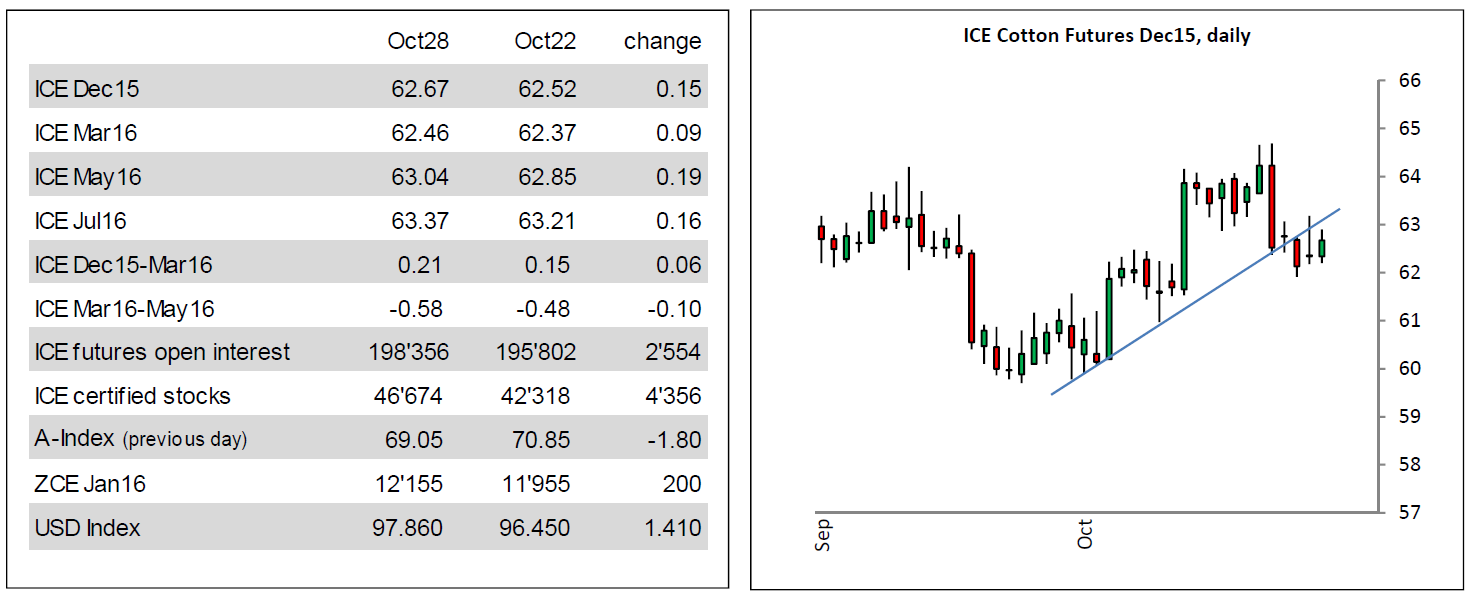

ICE Cotton Futures

Unlike some other markets, e.g. the US$, crude oil and equities which all engaged in strong moves, cotton futures have experienced a very much uneventful week. Following last week’s strong decline from this monthΆs high, futures prices have been content to engage in some back and forth trading within a just 100 points wide trading range.

The lower levels have uncovered quite good mill demand for mostly near-term deliveries. This has helped to prevent futures volume from being very light.

