Since mid-May, ICE cotton futures have witnessed an historic short-term collapse (see this article https://southernagtoday.org/2022/07/what-is-behind-the-recent-cotton-futures-market-plunge/ ). In the two-month period between May 16 and July 14, the December ’22 contract fell over 49 cents. In the last 40 years, there have only been six December cotton contracts with more than that total level of change, measuring from the contract high to the contract low. The reason for the price decline has been attributed in the farm press and industry newsletters as “demand destruction” which is probably intended to mean both 1) a lower quantity demanded at the formerly high prices, and 2) an inward shift in demand in response to recessionary expectations.

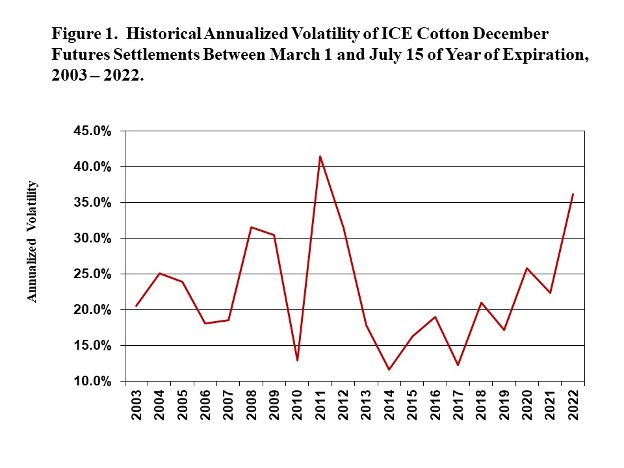

Besides the major downward trend of this price movement, it is also associated with high volatility. By volatility, I mean that prices are gyrating more variably and more quickly. Historical volatility is a measure of the spread or risk of price movements over a defined period. Figure 1 shows historical volatility in ICE December cotton futures during the period March through Mid-May. The underlying measure of dispersion used in Figure 1 is the standard deviation of December futures settlements.

Contributing to the high volatility of the December ’22 contract were the strong price moves higher and lower, including many limit up and limit down moves. Figure 1 indicates that the volatility of the December ’22 prices is approaching that of the notable price rally of 2010-11, which then reverted to more normal prices, a pattern that economists call “mean reversion”. Like 2010-11, the current price movements will likely become smoother and less volatile, but perhaps not until the post-harvest season. (Note: the 2010-11 price spike was triggered by a global supply shortage that was several years in the making. In contrast, the 2021-22 price spike appears more demand driven.)

The plunge in cotton futures represents a lost opportunity for growers with unsold or unhedged production this year. The contribution of high volatility also increases the costs of marketing since more variable price moves increase the costs for growers or for merchant buyers of simpler hedging strategies. The experience of high volatility in 2022 should serve as a reminder to growers about the riskiness of cotton price movements.