Hudson, Darren

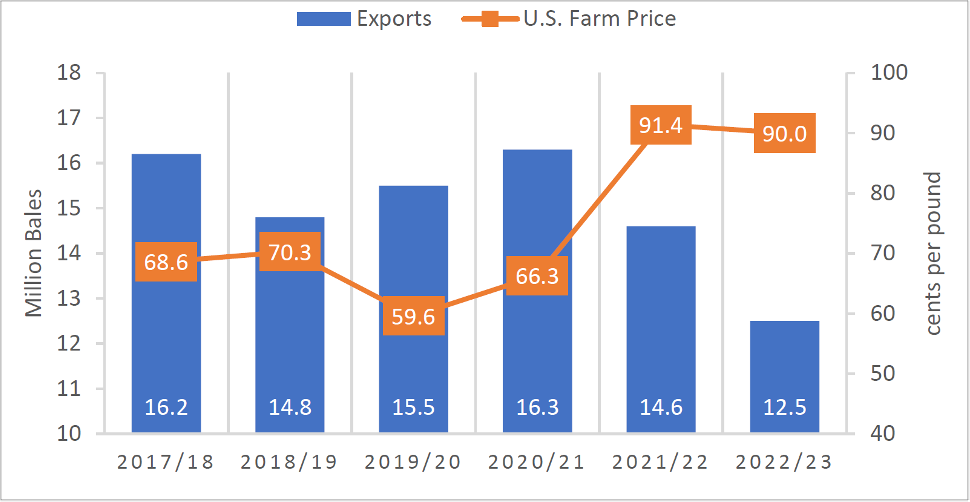

The drought of 2022 in Texas has taken its toll on U.S. cotton production, with USDA forecast 13.8 million bales (mb) (or 3.7 mb lower than 2021). Lower output equals lower exports, with current forecasted exports of 12.5 mb, down 14% from the previous year (See Figure 1). That also means lower ending stocks, currently estimated at historically low levels of 2.8 mb. But the drought (and higher than average price) has not slowed exports, with roughly one-half of expected production already sold or shipped where China has been the largest destination so far this year.

USDA data show the typical inverse relationship between crop size and farm price. And even though expected farm price is below last year, if realized, would be the second highest average farm price on record.

But there are concerns. Recent price action in the 22 and 23 December contracts have shown considerable weakness relative to earlier in the year. Recent lower prices would be expected to stimulate buying. In fact, exports do show strength. But there appears to be substantial selling pressure any time price moves up. And the market appears to be inverted with nearby prices above prices in out-month contracts suggesting current demand above future demand.

What is perplexing is the relatively low DEC23 price (currently in the mid-70 cents per pound range). That price level is insufficient to cover anticipated costs in many regions of the U.S. Also, relative to grains, the price for the DEC23 contract appears to signal fewer cotton acres next year. There is still time for prices to realign, but the market may be signaling lower anticipated cotton demand in 23 driven by higher apparel prices (and general inflation). For now, cotton is moving globally, and the US is likely to end the 22/23 marketing year with historically empty warehouses.