MAY 14, 2021

EXPORT SALES REMAIN SLOW, ALL EYES ON UPCOMING REPORTS

- Additional Pressure Placed on Export Commodities

- U.S. Ending Stocks Forecast Falls 600,000 Bales

- Export Sales Remain Relatively Slow

- 25% of Expected Cotton Acreage Has Been Planted

Prices slid every day but Wednesday this week. Last Friday’s July high at 91.00 cents per pound was the high and Thursday’s close at 84.98 cents was just 23 points over the low. From last Thursday’s close, July futures fell 560 points. Open interest climbed 7,325 contracts even as prices fell, finishing the week at 229,779. Daily trading volumes were healthier on active trading surrounding the release of economic data, the USDA’s May WASDE report, and Thursday’s Export Sales.

OUTSIDE MARKETS

April’s Consumer Price Index (CPI), a core gauge of inflation, was a bombshell on Wednesday. Consumer prices were higher than expected, rising 0.8% from March and 4.2% from April of last year. Producer prices were released Thursday and were in line with the jump in consumer prices. While last week’s disappointing jobs report appeared to give the Federal Reserve cover to keep up asset purchases and accommodative (low) interest rates, this week’s inflation data was a strong counter-point. Upon seeing the CPI data, investors immediately sold out of stocks and other risk assets, including commodities, on bets that the surge in inflation will force a tightening of monetary policy. The U.S. Dollar also jumped higher versus other major currencies, which put additional pressure on export commodities like cotton, corn and soybeans.

WASDE

Just after the CPI figures came out on Wednesday, agricultural commodity traders also had to contend with the release of the May WASDE report. This month’s report gave the first look at USDA expectations for the 2021/2022 balance sheet in addition to continued revisions of the outgoing marketing year. For 2020/2021, notable U.S. revisions included reducing the crop by 90,000 bales to 14.61 million and lifting exports to 16.25 million bales, consistent with the high level of U.S. export commitments this year. The U.S. ending stock forecast for this year fell 600,000 bales to 3.3 million.

