John Robinson, Extension economist, cotton marketing

At a Glance

- Old-crop foreign production cut by 1.1 million bales

- U.S. old-crop exports raised by 400,000 bales

- New-crop U.S. production reduced by 500,000 bales

It’s a quadruple bull report for cotton, if you look at the June WASDE. No, that’s not an energy drink; it’s the World Agricultural Supply and Demand Estimates report. We are in that time of the year between May and July when USDA’s cotton supply and demand adjustments apply to four balance sheets:

old crop for U.S.

old crop for world

new crop for U.S.

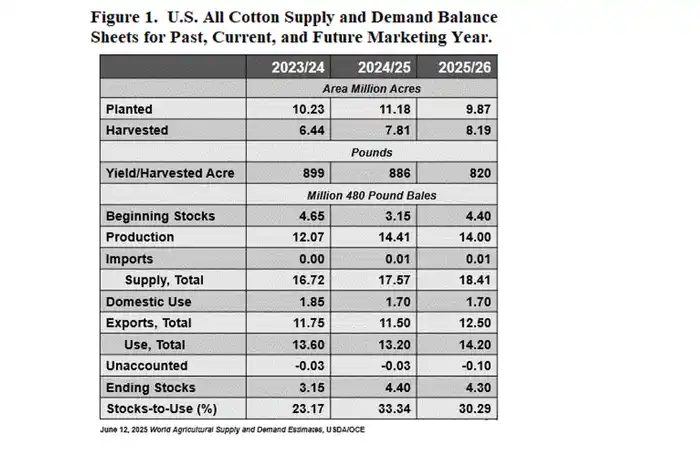

“Old crop” and “new crop” refer to the current 2024-25 and future 2025-26 marketing years, respectively. The U.S. balance sheets as of the June adjustments are shown in Figure 1.

USDA made bullish adjustments to all four balance sheets, which is unusual for the historically uneventful June WASDE report.

To begin with, old-crop foreign production was cut 1.1 million bales, with a corresponding 1.1 million-bale reduction in old-crop cotton ending stocks. This represents a modestly bullish adjustment.

This adjustment carries into the new-crop world balance sheet with 1.1 million fewer beginning stocks in the future 2025-26 world balance sheet. This was reinforced by an 820,000 cut in new-crop cotton production in the 2025-26 balance sheet. This represents almost a 2 million-bale cut in supply that dwarfed a 320,000 reduction in new-crop world consumption. The bottom line was a 1.58 million-bale reduction in new-crop world ending stocks. This is a more bullish adjustment.

U.S. adjustments

Focusing on the U.S. adjustments, old-crop U.S. exports were strongly raised by 400,000 bales, month over month, from 11.1 million to 11.5 million bales (Figure 1, middle column). That adjustment went straight to the bottom line with 400,000 fewer bales of old-crop ending stocks. This represents a modestly bullish adjustment to a less bearish year-over-year level.

The latter adjustment also means 400,000 fewer bales of carry-in stocks for the U.S. new-crop balance sheet.

On top of that, U.S. new-crop production was cut by 500,000 bales based on forecasted reductions in Delta yields and harvested acres. These adjustments combine for a whopping 900,000-bale reduction in supply, which went straight to the bottom line for a 900,000-bale cut in new-crop ending stocks. This is a hugely bullish adjustment, and it changes the year-over-year comparison of ending stocks from bearish (in May) now to neutral (Figure 1, middle and right columns).

Although Intercontinental Exchange cotton futures did not react very bullishly to this report. This could be a setup for a stronger market reaction in case the June 30 acreage report comes in surprisingly low. Such an event could trigger a long-awaited rally in December ’25 futures, especially if a number of the short-positioned hedge funds decide to cover their positions.

If that happens, and if December ’25 moves toward the mid-70s, I would not wait to take action with hedging or forward contracting. The normal seasonal pattern is for ICE cotton to weaken in mid- to late summer. So, time may not be on your side.

Robinson is with the Texas A&M AgriLife Extension Service. Visit his weekly online newsletter at agrilife.org/cottonmarketing.