International cotton prices hit new high during the Spring Festival holiday, stimulated by the marketing-year high of U.S. cotton export shipments, limited improvement of Indian cotton arrivals and small growth of cotton production in Pakistan. Nevertheless, on the first trading day returning from the holiday, Zhengzhou cotton futures market rises limitedly, and domestic cotton market is obviously weaker than foreign market. In the meantime, the sowing progress of cotton crops in Brazil is comparable with that in 2019/20 season. The 2022/23 global cotton production has shown signs of growth, and later, the upward space of prices may be limited.

I. Foreign cotton market stronger than domestic market before and after the Spring Festival

During the Spring Festival holiday, the spot cotton prices in the major cotton producing countries (India, U.S., Brazil and Pakistan) have hit the new highs, and ICE cotton futures were firm obviously. On the first trading day returning from the holiday, though ZCE cotton futures opened high, the increment was smaller compared with foreign cotton.

| International cotton price change during Spring Festival holiday | |||

| 2022/1/27 | 2022/2/4 | Growth rate | |

| ICE cotton (cent/lb) | 116.63 | 120.91 | 3.70% |

| Cotlook A (cent/lb) | 136.45 | 141.5 | 3.70% |

| Indian cotton, S-6, 29mm (Rs/Candy) | 76000 | 78000 | 2.60% |

| Brazilian cotton, CEPEA/ESALQ Index (cent/lb) | 129.37 | 131.92 | 2.09% |

| Pakistani cotton, Karachi spot rate (Rs/maund) | 19400 | 19700 | 1.50% |

| ZCE cotton (yuan/mt) | 21675 | 21895 | 1.09% |

II. U.S. cotton export shipments increase

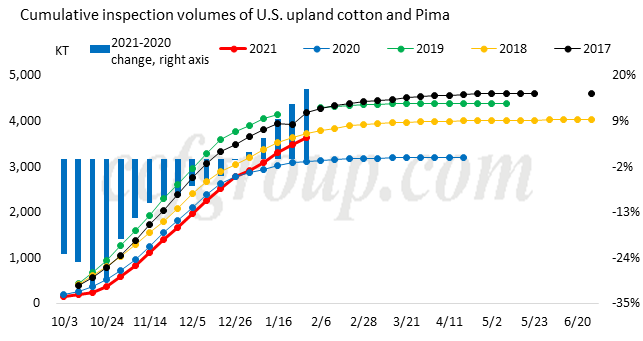

According to USDA, by the week ending Jan 27, inspection volumes of U.S. upland cotton reached 3.5771 million tons, up 18.3% year on year, about 95.2% of the forecast production (3.73 million tons) and the inspection volumes of upland cotton and Pima totaled 3.6466 million tons, up 16.7% year on year, about 95.1% of the forecast production (3.836 million tons). The proportion of the upland cotton tenderable against ICE futures amounted to 83.5% for the marketing year, up 8.1 percentage point year on year.

Since Jan, the yearly growth of cumulative inspection volumes continued to expand, and the proportion of the upland cotton tenderable against ICE futures also maintained high. With the guaranteed production and quality, the weekly export shipments started to rise from Jan.

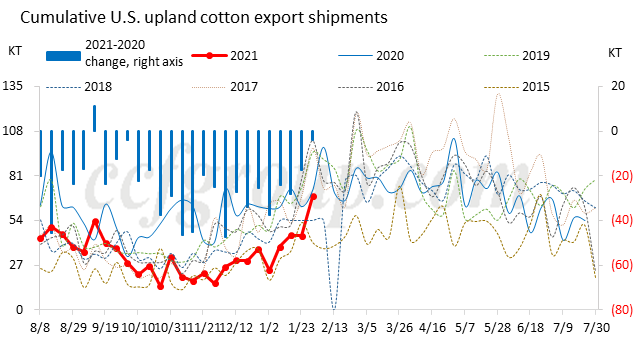

By the week ending Jan 27, export sales of 2021/22 US upland cotton were 75.3kt, down 15.1% from previous week and up 10% from prior 4-week average. The cumulative export sales were 2.7195 million tons, a fall of 6.1% year on year. Weekly export shipments were 68.5kt, up 52.7% from previous week and up 80.8% from prior 4-week average. Total export shipments were 885.2kt, down 41.9% year on year. Export sales of 2020/21 upland cotton and Pima amounted to 2.809 million tons, about 86% of the forecast exports, and export shipments totaled 926kt, about 33% of the export sales.

The rise on the weekly export shipments was mainly benefited from the stimulus from China, Pakistan and Vietnam. Meanwhile, in Jan, the export sales from India also increased. Based on the seasonality, U.S. cotton export shipments may speed up later.

