USDA’s September WASDE report was as surprising as the previous month, but in the opposite direction.

The September world numbers were reasonable enough. They reflected net gains in world stocks from supply side increases to the 2022/23 world old crop cotton balance sheet, driven largely by U.S. adjustments (see below). Beginning stocks were raised a negligible 70,000 bales, month over month. World production was 1.44 million bales higher compared to last month, as a result of increases in the U.S., China, Australia and Turkey that outweighed decreases to flood-ravaged Pakistan. Forecasted Indian production was unchanged, month over month, implying that the effect of excess rains on Indian cotton production is, so far, a literal wash.

The world trade categories were little changed after a few mostly offsetting adjustments. Most notably, Pakistani imports were raised as an impact of their production losses. World consumption was cut 460,000 bales, again mostly in Pakistan, along with a 100,000 bale cut in Vietnamese spinning. The cuts to world total use were outweighed by the gains in production, leading to a two million bale increase to world ending stocks, month-over-month. This adjustment is fundamentally price negative in the size of the monthly decline, although the resulting stocks level has historically neutral price implications.

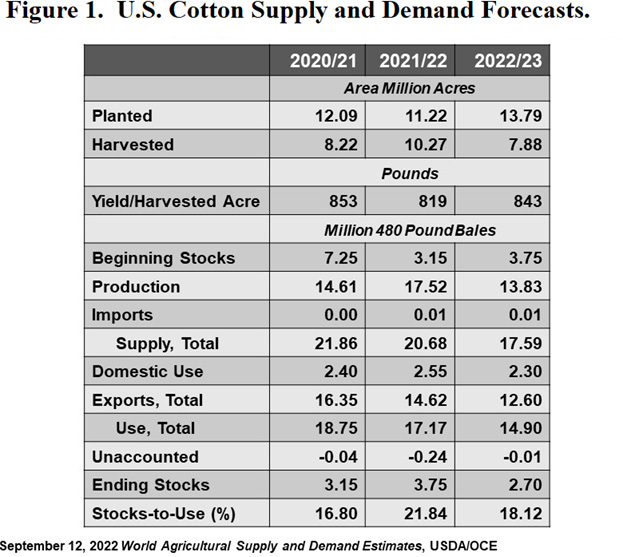

The U.S. 2022/23 crop cotton balance sheet (see Figure 1, last column) saw surprisingly large additions to U.S. all cotton production in the September WASDE compared to August. On the supply side, U.S. carry-in was raised 250,000 bales, month over month, reportedly to jibe with USDA AMS and USDA NASS data on 2021/22 ending stocks.

More dramatically, U.S. production was raised 1.26 million bales month over month. This is after a three million bale cut to forecasted U.S. production in the August WASDE. The higher production forecast was driven by a 1.31 million increase in planted acres. National average yield was lowered by three pounds per acre, and national average abandonment was unchanged at 43%. This effectively led to a forecast of 7.88 million harvested acres and 13.83 million bales of production.

On the demand side, domestic use was unchanged while forecasted U.S. exports were raised 600,000 bales, month over month. The bottom line of all this was a 900,000 bale increase in U.S. ending stocks, which is bearish, while remaining reasonably bullish in the resulting level.

For additional thoughts on these and other cotton marketing topics, please visit my weekly online newsletter at http://agrilife.org/cottonmarketing/.