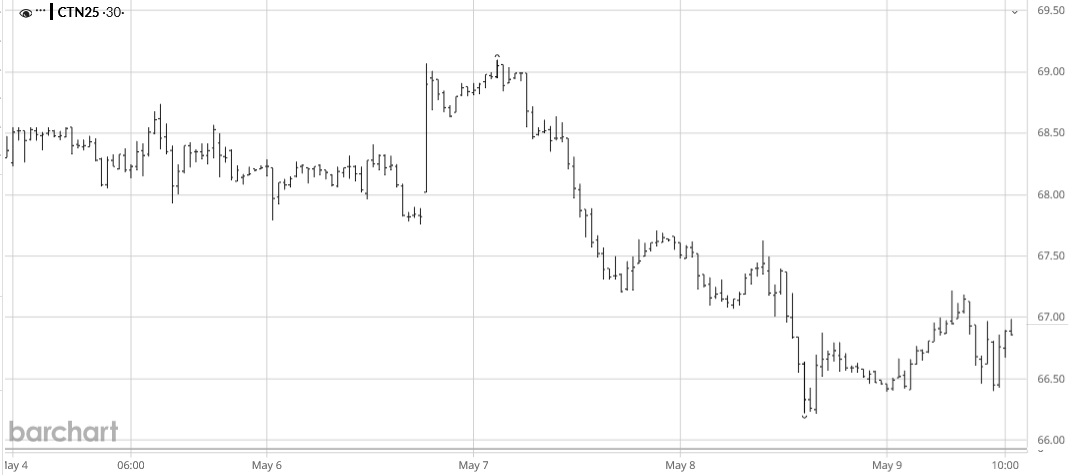

For the week ending Friday, May 9, ICE cotton futures followed a gradual-turning-bumpy downward path and down over two cents from Wednesday’s intraday highs (see chart above courtesy of Barchart.com). Jul’25 ICE cotton settled Friday at 66.61 cents per pound, while new crop Dec’25 settled the week at 68.67 cents per pound. Chinese cotton prices were flat-to-higher across their holiday-shortened week. The A-Index of world cotton prices followed a modest down-trend, resembling ICE cotton.

In other ag markets, the most active CBOT corn and soybeans, as well as KC wheat futures, all followed a similarly bumpy down-trend as ICE cotton. The U.S. dollar index traded flat-to-lower before rallying Thursday on improved expectations of trade negotiations and bullish U.S. employment numbers. Longer term, it is an open question whether the U.S. Dollar Index is bottoming after stair-stepping lower all spring. Other macro influences (i.e., GDP, inflation, and interest rate policy) remained mixed in their expectation and implication.

Cotton-focused market influences this week included continued reports of mostly light regional demand. The only active spot trading was in the West Texas-Kansas-Oklahoma region where there are moderate supplies left to trade. The week saw poor U.S. export net sales reports through May 1 (during which the Jul’25 contract was cheapening). The pace of 2024/25 export shipments continued above the weekly average level needed to reach USDA’s target level of exports (10.9 million bales). Probably all of the projected U.S. old crop production is ginned and classed as of early April (final classing report is due May 12).

For the week ending May 8, the day-to-day shifts in ICE cotton open interest were mixed, i.e., increasing and decreasing. As of May 6, the regular weekly (Tuesday) snapshot of speculative open interest showed long positioning in the form of 631 fewer hedge fund shorts and 1,717 more hedge longs, week over week. All this was reinforced by a 2,692 contract expansion in the index trader net long position, week over week.

The dynamics of ICE cotton futures may also represent a wet blanket on the market. It remains true that unfixed call sales (by mills) are at an historically low level, perhaps reflecting the cautionary buying on the demand side. In terms of ratios, unfixed call purchases (by suppliers) outweigh unfixed call sales by almost two-fold across all contracts, as of April 4.

For more details and data on Old Crop and New Crop fundamentals, plus other near term influences, follow these links (or the drop-down menus above) to those sub-pages.

Πηγή: TAMU