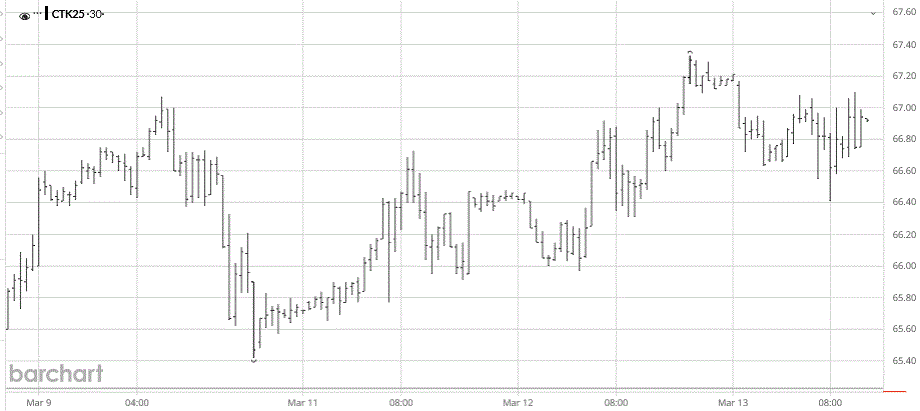

For the week ending Thursday, March 13, the nearby May’25 ICE cotton futures contract traded flat-to-higher higher (see chart above courtesy of Barchart.com). Chinese cotton prices were mixed, as was the A-Index of world cotton prices. The Adjusted World Price (a function of the A-Index) has weakened enough to generate a positive loan deficiency payment rate for the first time in years.

In other markets, the most active CBOT corn and soybeans contracts, as well as KC wheat futures, all traded flat-to-lower before shifting into a modest uptrend. The U.S. dollar index similarly glided lower and then higher across the week, with dollar strength at week’s end attributed to tariff-induced inflation expectations. This maintains the longer term appearance of a top to the post-Election Day rally that peaked January 13. Other macro influences (i.e., GDP, inflation, and interest rate policy) remained mixed in their expectation and implication.

Cotton-focused market influences this week included neutral old crop WASDE projections. For the old crop, probably all of the projected U.S. crop is ginned and classed as of early March. The last two months of U.S. export sales reports belie a slight uptrend, which was supported by decent enough export sales numbers for the week ending March 6. The pace of 2024/25 export shipments continue above the weekly average level needed to reach USDA’s target level of exports (11.0 million bales).

The dynamics of ICE cotton futures may also represent a wet blanket on the market. It remains true that unfixed call sales (by mills) are at an historically low level, perhaps reflecting the cautionary buying on the demand side. In absolute terms, unfixed call sales (by mills) are at an historically low level, reflecting the cautionary buying on the demand side. In terms of ratios, unfixed call purchases (by suppliers) outweigh unfixed call sales by almost two-fold across all contracts, as of March 7. In the nearby May’25 contract the imbalance is similarly in favor of unfixed call purchases. The implications of that imbalance are excess selling pressure on ICE futures when those May-based on call positions are fixed. Strictly speaking, this has less to do with the demand for cotton and more about the demand for futures by commercial hedgers.

Through March 12, the day-to-day fluctuations in open interest in ICE cotton were mixed in their direction, while the price settlements were flat-to-higher.

For more details and data on Old Crop and New Crop fundamentals, plus other near term influences, follow these links (or the drop-down menus above) to those sub-pages.

Source: TAMU