December 20, 2024

Bearish sentiment persisted in the cotton market as March futures hit a lifetime low. Stock markets were mixed following the Fed’s interest rate cut and reports of strong economic growth. How will markets respond to these unfolding events and a potential government shutdown in the week ahead? Get QuickTake’s read on the week’s events in five minutes.

March futures trended lower on a weak technical outlook and poor fundamentals.

- The March contract closed at 67.91 cents per pound, down 218 points for the week.

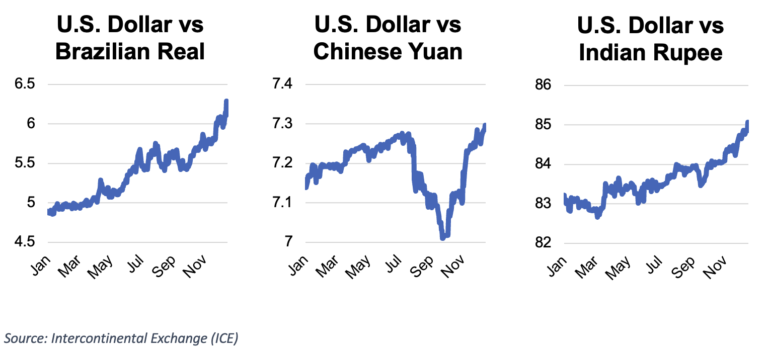

- March futures hit a contract low this week. A weak technical outlook has weighed on the market. Outside of that, there has been little new information to give the market direction. Recently, the strength of the U.S. dollar has become the biggest headwind for U.S. cotton, exacerbating already weak demand. The dollar is strong against the Brazilian Real, Chinese Yuan, and Indian Rupee—currencies that either compete with U.S. cotton or belong to major importers of U.S. cotton.

- It has been a chaotic week on the government front as we brace for a potential shutdown. Despite numerous attempts, lawmakers have failed to pass a bill that would fund the government for the short term. Without action today, government funding will expire at midnight. Producers and merchants are watching closely as this will impact CCC loan entries and redemptions.

- Open interest increased by 8,658 contracts, bringing total open interest to 243,242.

- Certificated stocks increased 6,839 bales to 20,113 bales.

Stock markets sold off after Fed Chairman Jerome Powell made hawkish remarks about the economic outlook following the announcement of an interest rate cut.

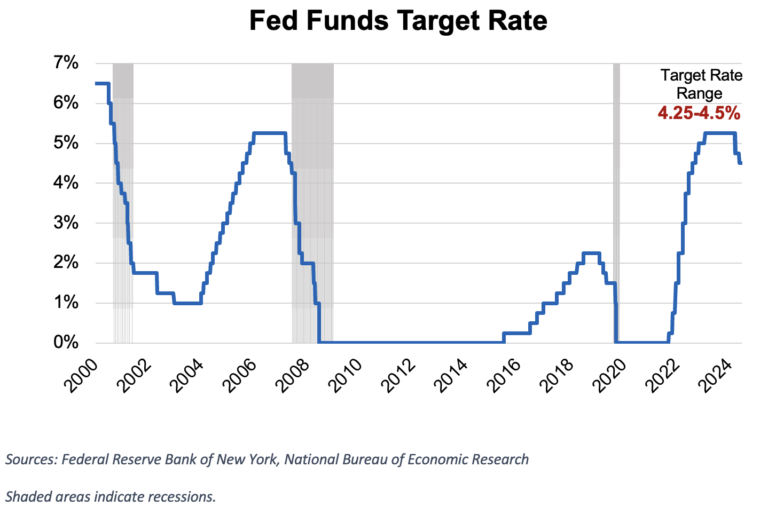

- The Federal Open Market Committee (FOMC) met this week and announced a 25-basis-point interest rate cut, lowering short-term rates to a range of 4.25% to 4.5%.

- The Dow Jones Industrial Average finished lower for ten consecutive sessions, the longest losing streak since 1974.

- At the press conference following the announcement, Fed Chairman Jerome Powell indicated that the Fed would be slow to implement further rate cuts in 2025, suggesting there could be just two. He cited ongoing inflation concerns and uncertainty about the challenges the new administration might bring. As a result, we are returning to a ‘higher for longer’ stance on interest rates.

- U.S. retail sales in November exceeded expectations, rising 0.7% month-over-month and 3.8% year-over-year. Sales of clothing and accessories were down 0.2% month-over-month but increased by 2.2% compared to the previous year.

- The U.S. Gross Domestic Product (GDP) increased by 3.1% in the third quarter, surpassing the expected 2.8% and exceeding the 3.0% growth in the second quarter.

- The U.S. Dollar reached a 52-week high, rallying on the news of fewer-than-expected rate cuts in 2025 and that the Bank of England and Bank of Japan kept interest rates steady following the U.S. rate cut. Commodities struggle when the dollar is strong, as it makes it expensive for other countries to import goods.

The U.S. Export Sales Report showed strong sales figures but weak shipments. Given the current conditions, demand for U.S. cotton remains solid with the lower prices, but exporting cotton has been challenging.

- For the 2024/25 marketing year, U.S. merchants sold 194,900 Upland bales and shipped 128,600 bales.

- From a sales perspective, the U.S. is currently ahead of the pace needed to reach the USDA’s estimated 11.3 million bales. Merchandisers need to sell approximately 145,000 bales per week to get there. However, shipments are significantly behind the pace, and 250,000 bales per week must be shipped to meet the estimate.

- Pima merchandisers sold just 500 bales, a marketing year low, but exported 12,000 bales. Shipments are on pace to reach USDA’s estimate.

The Week Ahead

- Next week’s trading schedule will be adjusted due to the Christmas holiday on Wednesday, December 25. On December 24, the market will close early at 12:05 p.m. CST. The market will be closed on December 25 and reopen on December 26 at 6:30 a.m. CST, resuming regular hours for the remainder of the day.

- Should a government shutdown occur, the release of standard government reports will be postponed until the government reopens. However, should one be avoided, reports such as the Export Sales Report, Cotton On-Call Report, and Commitments of Traders Report will have a delayed release due to the holidays.

The Seam

As of Thursday afternoon, grower offers totaled 178,525 bales. There were 18,472 bales that traded on the G2B platform with an average price of 61.74 cents per lb. The average loan was 48.90, resulting in a premium of 12.84 cents per lb. over the loan.