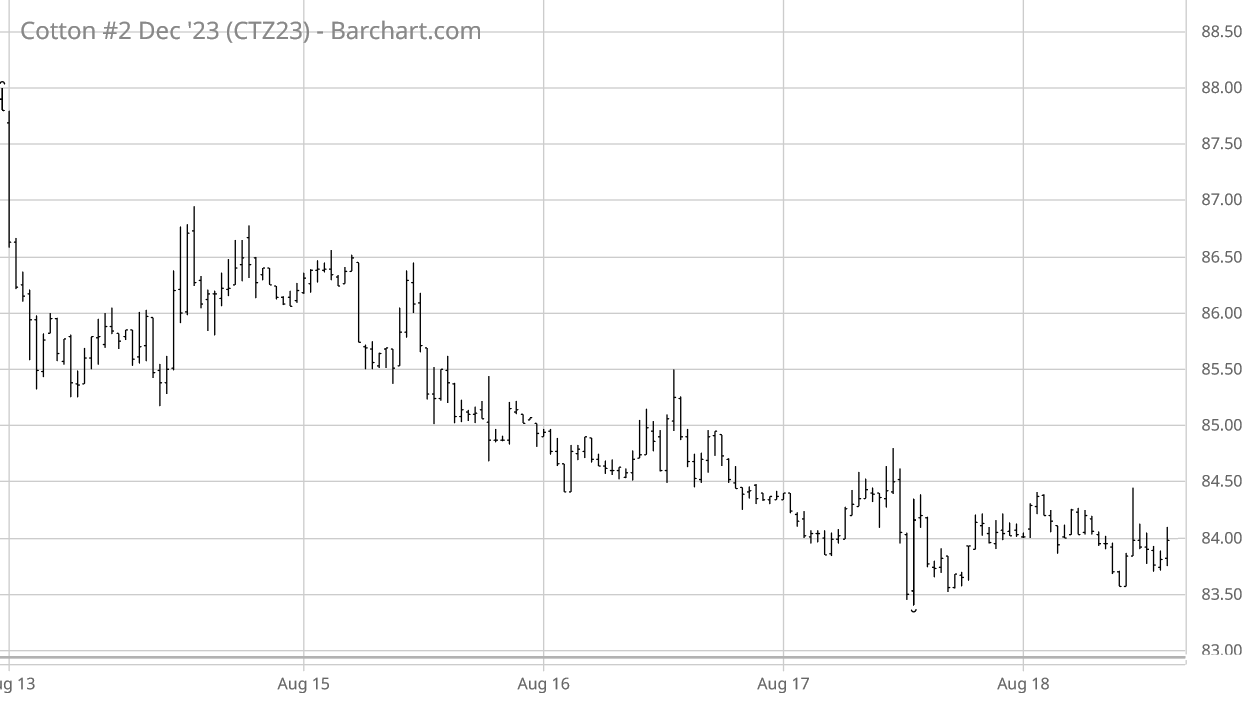

For the week ending Friday, August 18, ICE cotton futures slipped from the August 11 post-WASDE rally, then stabilized, and then eroded for the rest of the week (see chart above courtesy of Barchart.com). Chinese cotton prices fell this week following reports of Chinese economic unraveling, while the A-Index of world cotton prices was more mixed.

Other agricultural futures markets like CBOT corn, CBOT soybean, and KC wheat futures were flat/lower in the first half of the week and then flat/higher through the second half. The U.S. dollar index trended up to two month highs on Thursday. Other macro influences (i.e., GDP, inflation, and interest rate policy) remain a potential headwind to longer term cotton demand. For example, the week ending August 18 saw risk off selling in global financial markets due to the Chinese economic downturn.

Cotton-specific influences for the week included continued rainfall in the eastern Cotton Belt and an arcing band of showers from the Far North Delta region to the Texas Panhandle. The weekly regional summary of Texas continued to highlight hot and dry conditions (click here and scroll down for the Texas regional summaries). Looking back, the excess moisture in April/May had mixed effects in northwestern Texas, followed as it was by wind and heat. The resulting production uncertainty is still clouding the U.S. cotton supply/demand and market outcomes.

On the other side of the world, the southwest monsoon rains were relatively early in their complete coverage of India, albeit a bit below average in their early accumulation. July saw an intense flooding rains in northern India and Pakistan. Now the monsoon rainfall appears to be in a lull, with the major west central cotton growing regions showing a rainfall deficit. This maintains concerns about the agricultural impact of an historically dry August. Pakistan suffered crop damage from the excessive monsoon rains, and perhaps also from the more recent dryness. China’s main cotton producing region of Xinjiang had to deal with damaging temperature extremes. Meanwhile the U.S.’s two major export competitors in the southern hemisphere have been harvesting strong cotton crops.

Chinese buying supported decent U.S. export sales for the first full week of the new marketing year (through August 10). Actual export shipments were below the needed weekly average pace, but this is seasonally normal. USDA’s weekly summary of the U.S. regional markets continued to reflect mixed spot physical trading activity and very light to moderate demand, across the U.S. regions.

ICE cotton futures open interest declined across the week. In combination with lower ICE cotton settlements, this suggests long liquidation. The regular early-week snapshot of speculative positioning (through Tuesday, August 15) did, in fact, show a 1,776 decrease in the net long index fund position. However, there were 321 new hedge fund longs reinforced by 832 covered hedge fund shorts, compare to the previous Tuesday.

For more details and data on Old Crop and New Crop fundamentals, plus other near term influences, follow these links (or the drop-down menus above) to those sub-pages.