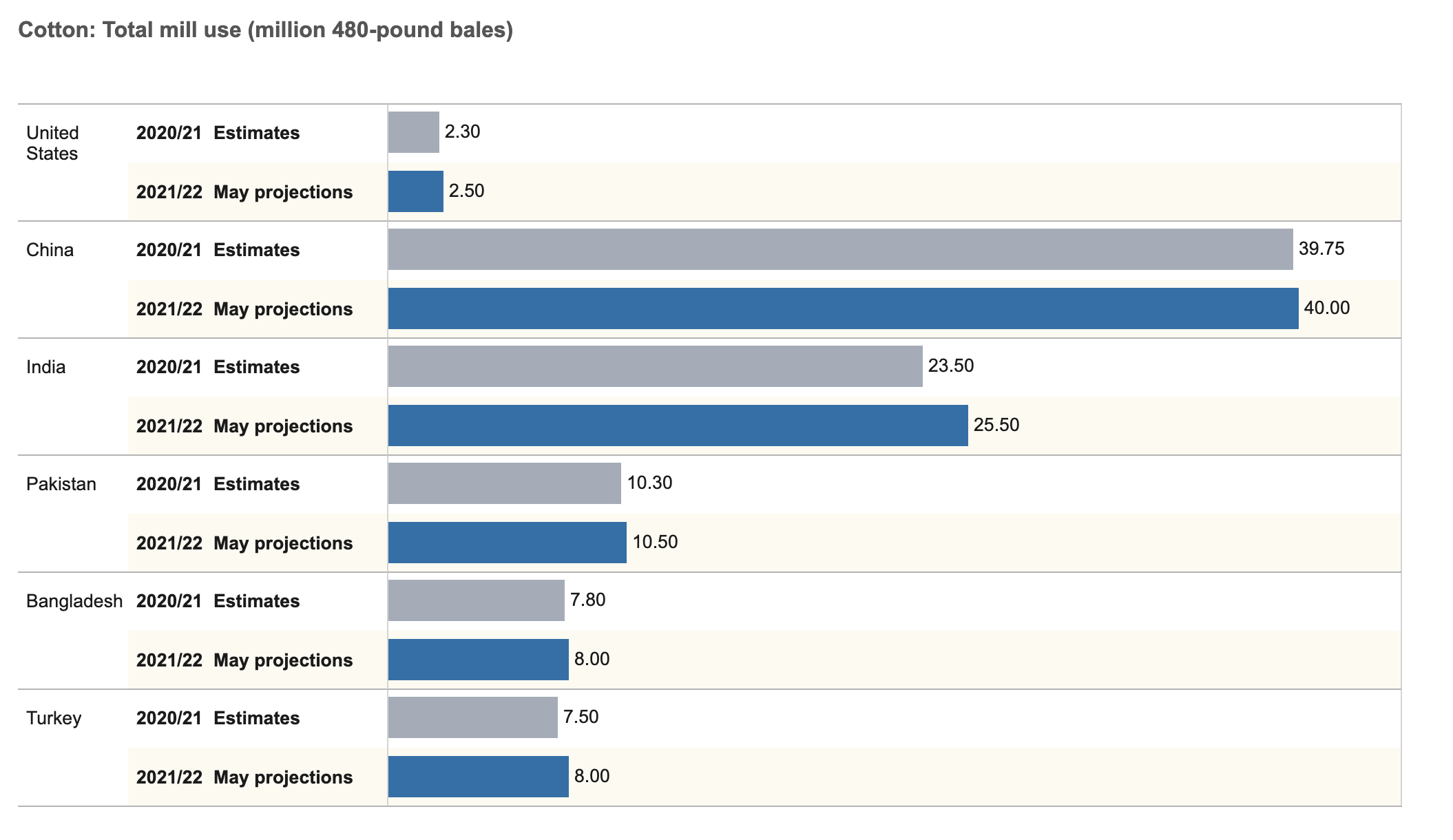

The initial U.S. balance sheet for 2021/2022 pegged this year’s production at 17.0 million bales, which reflected a relatively high abandonment expectation for the Southwest based on the drier and warmer bias on the seasonal outlook and remaining drought. With the 3.3 million bales of beginning stock, total U.S. supply may be the lowest since 2015/16. U.S. exports are forecast to be 14.7 million, down from this year on the lower supply outlook. Ending stocks were forecast to tighten even further to just 3.1 million bales. Globally, the USDA expects production to rebound to 119.4 million bales from this year’s 113.1, while consumption is expected to increase four million bales to 121.5. World stocks will tighten to 91 million bales, but most of the excess stocks are likely to be in the hands of government entities in China and, to a lesser extent, India.

EXPORT SALES

Export sales last week remained relatively slow as they have for the past month, but net new sales were still at the average pace needed to hit the USDA’s increased forecast with enough room for carryover sales. For the week ending May 6, U.S. shippers booked another 54,400 net bales of Upland for the 2020/2021 marketing year and another 72,100 bales for delivery in 2021/2022 (after July 31). Pima sales were 3,800 bales for this marketing year and 200 for next. Shipments were lower than last week, but were still fairly healthy at 296,500 bales. Accumulated exports have reached 12.17 million running bales which is the highest level ever for this point in the marketing year.

CROP PROGRESS AND WEATHER

According to this week’s Crop Progress Report, 25% of the expected cotton acreage has now been planted. While there are a few states that are pretty far behind, the Beltwide average is only 1% behind the five-year average. We now have some hope that West Texas will be able to plant in a timely manner as the current forecast for rain for the Southwest is as good as at any time in months. The models are calling for 3-5” for Oklahoma, Kansas, and much of the Rolling Plains. The 0.5-1.25” in the forecast for the Southern High Plains are less than we would like, but we welcome it. Beyond these rains, the seasonal forecast for June, July, and August has a drier and warmer bias.

THE WEEK AHEAD

Traders will be watching whether the weather forecast materializes over the weekend and into next week. With the WASDE behind, next week’s Crop Progress and Condition Report and Export Sales Report are a central focus.

IN THE WEEK AHEAD:

- Friday at 2:30 p.m. Central – Commitments of Traders

- Monday at 3:00 p.m. Central – Crop Progress and Condition

- Thursday at 7:30 a.m. Central – Export Sales Report

- Thursday at 2:30 p.m. Central – Cotton-On-Call