Cotton Market Update for the Week Ending December 1, 2017

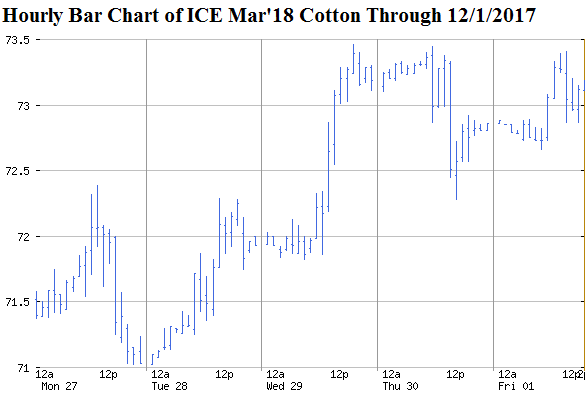

Since the middle of November, ICE cotton futures have climbed almost four cents. The week ending December 1 saw the most active Mar’18 gyrate around the 71.50 cent level before stepping up Wednesday to a higher level around 73 cents. Fundamental news this week included decent export sales which were in keeping with the normal pattern of export demand. The pattern of strong volume and rising open interest this week indicated new buying underneath the rally in prices, which was partially confirmed (through Tuesday) by the latest snapshot of speculative buying. Mar’18 ICE cotton futures settled the week at 73.28 cents per pound. The May’18 and Jul’18 contracts settled 60 and 78 points higher, respectively, reflecting a minimal amount of carry in the market. While this is an improvement over previous months, the market is still not really signalling to store cotton in hopes of higher prices. The old crop contracts were all inverted above Dec’18 which settled at 71.21 cents per pound on Friday. A sample of option prices on ICE cotton futures saw changes from the previous two weeks owing to the higher underlying futures contracts. On Thursday November 30, out-of-the-money 73 call options on Jul’18 ICE futures were worth 4.36 cents per pound; a further out-of-the-money 79 call on Jul’18 traded for 2.24 cents. Looking ahead to next year’s crop, a near-the-money 67 put option on Dec’18 cotton cost 2.63 cents per pound on Thursday, while an out-of-the-money 60 put on Dec’18 cost 0.79 cents. Chinese cotton futures and world price indices were both mostly higher this week.

More upside volatility could still come from surprising production cuts, coupled with continuing strong pace of U.S. export commitments and the eventual influence of large mill fixations. But there is also a risk to see futures weaken as much as ten cents (re: Ag Market Network November Conference Call) if the big crop gets bigger and/or if seasonally high U.S. exports turn out to be just a front-loaded pattern of what USDA has already been expecting. Remember, the current fundamental picture painted by USDA implies price weakness by virtue of a large year-over-year increase in ending stocks. In the short run, the potential for a price reversal is also there because of the fickle fuel of speculative buying that underlies the November rally.

Given all these uncertainties, growers should remain poised and ready to take advantage of rallies, and protect themselves from sudden sell-offs. Forward contracting, immediate post-harvest contracting, and/or various options strategies can be used to limit downside risk while retaining upside potential. In particular, contracted bales could also be combined with call options on the deferred futures contracts. It is also not too early to be evaluating the worth of put spread strategies to hedge the 2018 crop (or, really, to hedge the insurance base price).

{kind=link}