Again the market was strong over the last week with July finishing at 88.80 c/lb, up 3.77 c/lb in the week.

Despite a strong cotton picture we should not forget the now critical situation in India with regards to Covid. The country reported over a million cases in just three days, with this just being the reported figure the real number is likely to be far higher. The government is however keen to keep factories open for now and so we do not expect any significant effects to consumption. Due to this, the Rupee also depreciated 4% in the last week and has therefore lead to some increased export demand with some cheap Indian offers in the market this morning. We wish our Indian friends all the very best through this tough period.

Despite the global covid situation appearing to deteriorate, the Dow Jones and S&P continue to go from strength to strength. The jobs market in the US continues to improve and is perhaps a contributing factor to the booming stock market. The number of Americans applying for unemployment aid fell last week to 547,000, a new low since the pandemic began and an encouraging sign that layoffs are slowing in an improving job market.

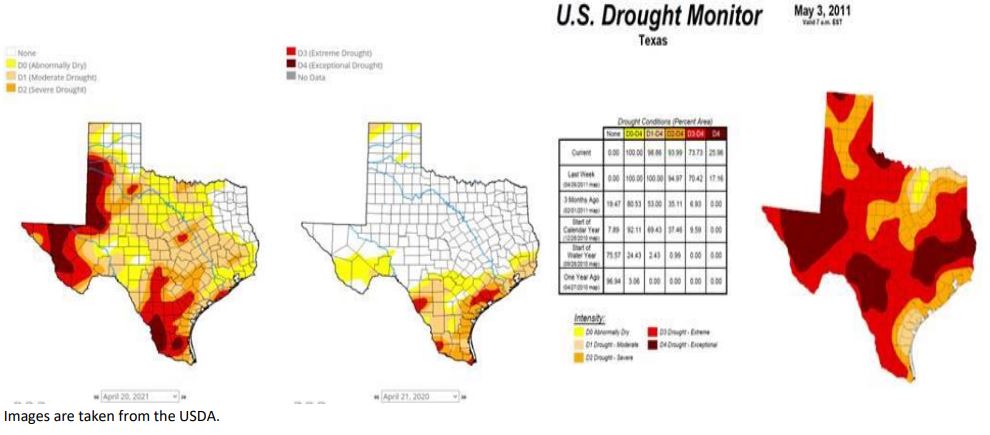

The recent rally has been two fold. The Soy and Corn markets have now hit contract highs for the year and therefore US farmers will no doubt look at these crops instead of cotton for better returns. There is also the continued drought in Texas which is of great concern. There is some rain due towards the end of the week but analysts suggest that it is not enough and the damage is done, even irrigated land will struggle this coming year. The picture below gives you an idea of how bad the drought is when compared with last year and then also the drought of 2011 in the third image. We shouldn’t forget that ICE is effectively a hedge of US cotton and therefore any negative affects to supply should be bullish ICE.

In Pakistan this week it was announced that a 10 billion rupee package would be available for cotton growers, giving subsidies on fertilizers, seeds and pesticides. The idea is to help revive the deteriorating cotton crop. Locally the fear is that these subsidies can be diverted to crops that are not cotton and Pakistan will continue with the same old and tiring seed, so yields will still be a major issue.

We saw last week plenty of West African tenders for current and new crop that were traded successfully. Burkina Faso reported this week that they are expecting a 36% increase in production to around 270k mt of lint, up from the 200k mt of lint they should produce this year.

Demand for cotton has again been relatively subdued as the higher prices have again forced buyers to the sidelines. That said, there is some enquiry for nearby shipments coming out of Bangladesh and Vietnam. The yarn prices have so far not followed NYF up and therefore buyer’s bids are not in line with market expectations.

The cotton charts look strong, and whilst demand is not excellent, it is the production side which is of greater concern, especially in the US. However, outside markets have dictated moves in the cotton market over the course of the year, continued COVID issues in Asia and new variants will keep investors on their toes and therefore the cotton market too.

Πηγή: Mambo