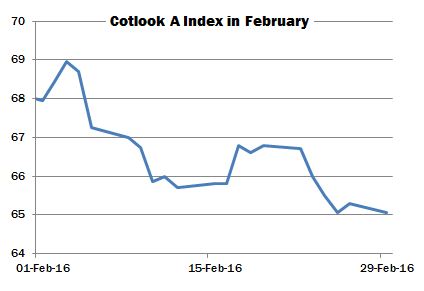

International raw cotton prices declined during February, with New York retreating below the previously well-established range. ICE futures posted life-of-contract lows on several occasions, as did those on China’s ZCE and CNCE platforms. The Cotlook A Index lost a net 290 cent points on the month (the A Index has moved lower by 490 cent points since the beginning of the calendar year, representing a loss of 7.5 percent of its value by the end of February).

Cotton appeared finally to have succumbed to the pressure of a negative macro-economic environment which had influenced other commodities in recent months. Broader-based mill demand was to some extent prompted by the decline in asking rates, and buying interest occasionally extended beyond the nearby delivery period. However, the market did not reach a level at which the vast majority of spinners felt sufficiently confident to abandon a hand-to-mouth buying policy, and begin to cover further forward.

In addition to the sustained decline of futures, the potential impact of ChinaΆs impending state reserve sales remained an unsettling factor. Uncertainty tended to confine spinnersΆ enquiries in that destination to very nearby or afloat cotton. In the wider international market, the prospect of a large release from the state reserve likewise continued to engender some apprehension, most notably amongst those spinners that are customary exporters of cotton yarn to the Chinese market. The spinners in question stand to face increased competition from local spinners, should the latter have access to attractively-priced cotton from the state reserve. The consensus at the end of the reporting period was that sales are likely to begin in April, but no official confirmation had been forthcoming.

The growths in demand during the month included West African, Brazilian and (principally for neighbouring markets) Indian cotton, with the result that the supply positions in those origins were perceived to have tightened, particularly for the more desirable qualities. Estimates of production in India and some African Franc Zone countries were reduced during the month. The reduction of exportable stocks, coupled with persistent demand and lower futures, had by the end of the month contributed to a modest strengthening of basis levels for these origins.

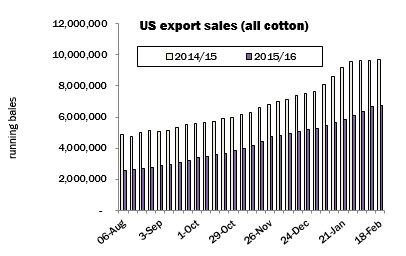

US export sales also began the month on a strong note, and continued in a positive vein, registering a marketing-year high in the report released for the week ended February 11. However, the subsequent report saw a number not much in excess of 100,000 bales. The discrepancy between cumulative sales during this season and last therefore remained substantial, at almost three million running bales.

By far the biggest shortfall in commitments to traditional export markets for the United States concerns China. Also noteworthy, however, is the unfolding situation in Turkey, where a recommendation has been made for anti-dumping duties on the import of US raw cotton, following a lengthy investigation. Spinners put their case against such a measure at a hearing held on February 24. Pending confirmation of the governmentΆs intentions, their appetite for US cotton, which had previously been very active, all but disappeared. In the 2014/15 season, over 40 percent of TurkeyΆs raw cotton imports were of US lint. The sole adjustment to USDAΆs domestic supply and demand estimates in February was a reduction in the export projection of 500,000 bales, which resulted in a commensurate rise in projected ending stocks, to 3.6 million.

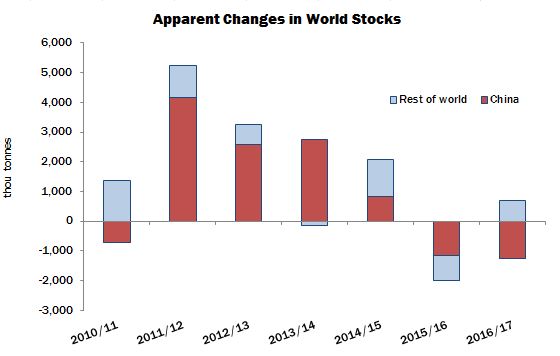

Cotton OutlookΆs initial, tentative estimates for global production and consumption in the 2016/17 season were released in the last week of the reporting period, and imply a second consecutive season of decreasing world stock levels, albeit with the drop occurring in China, whereas stocks outside that country are expected to recover, following a reduction this season.

Global cotton production is predicted to increase by around eight percent, to 22,748,000 tonnes, though that still represents a decline of eleven percent from the volume produced in 2014/15. Planted area is expected to rise modestly, with some countries, including the US, increasing acreage. However, the biggest improvement is anticipated to result from a recovery of yields in some major producers, including India and Pakistan, where pest infestations and unseasonable weather have dogged the growing season this year.

Cotton consumption is expected to remain stagnant, with a projected increase of just 1.4 percent. An unpromising economic environment and continued intense competition for market share from man-made fibres for the time being rule out a more positive forecast. Bangladesh has continued to consolidate its position as the favoured source of ready-made garments for Western importers, and Vietnam has remained a target for significant outside investment, with the result that consumption in those markets is expected to increase by 10 and 20 percent, respectively. Elsewhere, however, consumption is not expected to be reignited with any vigour, and indeed many countries may witness a marginal contraction.