Our thoughts and prayers go out to everyone, but especially our fellow farmers and cotton producers in North Carolina, South Carolina and Virginia.

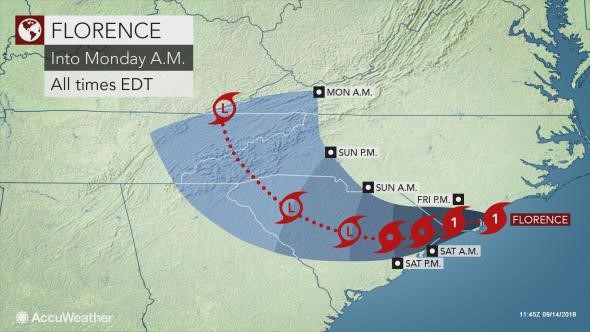

The very latest projected path of the storm (as of the morning of September 14), takes it along the NC coast, then inland across virtually all of SC. The storm is slow moving, meaning that it will dump a lot of rain and there will be high winds for several days.

Accumulated rainfall from this storm is expected to total 12-18 inches or much more in some areas and accompanied by high winds. Most areas, even if not in the most heavily impacted area, are expected to receive totals of 5-12 inches of rainfall.

It looks like Georgia may be fortunate to escape the brunt of any major impact on crop production:

“I am relieved to say that with the current path of the storm, impacts on most of Georgia are now expected to be minimal. Eastern counties will still experience some wind gusts from the storm which could cause isolated power outages, but they are expected to be less than 40 mph. Rainfall will be confined to the northeastern part of the state and should amount to less than two inches in all. The rest of the state should see no rain at all from the storm, which is not good for areas that are currently suffering from dry conditions. The southern half of Georgia should not experience any significant impacts from the storm and northern Georgia’s impacts will be small and limited in space and time.”

Pam Knox, UGA Agricultural Climatologist, September 14, 2018

NC, SC, and VA are currently forecast to produce a total of 1.58 million bales of cotton this year. Recognizing the location of most cotton production in these states (this is 2017 county production; VA is not shown I assume to avoid disclosure of individual farms), it appears that SC cotton will be subject to heavy rainfall, as well as NC. VA will receive less and east GA mostly 1-2 inches or less.

As we experienced with Irma here in Georgia last year, the damage from sustained high wind can be significant, resulting not only in lost lint from open bolls, but also twisted and lodged plants difficult to harvest. As of September 9, the NC crop was 43% open, SC 28%, and VA 37%.

Market Update

The visions of a return to 90-cent cotton appear to be fading. The good news is that the market is clearly showing signs of good support at roughly 82 cents. Support is a good thing. But prices (December futures) have struggled to clear a hurdle at 85 cents – we’ll first have to clear 85 if we hope to reach 90. For producers looking for an opportunity to add on to earlier sales, support is good, but a rally is even better.

USDA’s September estimates raised the U.S. crop to 19.68 million bales – 440,000 bales higher than the August estimate. The 2018 forecast yield was lowered just a bit, but acres planted was raised 520,000 acres.

The U.S. crop is still a big unknown. This is one thing giving us support. Texas, as of September 9, is 62% poor to very poor condition. The September USDA numbers lowered the Texas state average yield to a projected 694 lbs/acre – down from 726, but added roughly 200,000 more acres to be harvested.

U.S. exports projected for the 2018 crop year were raised 200,000 bales from 15.5 million bales to 15.7 million. World demand is strong, but there is some skepticism within the industry about whether or not USDA is over-reaching a bit on its export number. 2017 crop year exports were 15.85 million bales.

Compared to the August estimates, China’s production for this season was raised 1 million bales, India production was unchanged, Australian production was cut 550,000 bales, and Brazil was raised 500,000 bales. Chinese imports and use were unchanged, as were Bangladesh and Vietnam imports.

Although prices appear to have good support, producers should be 50% sold or better at this point. The current level of prices (in the 82 cent neighborhood) is disappointing compared to where we have been. But if you’re not already at the 50% level, you also need to think about guarding against this market going to less than 80 cents and you being at-risk with most of your crop.

On the other hand, if you are already 50% or more priced, rallies to the 85 cent area could be a good opportunity to add further to sales – unless you want to take the risk of holding out for 85 to 90 – but then realizing you’re also taking the risk that the current level of support will hold.

Πηγή: Cotton Grower