III. The peak of Indian cotton arrivals has passed

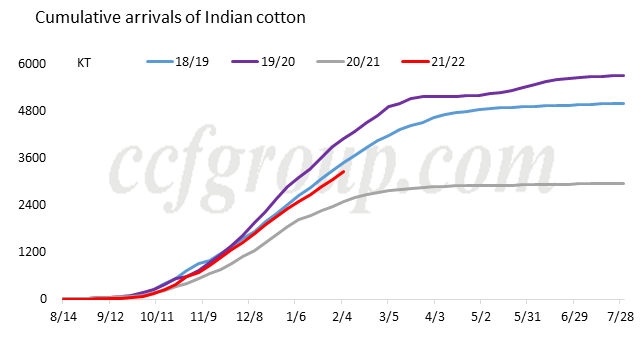

According to AGM, by the week ending Feb 5, the weekly cotton arrivals were 200kt, up 93kt from the same period of last year and up 26kt from the prior 3-year average. The cotton arrivals amounted to 3.27 million tons, up 780kt from the same period of last year, and down 90kt from the prior 3-year average.

Based on the arriving progress in previous years, about 66-72% of Indian cotton is supposed to be arrived on the market currently, and the peak has passed. Later, the arrivals may fall down gradually. In addition, according to the planting areas and weather condition this season, Indian cotton production may be around 5.67 million tons. Nevertheless, with the gradual end of arrivals, the stimulus from the supply side on the prices will weak gradually.

IV. Arrivals of Pakistani cotton end

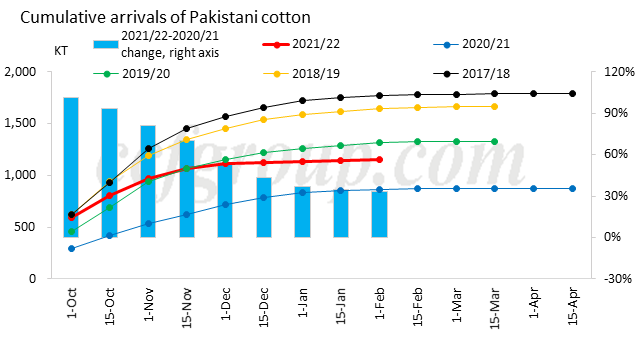

According to statistics from the Pakistan Cotton Ginners' Association (PCGA), by Feb 1, the new cotton arrivals approached 1.15 million tons, a year-on-year rise of 33.2%. The purchases from textile mills were 1.121, up 43.3% year on year.

Based on the arriving progress of previous years, the arrivals have virtually ended currently, and production is basically settled. Though the spot cotton prices hit new highs, its seed cotton prices have grown limitedly.

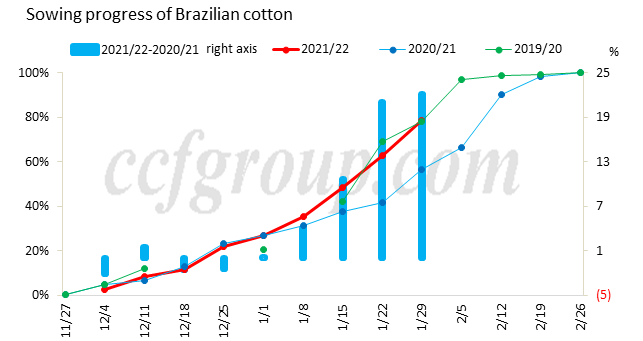

V. Steady improvement on the cotton planting in Brazil

CONAB: By the week ending Jan 29, the sowing progress of cotton crops in Brazil reached 78.8%, up 16% from previous week and up 22% from the same period of last year.

IMEA: by Jan 21, the sowing progress in Mato Grosso was 40.45%, flat from the same period of last year, and down 4.66% from 5-year average.

Currently, the sowing progress of cotton crops in Brazil is comparable with that in 2019/20 season. The high cotton prices stimulate growers to plant obviously.

Overall, international cotton prices hit new high during the Spring Festival holiday, stimulated by the marketing-year high of U.S. cotton export shipments, limited improvement of Indian cotton arrivals and small growth of cotton production in Pakistan. Nevertheless, on the first trading day returning from the holiday, Zhengzhou cotton futures market rises limitedly, and domestic cotton market is obviously weaker than foreign market. In the meantime, the sowing progress of cotton crops in Brazil is comparable with that in 2019/20 season. The 2022/21 global cotton production has shown signs of growth. Meanwhile, the high cotton prices have started to drag down the consumption. Later, the upward space may be limited.

Πηγή: CCFGroup