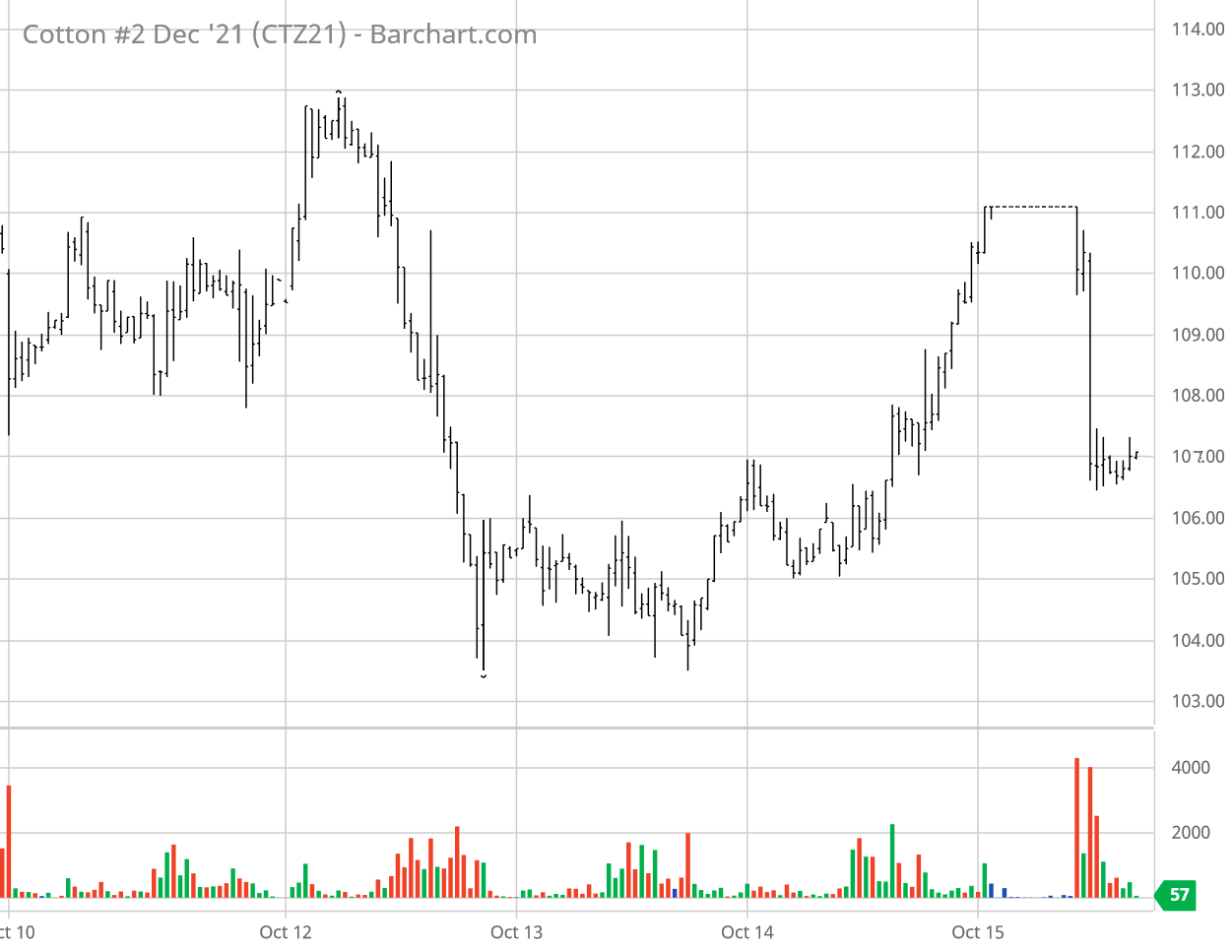

For the week ending Friday, October 15, Dec’21 ICE cotton futures gyrated higher and stair-stepped lower in a mixed pattern, settling Friday at 107.33 cents per pound. The level of ICE cotton futures open interest also fluctuated from day to day, indicating no clear trading pattern. However, two weeks ago the daily increases in hedge fund long open interest was large, e.g., four or five thousand contracts per day. In contrast, the daily adjustments in open interest this week were more like one or two thousand contracts. So I agree with the thought that the battle lines remain drawn between spec longs (looking to make or take profits) and commercial shorts (looking to fix on-call contracts at the lowest price possible). The most recent Tuesday snapshot (through October 12) did show long liquidation of ICE cotton futures with 10,190 fewer hedge fund longs, week over week. There was negligible increase in the number of hedge fund shorts or index fund longs, week over week. However, the index fund longs increased by 2,801 contracts.

Chinese cotton futures fluctuated around $1.50 per pound, while world prices trended lower this week. In somewhat contrast to ICE cotton, grain and oilseed futures markets showed a more distinct down-then-up trend across the week, as did U.S. stock indices. The U.S. dollar index showed a higher-then-lower trend for the week, ending lower for the first time in five weeks. All in all, cotton still appears to be dancing to its own tune.

Cotton-specific fundamental factors this week included both bullish (i.e., lower U.S. production) and bearish (lower world consumption) WASDE adjustments from USDA, lower weekly U.S. cotton export sales, continuing good U.S. cotton condition ratings, and unwelcome (for cotton) rains in various places, including Central/South Texas. U.S. cotton certified stock levels continued to erode after peaking in late June, which is perhaps more evidence of good export demand.

To the extent that the current rally was speculatively fueled, it could unfold unpredictably and dramatically. Speculative buying can be influenced by animal spirits, risk on/off developments, and other effects that have little to do with ag market fundamentals. I would also point out that this isn’t 2010, the last time we had dollar-plus cotton. Back then there was a global shortage, and the surging cash market pulled the futures market along for the ride. That is not the current situation.

The movement of ICE cotton futures has implications for potential hedging strategies. The price volatility in 2021 is a reminder why it is risky to hedge by selling futures, and it’s also made some option premiums more expensive. As new crop Jul’22 cotton futures risen in the last few months, a near-the-money 85 call option has increased in value. Between September 23 and October 14, an 85 call option on July’22 rose from 9.45 cents to 20.67 cents per pound. Had it been purchased in the previous months (i.e., back when some new crop was being cash contracted in the mid-80s), the current uptrend clearly illustrates the insurance aspect of call options. In general, a call option represents upside price risk protection, in combination with cash contracting or selling futures. Looking further out, the rising new crop Dec’22 futures contract has resulted in an out-of-the-money 80 cent put option premium declining from fourteen cents in January to 4,82 cents per pound by October 14. If Dec’22 futures keep rising, this and similar put options will become increasing affordable down-side price insurance. That is, once purchased, it will buffer unexpected declines in Dec’22 futures by increasing in value.

For more details and data on Old Crop and New Crop fundamentals, plus other near term influences, follow these links (or the drop-down menus above) to those sub-pages.

Source: tamu.edu