.26 million bales, while exports remained unchanged at 11.3 million bales. The higher production led to a 100,000-bale rise in ending stocks, bringing the total to 4.4 million bales. This caused the stocks-to-use ratio to increase from 32.8% to 33.6%, resulting in an overall looser U.S. balance sheet.

- The global side of the balance sheet saw a few notable changes, but overall sentiment regarding supply and demand remained unchanged. Production increased by 1.21 million bales, reaching 117.39 million bales, while consumption rose by 570,000 bales to 115.79 million bales. Ending stocks grew by 270,000 bales to 76.02 million bales, bringing the stocks-to-use ratio to 65.7%.

- The most significant change came from India, which saw a one million bale increase in production and a 500,000 bale increase in consumption, accounting for the majority of revisions to the global balance sheet. Imports from Pakistan and Vietnam also increased, though Chinese imports decreased.

- Despite an overall increase in the U.S. crop, production in the Southwest was lower. Texas production decreased by 300,000 to 3.9 million bales, Oklahoma fell by 10,000 bales to 290,000 bales, and Kansas remained unchanged at 190,000 bales. Additionally, the Texas Pima crop increased by 11,000 bales, bringing the total to 51,000. Overall, Southwest production is now expected to reach 4.431 million bales, down 299,000 bales from the November estimate.

Stock markets were mixed for the week, with the Dow edging lower while the NASDAQ set new records.

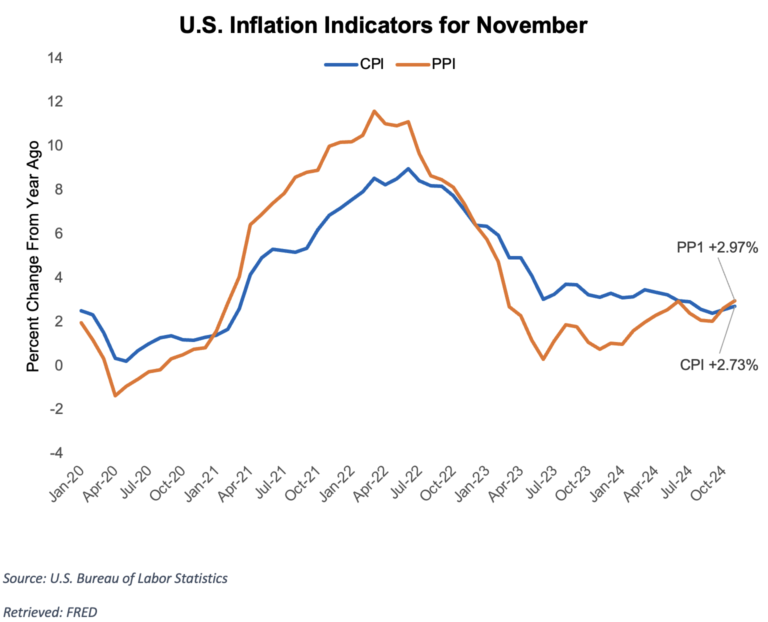

- The November U.S. Consumer Price Index (CPI) was reported in line with expectations, rising 0.3% month-over-month and 2.7% year-over-year.

- The November Producer Price Index (PPI) was slightly hotter than expected, rising 0.4% month over month and 3.0% year over year.

- Despite the stronger inflation data, markets have priced in another 25-basis point cut to interest rates at next week’s Fed meeting on December 17 and 18. Inflation has not decreased as much as expected, and the labor market remains relatively strong, so the outlook and timing for rate cuts in 2025 remains uncertain.

- Crude oil prices rebounded this week due to China’s stimulus measures and potentially stricter U.S. sanctions on Russian oil, which could reduce global supply. However, a report from the International Energy Agency on Thursday projected a global oil surplus next year, halting crude’s advance.

- The U.S. Dollar remained strong, bolstered by global interest rate cuts, including the European Central Bank’s third consecutive rate reduction. This has also weighed on commodity prices, as a stronger dollar makes U.S. goods more expensive for other countries to import.

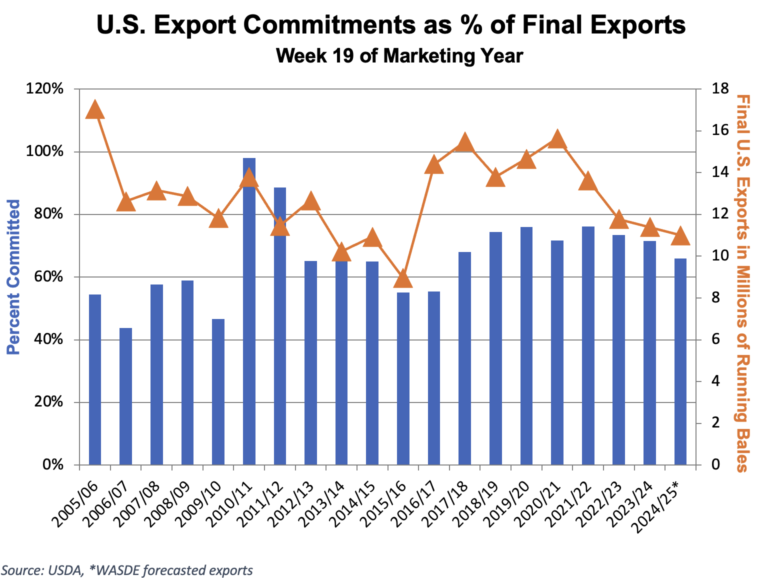

The U.S. Export Sales Report continued the previous trend, indicating steady sales along with below-average shipments.

- For the 2024/25 marketing year, U.S. merchants sold 153,000 Upland bales and shipped 157,500 bales.

- Demand for U.S. cotton has been subdued this marketing year, and shipments have also been disappointing. To meet the USDA’s forecast of 11.3 million bales, shipments need to average nearly 250,000 bales per week, meaning they are still far behind the required pace.

- Pima merchandisers sold 6,900 bales and exported 6,500 bales.

The Week Ahead

- Next week will be data-heavy for markets, with reports on retail sales, Gross Domestic Product (GDP), and personal income. Despite a bleak outlook, the cotton market will continue to monitor the weekly Export Sales Report and updates from the classing offices.

- Lastly, the Federal Open Market Committee (FOMC) will meet on December 17-18 and announce its interest rate decision on the 18th.

The Seam

As of Thursday afternoon, grower offers totaled 165,487 bales. There were 16,265 bales that traded on G2B platform with an average price of 62.52 cents per lb. The average loan was 48.74, which resulted in a premium of 13.78 cents per lb. over the loan.