Cotton Market Update for the Week Ending Friday September 21, 2018

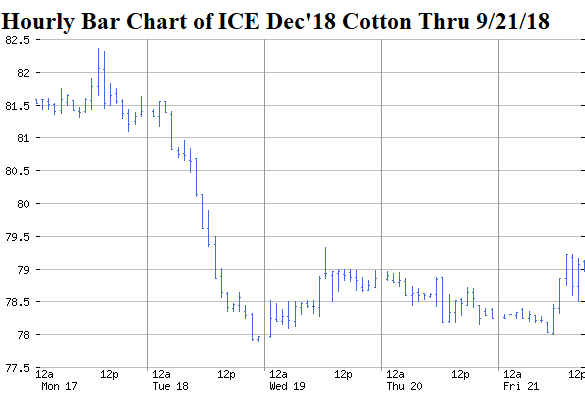

The week ending September 21 saw ICE cotton futures start off going sideways before taking a 2.5 cent stair-step down in a high volume sell-off. After that trading resumed the sideways pattern to close the week. Tuesday’s price drop was associated with speculative long liquidation in apparent fear of newly announced expanded tariffsbetween the U.S. and China. Technical signals like violating the 200-day moving averagemay have encouraged speculative selling. Other fundamental influences this week included so-so weekly export sales, a remaining seasonally high level of export commitments, and unhelpful tropical rainfall along the Gulf Coast and Atlantic Seaboard. Chinese cotton prices down-trended this week while world prices were followed the single down-shift pattern of ICE futures.

The Dec’18 contract settled on Friday at 79.13 cents per pound. The Jul’19 contract settled the week at 80.72, while the distant Dec’19 settled Friday at 76.60 cents per pound.

A sample of option premiums on ICE cotton futures saw changes from the previous week due to the decline in the the underlying futures. On Thursday, September 20, a deep in-the-money 90 cent put option on Dec’18 cotton was worth 11.74 cents per pound, up from 9.05 cents the previous week. Similarly, an 85 put settled Thursday at 7.08 cents per pound (+2.21 cents on the week) while an 80 put settled at 3.16 cents per pound (+1.32 cents on the week). These values and their weekly change show how put options increase in value with falling futures prices, thus acting as down-side price insurance. An out-of-the-money 85 call on Jul’19 cotton was worth 3.07 cents per pound, down 1.3 cents from the previous week. Looking way out there, a near-the-money 75 put on Dec’19 cotton settled Thursday at 4.5 cents per pound.

This week provides an example of the ever present risk of unexpected market volatility. It can happen in both directions. For example, a surprise resolution to U.S.-China trade relations, extensive damage from another hurricane, revising Indian stocks downward by USDA, or something else totally unexpected could trigger speculative buying. As always, the most relevant question is whether a cash contract or a hedge on today’s futures pricewill be a profitable, or at least survivable, price floor.

Given all these uncertainties, growers should always be poised and ready to take advantage of rallies, and protect themselves from sudden sell-offs. Forward contracting of new crop bales, immediate post-harvest contracting of old crop bales, and/or various options strategies can be used to limit downside risk while retaining upside potential. Earlier hedges with puts or put spreads on Dec’18 futures should be evaluated with an eye towards exiting those positions in the next month or so. Contracted 2018 bales could be combined with call options on the deferred futures contracts. New crop put strategies to hedge the 2019 crop are a straightforward and relevant approach.

Πηγή: The Cotton Marketing Planner