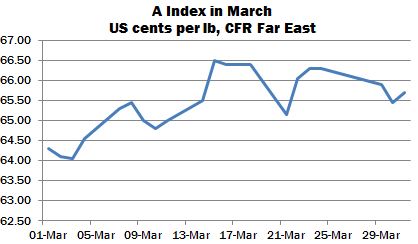

International cotton prices have advanced in the past month, influenced by upward movements in New York, and have returned to the lower end of the previously well-established trading range, which had prevailed for several months. The Cotlook A Index started the period close to its lowest point during the month of 64.05 US cents per lb, and advanced to a high-point of 66.50 cents per lb on March 15, before subsequently easing to end the month slightly below that level (65.70).

International business activity has remained much the same as in the past several months, with spinners generally unwilling to extend demand beyond hand-to-mouth requirements. Mills have remained concentrated mainly on cotton for nearby delivery. The steady pace of business during the past few months has resulted in a fairly well-sold position for many trade sellers, with the result that the volume of cotton available from certain origins during the remaining months of the season appears to be becoming tight. However, little demand for cotton further forward has been in evidence, with the exception of some Brazilian new crop into Far Eastern markets.

Sellers perceive the prospective dwindling supply of higher grades as being a supportive price factor, and some growths (most notably African Franc Zone and Indian) have seen their bases firm against ICE futures, but with a sluggish yarn market and high replacement costs, spinners have continued to resist increases in asking rates.

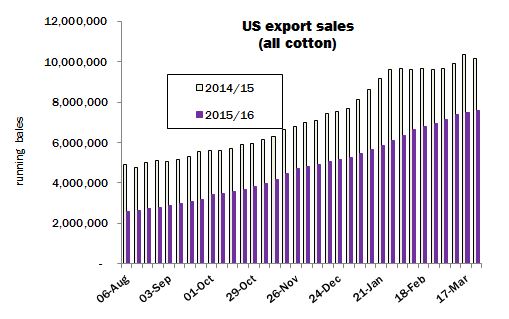

US export sales reports released during March have painted a rather mixed picture, with strong numbers in the first half of the month and a less robust pace in the succeeding weeks. However, should the recent momentum be maintained, USDA’s current forecast for the season (9,500,000 bales of 480 lbs) seems achievable. At the time of writing, the discrepancy between cumulative sales during this season and last has narrowed, but remains considerable, at almost 2.6 million bales.

Turkey has continued to feature quite heavily as a destination in US export reports, despite the approaching deadline for Ankara to clarify its position as regards the imposition of the proposed anti-dumping duties on US cotton.

Announcement of the details regarding sales from ChinaΆs state reserve is still awaited. Disclosure has been made of the quantities that will initially be readied for sale over an extended period (consisting mainly of the older stocks but including some 300,000 tonnes of imported lots). A mid-April starting date to the sales campaign is widely anticipated, but as yet unconfirmed, as is the mechanism by which prices will be established. Indications are that the latter will be set by reference to a combination of domestic and international price indicators on a weekly basis. Until the details become clear, however, the potential impact on international cotton and cotton yarn prices remains difficult to construe.

As spring planting windows open in Northern Hemisphere growing countries, focus is intensifying on farmersΆ choices of crop. In the United States, WashingtonΆs assessment of planting intentions foresees an eleven percent increase overall, compared with last year, including a strong rise (36 percent) in the area sown to Pima. An overall decrease of around ten percent, meanwhile, is foreseen in China, though growers in Xinjiang may still give preference to cotton, among competing crops, given the subsidy regime in place. In India, the government has issued a directive that farmers should adhere to a sowing ‘windowΆ as one measure that might help in the effort to prevent a repeat of last yearΆs insect damage. Private estimates in Pakistan, which likewise sustained heavy losses in 2015, cover a fairly wide range, owing to uncertainty as to whether pest damage will persist, even if more normal weather pattern should prevail. Planting has begun in the early sown districts, but a lagging winter wheat harvest threatens to slow the process.

Cotton OutlookΆs global supply and demand estimates were unchanged in March. A modest fall in global stocks is predicted (occurring principally in China), an improvement (albeit tiny) is foreseen in consumption and, as previously mentioned, increasingly tight supplies nearby are noted for some origins. However, tough trading conditions persist in global cotton yarn markets, something which will not be eased if ChinaΆs import tempo is indeed slowed as a result of the forthcoming policy announcement for state reserve sales of raw cotton.