August 19, 2022

- Macroeconomic Volatility Still Roiling Markets

- Weak Foreign Demand for U.S. Cotton

- Prospects for Rain Over the Next Week

December futures started the calendar week with a large gap higher following Friday’s limit-up close at 108.59 cents per pound on the back of last week’s bullish WASDE Report. The opening price Sunday night was 111.53 cents and futures traded right to limit up once again on Monday, locking at 113.59. Although futures did touch limit up at 119.59 on Tuesday, the historic rally seemed to find some equilibrium as the market began to backfill much of the area that it had simply run past on Monday. By Thursday’s settlement, prices had traded as low as 111.71, but finished our Thursday-to-Thursday reporting week at 112.70, up 811 points. While volume was clipped by being locked limit-up early in the week, Tuesday and Wednesday’s volume set records for this time of year with traders scrambling to adjust their positions on the extreme move. Market participation climbed to its highest level since June, with open interest gaining +9,426 to 197,504.

Outside Markets

Equity markets were a bit more two-sided this week. Recent economic data exemplify the sticky situation that the Federal Reserve faces. While the housing sector continues to underperform analysts’ expectations, other key indicators such as jobless data and retail sales are performing better. Broader market sentiment seems to be flip-flopping based on whether or not the Fed looks likely to continue raising rates, and investors are re-positioning with each new data point. Unfortunately, economic weakness in China and Europe are only complicating the picture. Macroeconomic volatility is still roiling markets.

Export Sales

Last week’s foreign demand for U.S. cotton was very weak for this time of the year. U.S. shippers made net new sales of just 49,500 bales of Upland and 300 bales of Pima. On the other hand, unshipped sales are over 7 million bales versus an expected crop of just 12.6 million, leaving 56% of production already committed to exports. After expected U.S. consumption of 2.3 million bales, there may be only 6 million bales left to split between ending stocks and new export sales for the rest of the year. In other words, the market can afford for export sales to be slow for a little while. Whether or not tepid demand outlasts short supply is a question we’ll all have to wait to see, but for now the Export Sales Report is a little less important than usual.

Crop Progress and Weather

Prospects for rain over the next week are the best they have been in many months. How much moisture will actually hit the right areas and how much good it will do are still subjects of speculation, but the rain is definitely welcome if for nothing more than getting a cover crop in. At a national level, the crop is now just 15% open, with most of that in South Texas, Louisiana, and Arizona. Eighty percent of the crop is now setting bolls, slightly ahead of average. Among the states, the Southeast region appears to be in the best shape. Overall, just 34% of the U.S. crop is rated “Good” or “Excellent.”

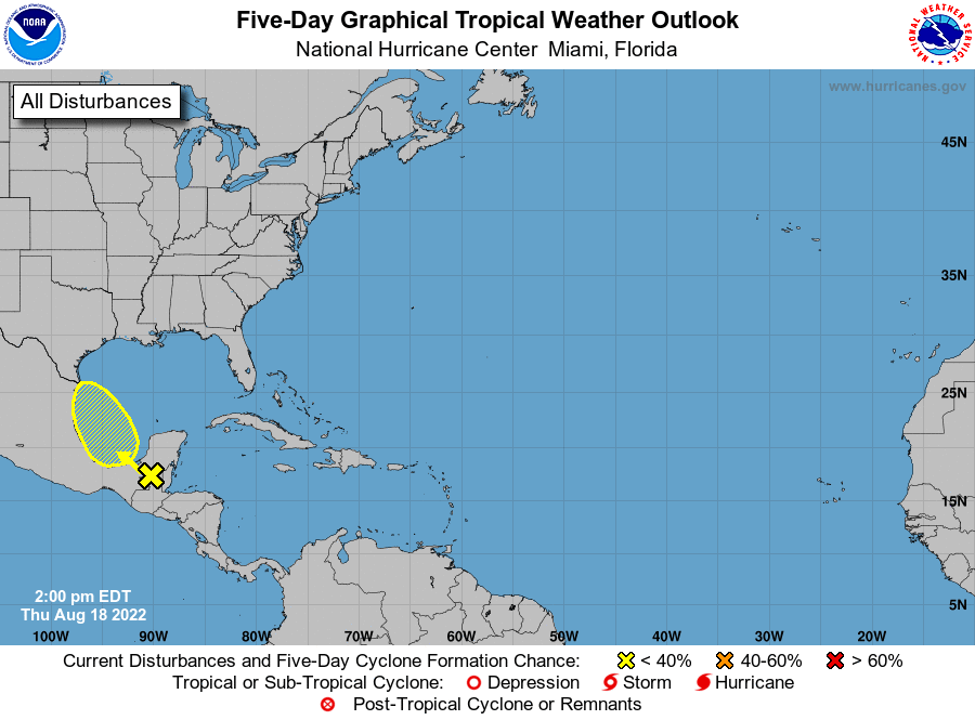

The Week Ahead

With GDP figures expected next Thursday, rain across the Cotton Belt will not be the only key factor that traders are watching. Keep an eye on potential hurricanes in the Atlantic and Gulf of Mexico, including the potential system that is already in the five-day outlook.

- Friday at 2:30 p.m. Central – Commitments of Traders

- Monday at 3:00 p.m. Central – Crop Progress and Condition

- Thursday at 7:30 a.m. Central – Export Sales Report

- Thursday at 7:30 a.m. Central – U.S. GDP and Personal Consumption

- Thursday at 2:30 p.m. Central – Cotton On-Call