by Andy Ryan

The current partial government shut-down here in the USA continued to be a drain on many markets during the opening days of 2019. Additionally, the shut-down is delaying any new numbers from the USDA, FAS and CFTC, which are all government entities. Cotton needs these numbers to help guide price discovery on the ICE #2 Cotton contract. Going on two weeks now, the lack of fresh data adds more uncertainty to the market. Speaking to those in the physical cotton trading business leads me to believe that there is demand for cotton at the current prices, although nothing huge. While the price has dropped around 9 US cents/lb over the past month, the selling basis strengthened only about 1.00-1.50 points for US bales or about half of what would be considered normal for such a drop in futures prices.

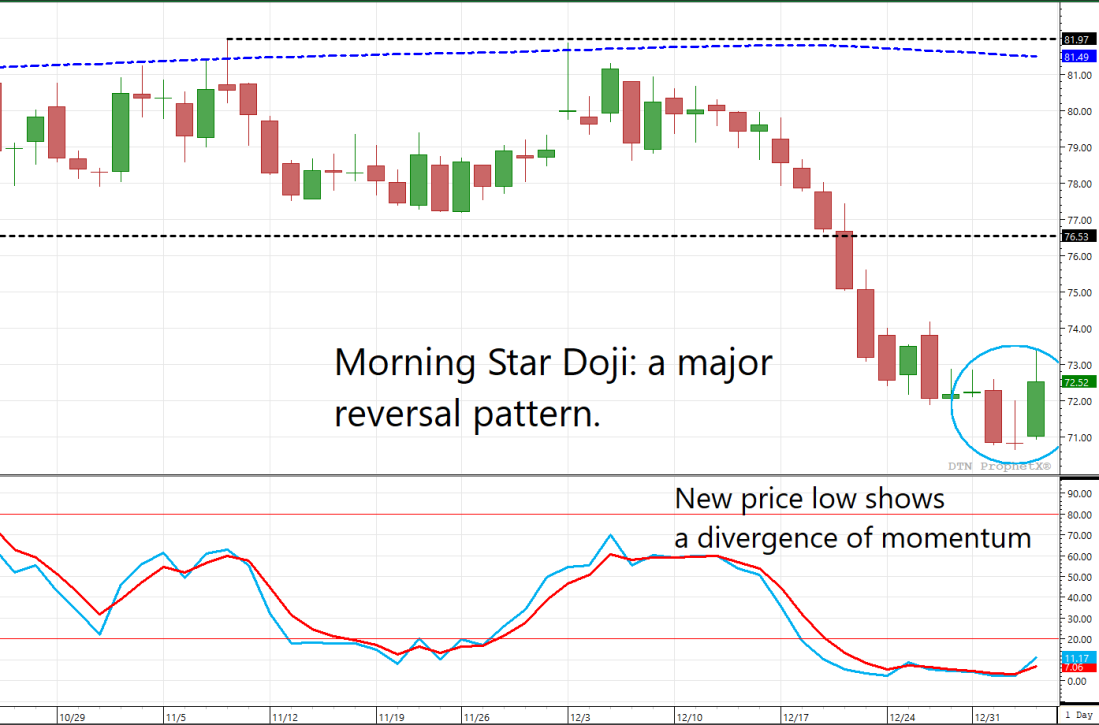

Because there is no fresh data to guide the market, looking at the technical situation might be helpful. Today’s rally marked a three-day reversal pattern known as a morning star doji according to Japanese candlestick theory. The doji session, in which the open and close are the same, is a warning signs to the bears that momentum has stalled. However, it is the large green up candle today that confirms the warning. In the context of the large down move and range break out of the last month lends validity to the potential reversal.

Despite not being able to see fresh data from the CFTC on-call report, I imagine it is still showing the same general crop year trend as in recent years. That means, the producer (mostly US in this case) has already priced much of this year’s crop, leaving a limited number of natural sellers against the March19, May19 and July19 contracts. While on the other side, the mill still has huge quantities to fix (buy futures) during the same period. The same dynamic has helped the market maintain a somewhat bullish seasonal bias during the first half of the calendar year in recent experience. In very simple terms, there are more natural buyers than sellers for the remaining crop year contracts.

by Andy Ryan

andy.ryan@bnacommodities.com

Πηγή: The Cotton Trader