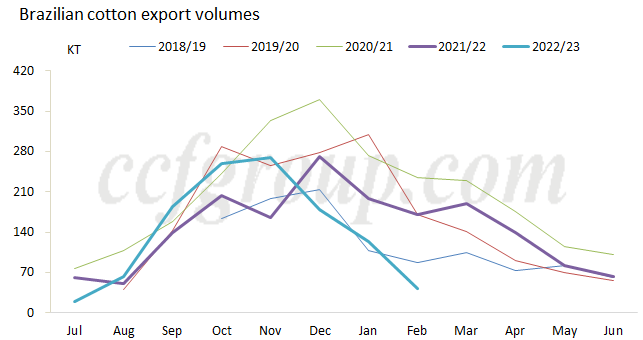

In Feb 2023, Brazilian cotton exports are 43kt, down 65.32% from Jan, down 73% from Feb 2022, and down 69.2% from the same period of prior five-year average, to hit a historical low. Moreover, combined with the exports of 2022/23 U.S. cotton, not only the demand in China is weak, but also the market outside China, like Southeast Asia, seeing the weak cotton consumption.

1. Brazilian cotton exports are lower than anticipated

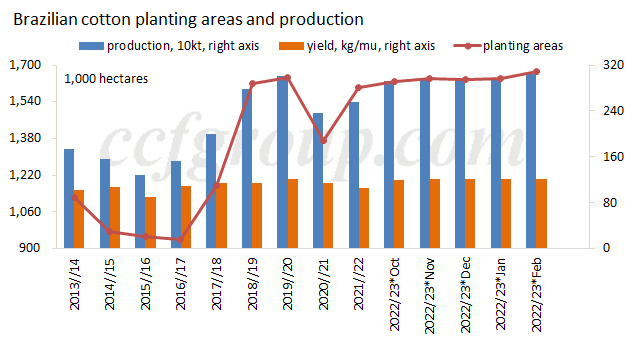

According to the Feb report of CONAB, the forecast on 2022/23 Brazilian cotton production remains at 1.978 million tons, up 9.6% year on year, while down 4kt from prior three-year average. Exports are forecast to be high. But according to the export data by now, the exports are high first but then weaken. From Aug 2022 to Feb 2023, exports totaled 1.119 million tons, a fall of 80kt from the same period of previous year and down 600kt from 2020/21 season. The large decline of monthly exports is likely to be related with the foreign exchange reserves crisis of Pakistan, Turkish earthquake and difficulties in opening Letters of Credit in Bangladesh. To some extent, it also reflects that the cotton consumption outside China is on downside.

2. Competitive U.S. cotton exports are also low

With the large reduction of Brazilian cotton and the competitive relationship with U.S. cotton, some market players wonder whether it is because of the lower U.S. cotton prices in recent two month and the high offers of Brazilian cotton. Viewed from the recent U.S. cotton weekly export sales, though the export sales reach 100kt to hit a marketing-year high by the week ending Feb 16, the data next week declines to 38.7kt. Based on the previous years’ data, the U.S. cotton exports should warm up gradually in mid-Jan and reach the peak in mid-Feb, but this year, U.S. cotton exports see no obvious improvement, far lower than the same period of previous years. The import demand for cotton outside China is sluggish apparently, and the economic recession in Europe and U.S. restrains the global apparel consumption obviously.

3. Planting of Brazilian cotton ends, and 2023/24 season may be a bumper year further

According to CONAB, cotton planting was complete by Feb 25, and the planting developed well in Mato Grosso, reaching 99.6% by Feb 24. In its Feb report, planting areas are projected at 1.673 million hectares, to a record high. The planting is late in Mato Grosso and the yield may be impacted, but if the weather is normal later, Brazilian cotton production is still expected to be good. Nevertheless, based on current unsatisfied export data, the exports face selling pressure. Besides, local cotton prices fluctuate downward recently. If the selling pressure increases later and cotton prices move lower, international cotton prices may face upward pressure.

Currently, Chinese downstream market reflects that export orders are dull, and we also communicate with traders with overseas business, the export orders of Southeast Asia are also poor. Looking from the export data, the global cotton consumption is not favorable in traditional peak season outside China. On supply side, the cotton planting ends in South Hemisphere, and speculative topic is only on the planting areas in North Hemisphere. U.S. cotton prospective planting areas will be released in end month, and market players expect the planting areas reduce by 20%. Meanwhile, the expectations of US Fed to raise the interest rate in Mar are strong and under the background of weak consumption, international cotton prices face upward pressure before end Mar.

Πηγή: ccfgroup.com