Old crop July futures has now lost 3.75 cents since the recent “peak” at over 57 cents on April 30. New crop December futures has declined 3.5 cents after reaching almost 59 cents on April 30.

It now appears we will test a likely range of 52 to 57 cents until the next “mover” comes along. July should have support (keep our fingers crossed) at 52 cents and, should we begin to trek up again, 58 will the hurdle to negotiate.

What does all that mean? If you’re holding cotton – and I know some of you are – the LDP or MLG will give you protection if prices head further south. Relax. The LDP/MLG will decrease as price approaches 59 cents and zero out above that. If you’re still holding cotton, your equity should increase during a week that the market is improving while and before the MLG changes effective on Friday.

Reports and observations from various sources suggest that the recent weakness has developed due to concerns that another round of ill-will between the U.S. and China may break out over the coronavirus pandemic – one that could work against the intentions of the Phase One trade agreement.

Last week’s export report was a good one – and one reason for the rally before late week and this week’s losses. Sales for the week ending April 23 were 448,300 bales and shipments were 268,500 bales. Shipments need to average approximately 307,000 bales per week to meet USDA’s now lower projection of 15 million bales for the 2019 crop marketing year.

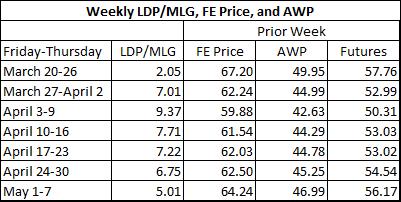

The LDP/MLG is currently 5.01 cents through close of business on May 7. Given this week’s downturn in prices, the LDP/MLG may increase, but this is subject to what happens on Wednesday and Thursday to round out the week.

Since LDP’s/MLG’s began back on March 20, nearby cotton futures have averaged mostly 8 to 9 cents below the FE Price. The AWP is the FE Price minus 17.25 cents for transportation and quality adjustments. Likewise, the AWP averages 8 to 9 cents below nearby futures. So, what’s the point? An LDP/MLG is in effect when the AWP is below 52 cents (the base Loan rate). That would be when our futures prices are approximately 60 cents.

This is why when you look ahead and plan for 2020, market signals below 59 to 60 cents are not relevant to your decision making. Why? Because when prices dip below 60 cents, the LDP/MLG is going to kick in – if futures are 57 cents + 3 cents LDP/MLG = 60; if futures are 50 + 10 cents LDP/MLG = 60. Your worst-case scenario is 59 to 60 cents basis the futures because of how Marketing Loan mechanisms and price relationships work.

Let’s suppose the LDP/MLG is 6 cents for the week ending on a Thursday. Now, let’s suppose prices have gone up during the week. The new LDP/MLG effective on Friday will decline. If you are planning to sell, do so while prices are up and before the LDP/MLG declines. If prices are declining, the LDP/MLG will increase to protect you unless you have already “POPed” the cotton or no longer have beneficial interest.

May 31 is the deadline to put cotton in Loan or take an LDP in lieu of Loan. The market is concerned about demand/use, both now and what it will look like post COVID-19. Good export reports are a help, but not necessarily a longer-term solution.

Dr. Don Shurley is professor emeritus in the Department of Agricultural and Applied Economics at the University of Georgia, Tifton.

Πηγή: Cotton Grower