Το περιεχόμενο του άρθρου δεν είναι διαθέσιμο στη γλώσσα που έχετε επιλέξει και ως εκ τούτου το εμφανίζουμε στην αυθεντική του εκδοχή. Μπορείτε να χρησιμοποιήσετε την υπηρεσία Google Translate για να το μεταφράσετε.

Cotton futures continued to fall during a busy, data-driven week.

Cotton Market Weekly April 12, 2024

May futures settled at 83.37 cents per pound, finishing 377 points lower for the week.

With May First Notice Day less than two weeks away, the July contract will start to take focus. July futures settled at 85.25 cents per pound, finishing 332 points lower for the week.

Fundamental, technical, and macroeconomic news kept the market moving this week. Selling pressure came from continued speculative liquidation, index rolling, and rain in West Texas. The May and July contracts crossed below the 200-day moving average.

Daily volumes were heavy this week as major indexes continued to roll their positions forward. Total open interest decreased by 47,480 contracts to reach a balance of 233,271.

Certificated stocks have reached their highest level since June 2021. They were last reported at 155,045, an increase of 62,391 from the week prior.

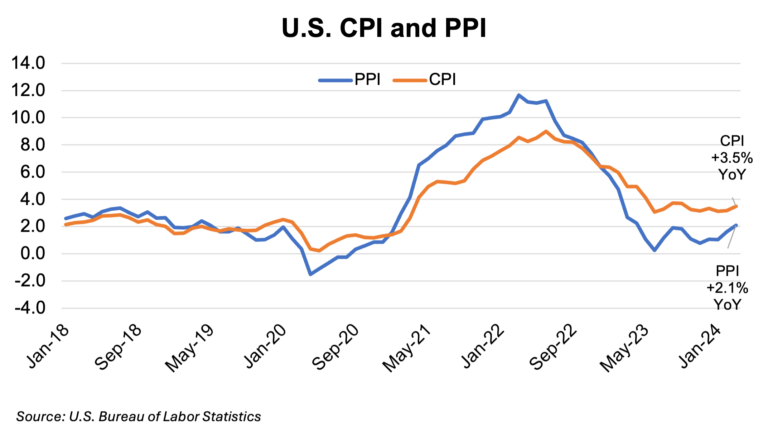

The U.S. Consumer Price Index (CPI) came in hot, prompting questions on how many interest rate cuts will happen this year.

CPI increased 3.5% year-over-year, rising more than expected, causing a sell-off on Wednesday.

The Producer Price Index (PPI) came in slightly below expectations, rising 2.1% year-over-year. This helped markets recover from Wednesday’s sell-off, but the gains were limited due to lower weekly jobless claims.

The European Central Bank kept interest rates unchanged for April but signaled cooling inflation should allow interest rates to be cut soon.

After the stronger-than-expected inflation data, the U.S. Dollar rallied to an almost 5-month high this week, putting additional pressure on commodities.

U.S. export sales and shipments remain steady for the week ending April 4.

A net total of 81,500 Upland bales were booked, and 274,100 bales were shipped during the reporting period.

A total of 48,900 bales were cancelled this week, 24,400 from Turkey and 11,000 from China.

New crop sales of 35,700 bales continue to be below the average typically sold at this point in the year.

A net total of 1,400 Pima bales were sold, and 5,200 bales were shipped for the week.

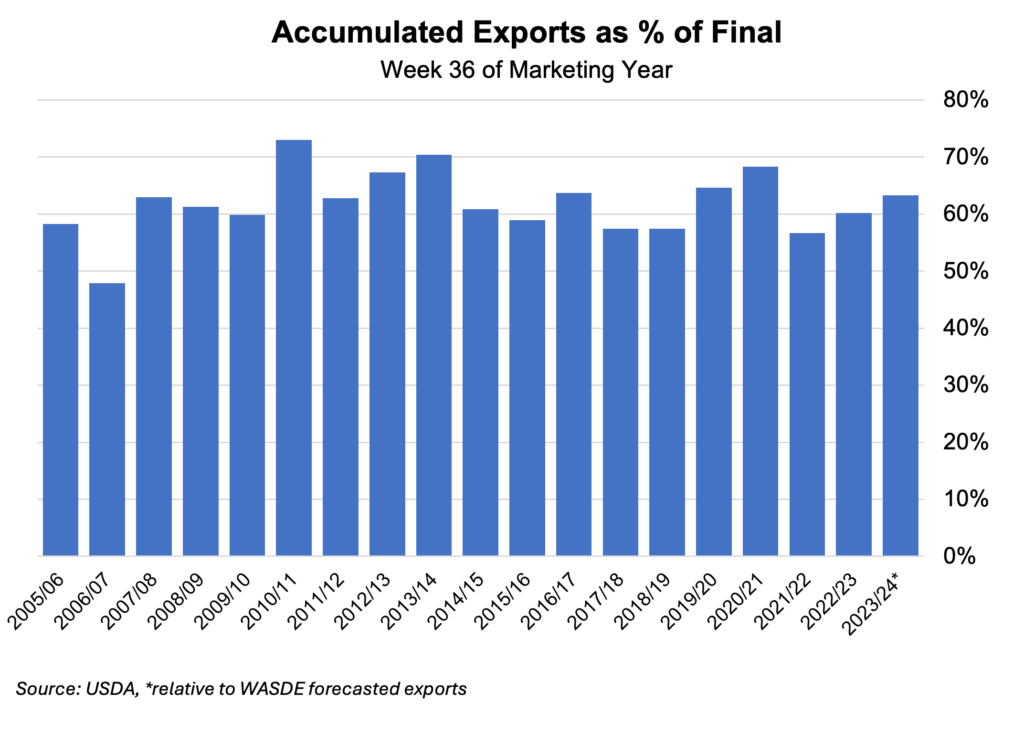

The April World Agricultural Supply and Demand Estimates (WASDE) release was lackluster, with the U.S. side of the balance sheet unchanged.

U.S. production was held at 12.1 million bales, exports kept at 12.3 million bales, and ending stocks at 2.5 million bales. Significant changes to the U.S. side do not typically occur in the April report, so this report was as expected.

For the world side of the balance sheet, consumption decreased by 120,000 bales to 112.82 million bales. Ending stocks were also lowered by 260,000 bales to 83.08 million bales.

The Week Ahead

Next week is the last full week of trading before first notice day of the May contract, which is on April 24.

The U.S. Export Sales Report will remain a central focus, but the Crop Progress Report will move back into rotation of normal weekly reports for traders to review.

After a busy, data-filled week, next week’s news will be light. U.S. retail sales for March will be released on Monday.

Planting continues in South Texas, and the cotton that has emerged in the most southern areas benefited from the moisture. The precipitation that fell in other areas in the Southwest was much needed.