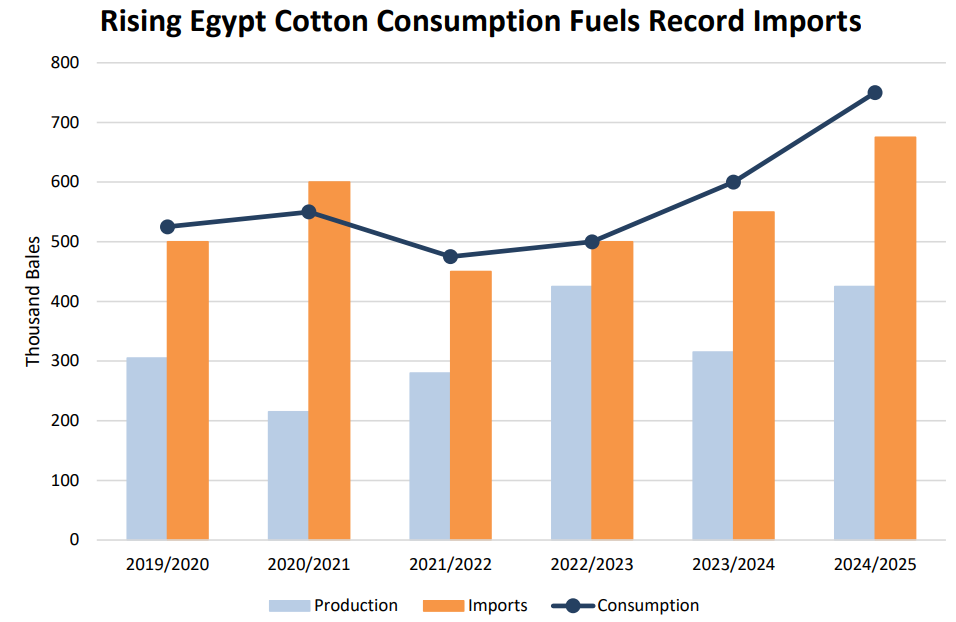

Egypt cotton consumption is projected at 750,000 bales in marketing year 2024/25 (August 2024 – July 2025), the highest level in 14 years, driven by a new wave of public and private investment. Imports are forecast at a record 675,000 bales to meet the demand of rising consumption since domestic production has stagnated over the past decade.

Egypt has historically been a prominent producer and consumer of cotton but now consumes less than half the peak volume reached in 1992/93. In recent years, the government has revitalized the industry by investing more than $1.1 billion in the state-owned textile company as part of a plan to use more cotton domestically rather than export it.1 The government also adopted policies to incentivize foreign investment such as establishing the Suez Canal Economic Zone with lower taxes and a pro-business environment.

Foreign companies are also drawn to Egypt by lower labor and energy costs and proximity to the EU market, the second largest importer of cotton products. In the past year, foreign investment from China totaled approximately $1 billion covering all stages of textile production.2 Multiple Turkish textile companies have also recently announced plans to build new spinning mills in Egypt. As additional spinning capacity from public and private investments materializes over the next few years, Egypt cotton consumption is projected to rise. Egypt has already jumped from the 16th largest cotton consumer last year to tie for 13th in 2024/25, if current forecasts are realized.  Egypt has relied on imports to support increasing consumption as domestic production stagnated in recent years and the government more than doubled the guaranteed farm price in 2024/25 despite falling global prices. 3 According to Egypt’s Cotton Arbitration & Testing General Organization (CATGO), just 50,000 bales of domestic cotton have been distributed to local mills so far this marketing year, roughly equal to recent years, despite higher consumption. This contradicts the government’s intention to redirect domestically produced cotton from exports to local mills.

Egypt has relied on imports to support increasing consumption as domestic production stagnated in recent years and the government more than doubled the guaranteed farm price in 2024/25 despite falling global prices. 3 According to Egypt’s Cotton Arbitration & Testing General Organization (CATGO), just 50,000 bales of domestic cotton have been distributed to local mills so far this marketing year, roughly equal to recent years, despite higher consumption. This contradicts the government’s intention to redirect domestically produced cotton from exports to local mills.

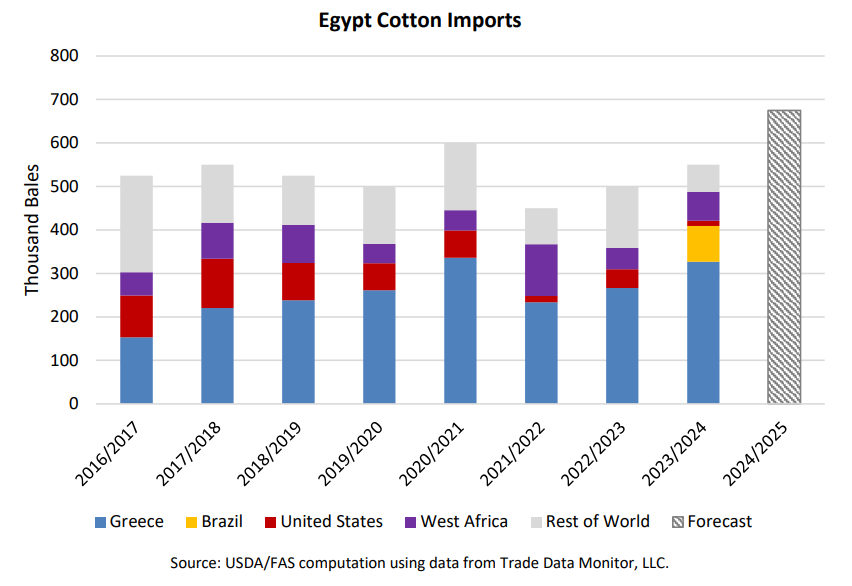

Greece is the principal source for Egypt cotton imports, accounting for more than half of market share during the past decade. The United States has historically been a top supplier with Pima cotton serving as a substitute for Egyptian extra-long staple (ELS) varieties while West African and Sudanese supplies have met the demand for more affordable upland cotton.

In 2023/24, Brazil became the second largest supplier after gaining market access in 2022/2023. In the first 7 months of 2024/25, Brazil export volume tripled compared to the same period last year as it continues to offer a lower price compared with competitors. Brazil remains the second largest supplier this year behind Greece which has seen less dramatic but still notable growth of 60 percent year over year. As a result of this growth from top suppliers, Egypt cotton imports are forecast at a record 675,000 bales in 2024/25. In contrast, U.S. cotton has lost market share to more affordable suppliers. FAS Export Sales Reporting shows sales of less than 1,000 bales of upland cotton for 2024/25, compared to the 10- year average of nearly 50,000 bales. This reflects Egypt’s expansion from a niche supplier of specialty cotton products to a more significant textile producer that competes on price with other textile producing countries.

Πηγή: USDA-FAS