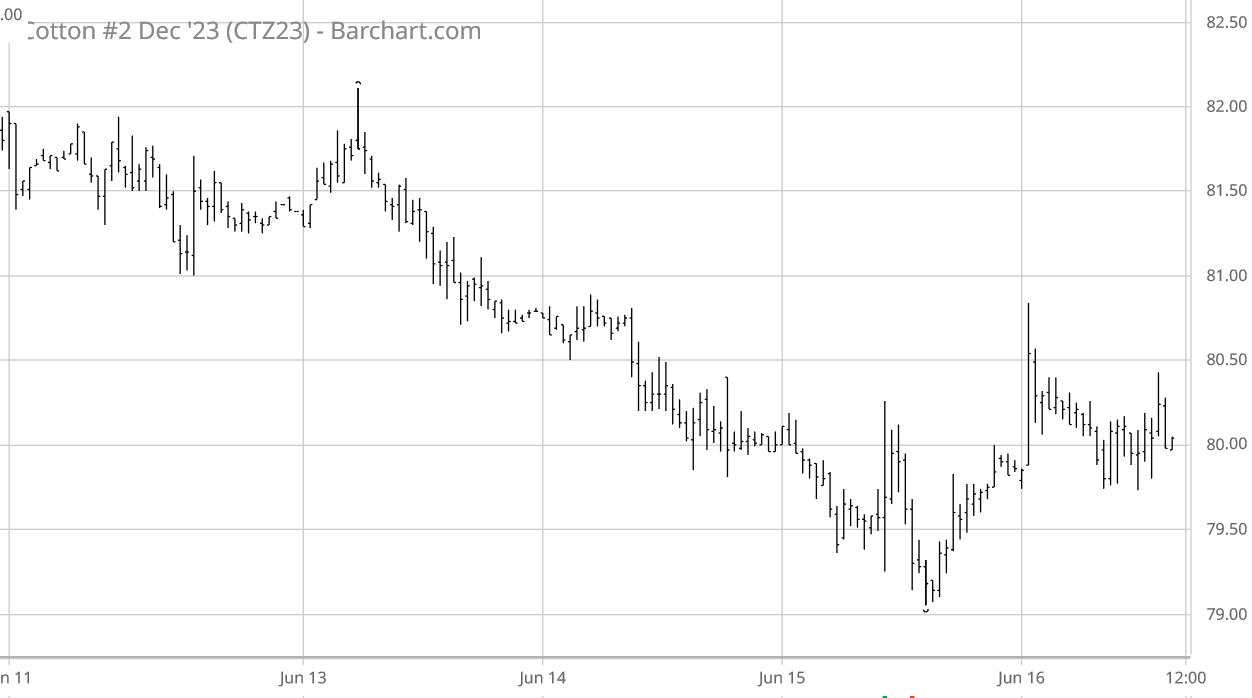

For the week ending Friday, June 16, ICE cotton futures declined steadily in a downward glide, only to do a mild touch-and-go at week’s end (see chart above courtesy of Barchart.com). In contrast, the week saw up-trends in CBOT corn, CBOT soybeans and KC wheat futures. Chinese cotton prices were mixed this week, while the A-Index of world cotton prices trended lower. The U.S. dollar index trended lower this week, perhaps giving support to crop futures other than ICE cotton.

Cotton-specific influences this week included the onset of hot weather over Texas, especially in the Gulf Coast region. The westerly parts of the northern Texas Panhandle experienced some severe hail damage. The excess rains of the preceding month have created mixed impacts on the Texas High Plains. The statewide regional summaries (click here and scroll down) reflect the transition from rainy to hot conditions. It remains to be seen how extreme heat on shallow rooted South Texas crops will impact the yield potential — yet another trade-off this season.

On the other side of the world, the southwest monsoon is still relatively late in it’s progress over the Indian subcontinent. U.S. export sales were much weaker compared to previous weeks, and actual export shipments slacked off below the needed weekly average pace. USDA’s weekly summary of the U.S. regional markets continued to reflect mixed spot physical trading activity and demand across the various U.S. regions. Macro influences (i.e., GDP, inflation, and interest rate policy) remain a potential headwind to longer term cotton demand.

ICE cotton futures open interest decreased across the week, while futures settlements declined. This has the appearance of long liquidation Indeed, the regular weekly snapshot of speculative positioning (through Tuesday, June 13) indicated long liquidation from 3,343 fewer hedge fund longs, in addition to 2,156 new hedge fund shorts, week over week. The index fund net long position through Tuesday grew by 5,412 contracts.

For more details and data on Old Crop and New Crop fundamentals, plus other near term influences, follow these links (or the drop-down menus above) to those sub-pages.