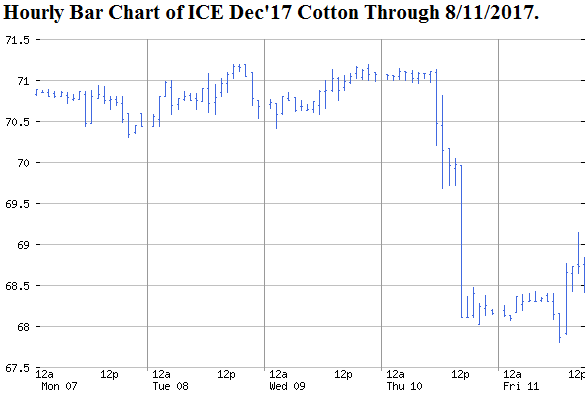

The week ending Friday August 11 saw uneventful sideways pre-WASDE trading in the recently established 70.50 to 71.00 cent range. Then a surprisingly large U.S. cotton production forecast by USDA on Thursday apparently shocked traders and sent the market limit down in high volume. Friday saw a slight recovery with Dec’17 settling up fourteen points at at 68.25 cents per pound. The initial market reaction and stabilization is not unusual considering how much uncertainty remains in the production and ending stocks outcomes. Deep in-the-money 73 and 75 cent put options on Dec’17 settled Friday at 5.71 and 7.35 cents per pound, respectively. Meanwhile, near-the-money 66 and 67 cent puts on Dec’17 settled Friday at 1.55 and 1.96 cents per pound, respectively. 73 and 79 cent call options on Dec’17 settled Friday at 0.96 and 0.25 cents per pound Chinese cotton and world prices modestly increased most of this week.

Other cotton specific news this week included a weak export sales report. In addition to recent questions/concerns about major flooding in India, there were new reports this week of pink bollworm infestations and potential damage.

Since we are in an uncertain weather market situation, growers should be poised and ready to quickly take advantage of any unexpected price rallies. Forward contracting and/or various options strategies can be used to limit downside risk while retaining upside potential. Physical bales that have been forward contracted could also be combined with call options on Dec’17 ICE cotton. For example, while an out-of-the-money 73 cent Dec’17 call costs 0.96 cents per pound (circa August 11), a 73:79 Dec call spread would cost a little cheaper at 0.71 cents. A relevant strategy to look at for unsold/uncommitted 2017 bales would have been buying put spreads on Dec’17 futures back when they were trading in the lower to mid 70s. This could still be a relevant strategy if some unexpected event rallies Dec’17 futures back into the lower to mid 70s.

Source: http://cottonmarketing.tamu.edu/