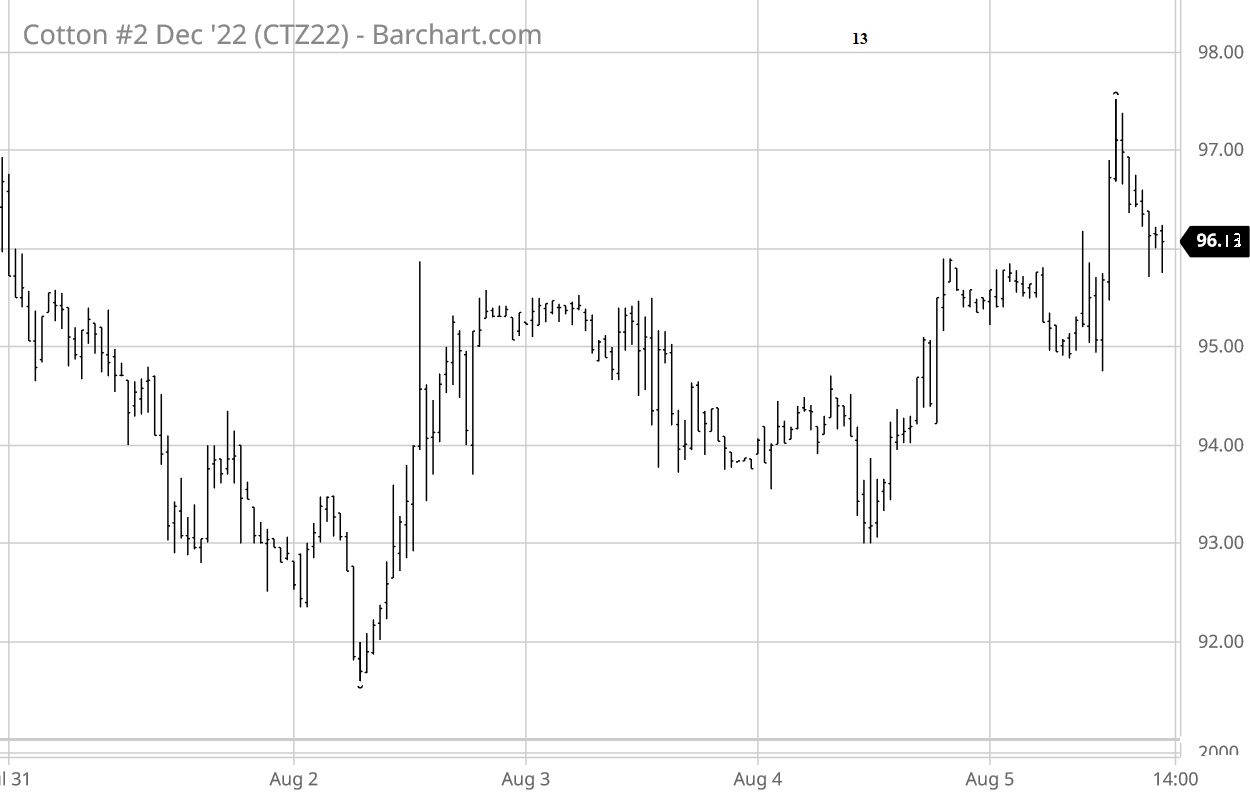

The week ending Friday, August 5 saw ICE futures zig-zag through a dip-recovery and then take several steps up (see chart above courtesy of Barchart.com). The Dec’22 contract settled at 96.13 cents per pound on Friday, up a cent and a half on the day, but down 61 points week over week. Chinese cotton prices were mixed this week along with the A-index.

Cotton-specific influences this week included some significants rains over New Mexico and the Texas High Plains, as well as across the Delta region. Texas still languishes under drought conditions, reinforced by continued hot/dry weather. August rainfall won’t end the drought, but it could benefit the yield potential of surviving cotton that hasn’t cut out. Hot and dry is actually desireable in South Texas as it proceeds to harvest. The week saw a continuation of very light-to-moderate demand in inactive-to-slow physical trading, seasonally weak (actually negative) old crop export sales, modest new crop export sales, and sub-par export shipments. U.S. squaring and boll setting progress were at or above the average pace, respectively. On the other side of the world, the Indian monsoon rains slacked off this week in the important west-central cotton growing states, in contrast to the excess rains in July.

ICE cotton futures open interest had a mixed pattern across the week. The regular Tuesday snapshot of speculative positioning (through August 2) showed continues selling with 2,236 fewer (liquidated) hedge fund longs, reinforced by 786 new outright hedge fund shorts, week over week. That is the fifth straight week of long liquidation and outright shorting by the managed money — at least through Tuesday. The index fund net long position, however, did got larger, increasing by 3,036 contracts compared to last week. So the speculative influences appear to be mixed and offsetting, based on the change in weekly numbers.

In contrast to ICE cotton, CBOT new crop corn and soybean futures, as well as KC wheat futures, all showed a longer downtrend into Thursday before partially recovering at week’s end. The U.S. dollar index showed a slight zig-zaggy uptrend.

For more details and data on Old Crop and New Crop fundamentals, plus other near term influences, follow these links (or the drop-down menus above) to those sub-pages.

Πηγή: TAMU