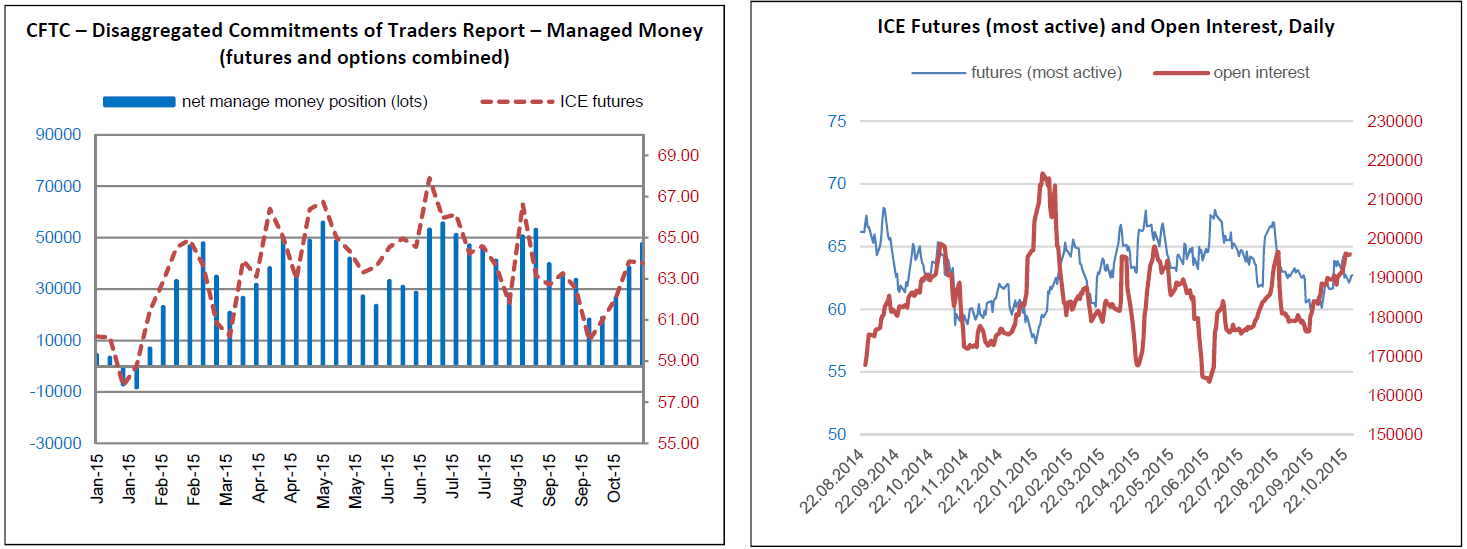

The open interest continues on its trend higher and will most likely break the 200Ά000 lots mark soon. Currently it stands at its highest level since February of this year. Fresh commercial short hedges should be the main contributor to this at the moment. During the past weeks managed money funds have been increasing longs and liquidating shorts. Their net long exposure has increased from about 18Ά000 to 48Ά000 lots between Sep 22nd and Oct 20th. Given that this long position is very close to the highest levels registered this year so far it may serve as a short-term warning signal for bulls.

Technical picture: Support is between 62.00 and 61.70. Settling below 61.70 sets 61.00-60.50 as minimum down-side objective. Resistance is at 63.20, 64.00 and key at 64.70.

India

The Cotton Association of India (CAI) has released its September estimate of the cotton crop for the 2015/16 season (period October 2015 to September 2016). The CAI has estimated cotton crop output for the season 2015/16 at 37.050 million bales (170 kgs each) which is by 1.225 million bales lower than the 2014/15 crop estimate. The CAI estimates further a total domestic consumption for the season 2015/16 of 32.500 million bales, while the total cotton supply is estimated to be 46.31 million bales. The result is an available surplus of 13.815 million bales. Exports business continued into Pakistan, Bangladesh & Far East markets, with price range USC 65-66 per LB CFR for standard G5 quality. Daily arrivals improved further and are now at around 75,000 bales. The total new crop arrivals now stand at 1.31 million bales, higher by 0.5 million bales compared to the same period of last year.

China

While harvesting is progressing fast and ginning is actually ahead of last year, selling of new crop domestic cotton is extremely slow. Prices for nearby physical cotton are coming down but are still well above parity to the ZCE futures market. Most of the cotton is still in farmersΆ hands. Expectations in the market are overwhelmingly bearish, while physical cotton isnΆt moving; as a result, the inverse between January and May contracts has widened further. According to latest reports, quality of machine picked cotton mainly of Northern XJ is hardly worse than the handpicked cotton, and the price discount has narrowed to about 2.50 c/lb. Since machine picking is much cheaper, that will add to the incentive to switch even more to mechanization next season.

As reported last week, some re-distributed quota has become available which led to a moderate picking up of import business, but still mostly for nearby lots. Spinning mills and the entire textile chain continue complaining about very bad business conditions, and for the time being there is no improvement in sight.