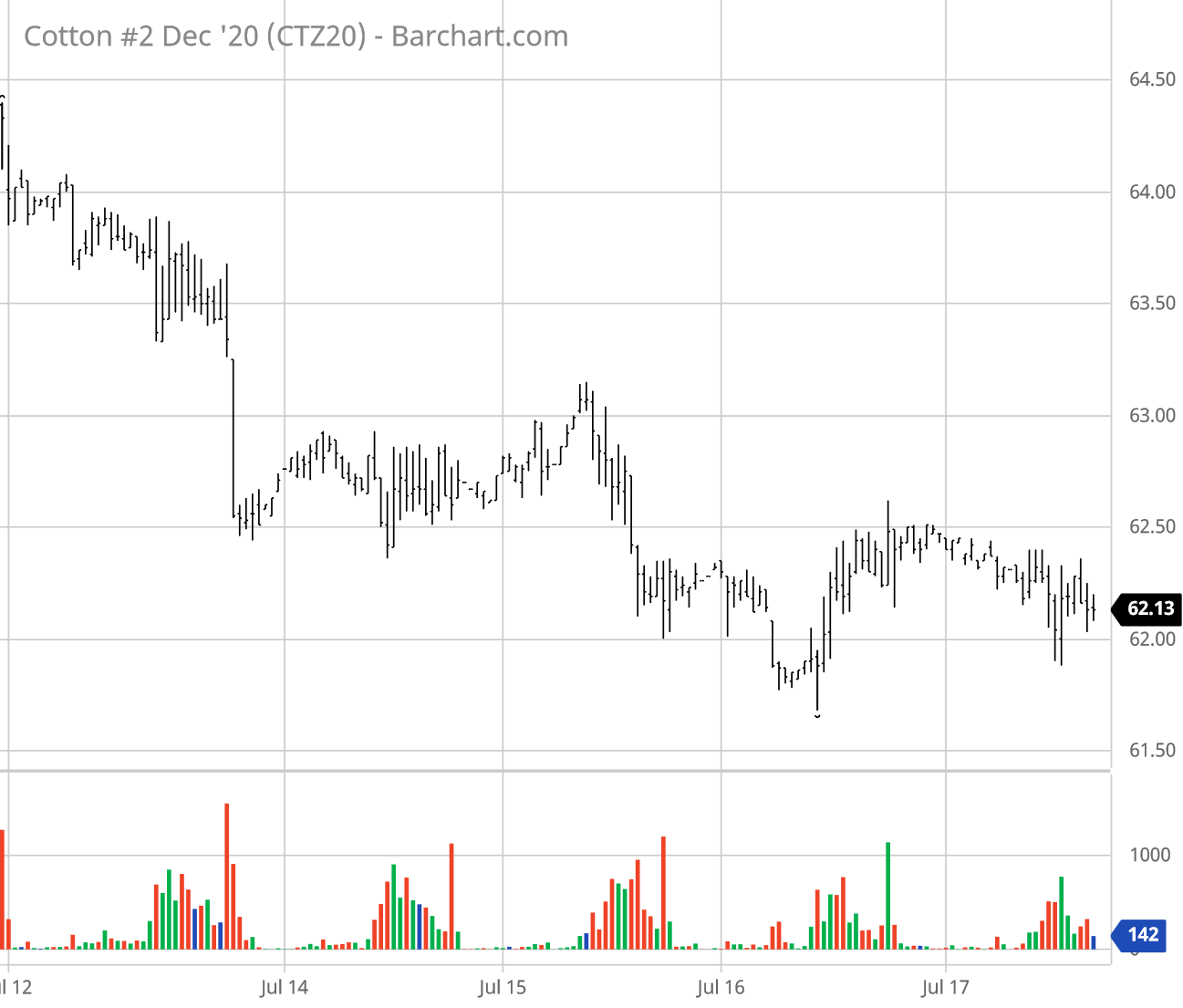

The week ending July 17 saw most active ICE cotton futures take several stair-steps lower from the recent highs to the 62-cent range (see graph above courtesy of Barchart.com). Chinese cotton prices were mixed this week while world cash prices trended lower.

Fundamental influences this week included continued heat/dryness in the Southern Plains. Thursday saw weak old crop (not unusual) and weak new crop (not good) U.S. export sales. Actual export shipments remained on trac. Certified stocks continued to decline from the peak earlier in July. Commercial demand remains reportedly slow outside of a handful of buyers in China and Vietnam.

The week saw continued low volume trading of ICE cotton futures, with a static pattern of open interest. Speculative short covering and new buying continues to be reflected in the Commitment of Traders data.

Ultimately, the market can’t avoid the bearish implications of USDA’s old crop balance sheet and the negative spillover effects for the 2020/21 situation. The June and July WASDE numbers reinforced the previous two month’s projections of lower consumption and higher ending stocks. Recent indicators of reduced demand include a 79% decline in U.S. clothing store retail sales in April, and a correspondingly large decline in estimated consumer spending on apparel. Even May’s recovery of U.S. clothing retail sales is still below normal levels, and the June retail apparel sales show the same thing, i.e., higher month over month, but lower year over year.

The longer term damage to cotton consumption by the COVOD-19 pandemic will surely take many months to resolve. If there was a near term medical quick fix to the spread and effects of COVID-19, I would expect only a partial relief in commodity and equity markets. The “fear and panic” portion of the decline in cotton prices might keep ICE futures over 60 cents, perhaps reaching the mid-60s or higher. But the repairs to cotton’s global supply chain and consumers’ willingness to buy apparel may take longer to normalize. Hence a return to profitable market price levels may not happen during 2020.

From a marketing standpoint, both old crop and new crop cotton prices remain at the low level of the federal program price support. In government-speak, the adjusted world price (AWP) remains below the 52-cent loan rate. This makes for positive loan deficiency payment (LDP) rates for those who sell their cotton in the cash market (being careful to maintain beneficial interest). So the worst having happened (knock on wood), there isn’t much sense in paying for more downside price protection.