FEBRUARY 23, 2018

COTTON FUTURES SHARPLY HIGHER

President’s Day shortened the trading week, but that did not keep the cotton market from packing extra activity into the remaining four days. Cotton futures shot higher in Tuesday’s session, breaking what had been a rather long fall from the market’s highs. With March futures all but gone, May futures have become the central focus. May futures made their low at the beginning of the week, briefly touching 76.96 cents per pound after the open of Tuesday’s trading. Prices turned sharply higher from there, and the May contract rallied three-and-half cents through Tuesday. Prices fell back on Thursday, but resumed the rally Friday, taking May futures as high as 81.42 cents at Friday’s close. Although December futures did not rise at the same pace as May, prices in new crop had not really fallen either. In fact, it was December that made new highs this week with a new life-of-contract high at 76.68 cents at the end of trading Friday.

COTTON CLASSING SLOWS

U.S. production for 2017-18 has become a topic of conversation again. As of Feb. 22, USDA had classed 19,319,272 samples. Of the 548 gins to submit samples this season, 106 were still receiving results, down from 138 last week. All Oklahoma and Kansas gins were still counted, as were 59 of Texas’ 199 gins. Only 187,153 samples were classed this week, and the fact that classing is slowing down has some analysts concerned that USDA’s 21.26 million bale production figure may be a little too high. The market still lacks approximately 1.4 million bales to hit USDA’s estimate. While Mid-South and Southeast regions seem likely to be reduced somewhat, figuring whether there will be a Southwest production shortfall seems a little premature with so much cotton still to gin. In any case, market watchers seem to be leaning lower for final U.S. production in 2017-18.

GOOD EXPORT DEMAND CONTINUES

On the demand side of the market, U.S. export sales continue to impress. For the week ended February 15, cotton exporters sold another 399,100 bales for shipments this marketing year, and 177,200 bales for 2018-19. Twenty different destinations were buying last week, and the largest buyers included China (68,400 bales), Bangladesh (57,600), Turkey (56,000), Indonesia (52,400) and Vietnam (40,600). The broad-spread interest indicates healthy demand. While U.S. export commitments have reached 95 percent of the current USDA forecast, last week’s shipments were just average. Many traders believe weekly shipments need to increase dramatically before USDA will reverse the downward revision it made to its 2017-18 U.S. export estimate in February. In any case, relatively slow shipping did not seem to bother the market, which rallied 1.50 cents higher after the figures were released.

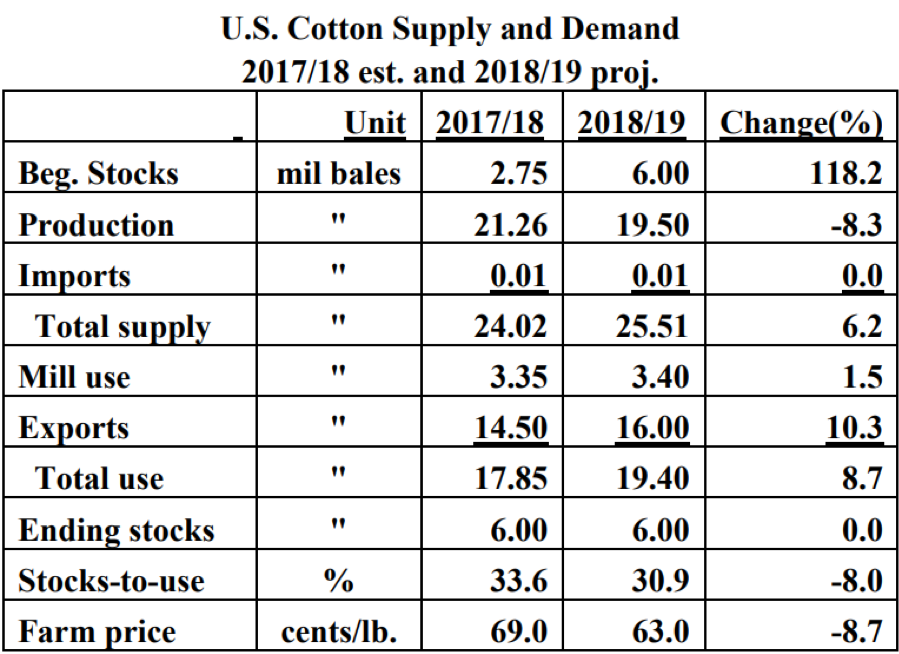

USDA RELEASES FIRST ESTIMATES FOR 2018-19

Turning attention to next year, USDA held its annual Agricultural Outlook Forum on Thursday and Friday and unveiled its first estimate of 2018-19 agricultural production. The forecast is influential, and the markets will take it into account. However, the balance sheets released at the Forum differ from WASDE (World Agricultural Supply and Demand Estimates) forecasts in at least one significant way. The Forum’s balance sheet is based entirely on forecasts. As the year progresses, surveys, reported acres, and observed data gradually replace predictions. The first major replacement will be planted acreage when USDA releases its own Prospective Plantings on March 29. Nevertheless, the Forum’s 2018-19 balance sheet is the only official USDA balance sheet that traders will see until May, when monthly WASDE forecasts for next season begin. Below is the 2018-19 projection as supplied by USDA.

USDA’s planted acreage figure (13.3 million acres) is slightly higher than the National Cotton Council’s estimate (13.1 million), because of cotton’s re-entry into the farm program. The NCC’s export estimates also were higher for 2017-18 (14.99 million bales vs. USDA’s 14.5 million), but much lower for 2018-19 (14.3 million vs. 16.0 million). USDA also penciled out slightly higher production (NCC was at 19.4 million bales). Nevertheless, USDA’s higher exports in 2018-19 kept ending stocks flat with the current year, and even slightly tightened the U.S. stocks-to-use ratio. Despite the relative tightening, the farm price forecast decreased to 63.00 cents per pound for next season from 69.00 cents expected this season.

NORMAL REPORT SCHEDULE NEXT WEEK

In some sense, things return to normal next week. Reports will be released on their usual schedules, and there are no major industry conferences releasing annual forecasts. Multiple forecasts of larger supply have been unable to shake the cotton market lower, and the resilience of mill demand for U.S. cotton is a large factor supporting the market. In addition to the export sales report, traders will be dedicating some attention to long-term weather forecasts as concerns about the Southwest drought continue to reduce next year’s production prospects.

IN THE WEEK AHEAD:

- The Export Sales Report will be released Thursday at 7:30 a.m. Central Time.

- The CFTC Cotton On-Call report to be released Thursday at 2:30 p.m. Central Time.

- The CFTC’s Commitments-of-Traders will be released Friday at 2:30 p.m. Central Time.