ZCE cotton futures market is on upward trend from Apr, and from mid-Apr, the bullish factors from supply side come gradually. On Apr 14, Xinjiang cotton target price policy was released, and the subsidy with a fixed production of 5.10 million tons was the first bullish factor. Next, in late Apr, especially during the May Day holiday, temperature in Xinjiang kept low, and South Xinjiang suffered sandstorm, rainy and snowy weather. North Xinjiang suffered snowy weather and low temperature. Under such condition, ZCE cotton futures market was sharply higher after the holiday, and the major contract continued to reach 16,000yuan/mt. Will ZCE cotton futures market continue to rise?

First, from the angle of supply, we have mentioned in the previous article-How is the weather in Xinjiang, that the weather was also unfavorable in late Apr, 2021, but improved in Jun-Aug. The 2021/22 Xinjiang cotton production reduced by 8% year on year. This year, the low temperature lasts longer than 2021, and according to the latest forecast report in Xinjiang, temperature in Aksu, Wusu, Changji and Bortala Mongolian Autonomous Prefecture remains low, with frost early warning, which is unfavorable for the sprout of cotton crops sowed before. Temperature is forecast to recover from mid-May. Before the temperature improves, cotton prices may be hard to decline. Compared with the high yield last year amid favorable weather, the yield of Xinjiang cotton in 2023/24 may reduce by 10% or above, and if the accumulated temperature is good after re-planting, arrivals of Xinjiang cotton may be late somewhat.

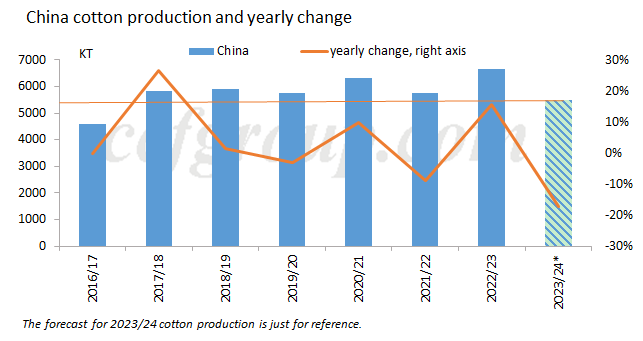

On Apr 23, Cotton Association of China issued the third survey of planting intentions. The national planting areas may reduce by 7.4% year on year in 2023, and that in Xinjiang may reduce by 4.3%. Barring the reduction of Xinjiang cotton areas, areas in Yangtze River and Yellow River see larger reduction of 32.2% and 22.8%. Plus the lower yield of Xinjiang cotton, 2023/24 China cotton production may see relatively large reduction, especially under historical high of production in 2022/23 season, the yearly reduction may be obvious in 2023/24.

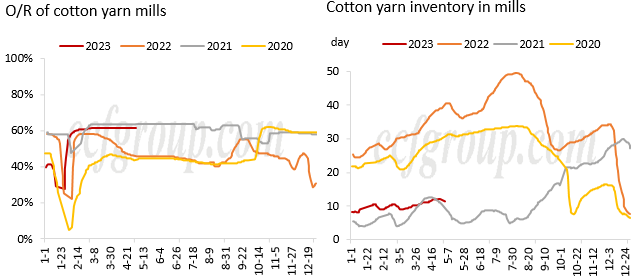

From the angle of demand, though downstream demand is weaker than Mar, and spot profits of spinners in inland keep negative, operating rate of spinning mills remains high, and product inventory is low. The negative performance in downstream sector is not obvious. Cotton yarn prices move up following higher cotton prices, and pay attention to the yarn price, sales and operating rate later.

In general, temperature in many regions of Xinjiang remains low, and the weather forecast shows that temperature will warm up till mid-May. 2023/24 China cotton production may see large reduction. Downstream spinning mills' operating rate remains high and product inventory is low. In short, cotton prices may remain firm. But inland spinners have seen losses and after Chinese cotton prices rise, substitution from imported cotton, cotton yarn, PSF and VSF increases. Cotton prices also face more pressure. Pay attention to the operating rate of spinning mills later. If the operating rate reduces in late May and Jun, cotton prices are expected to reduce in short, but in medium to long run, prices may remain strong.

Πηγή: ccfgroup.com