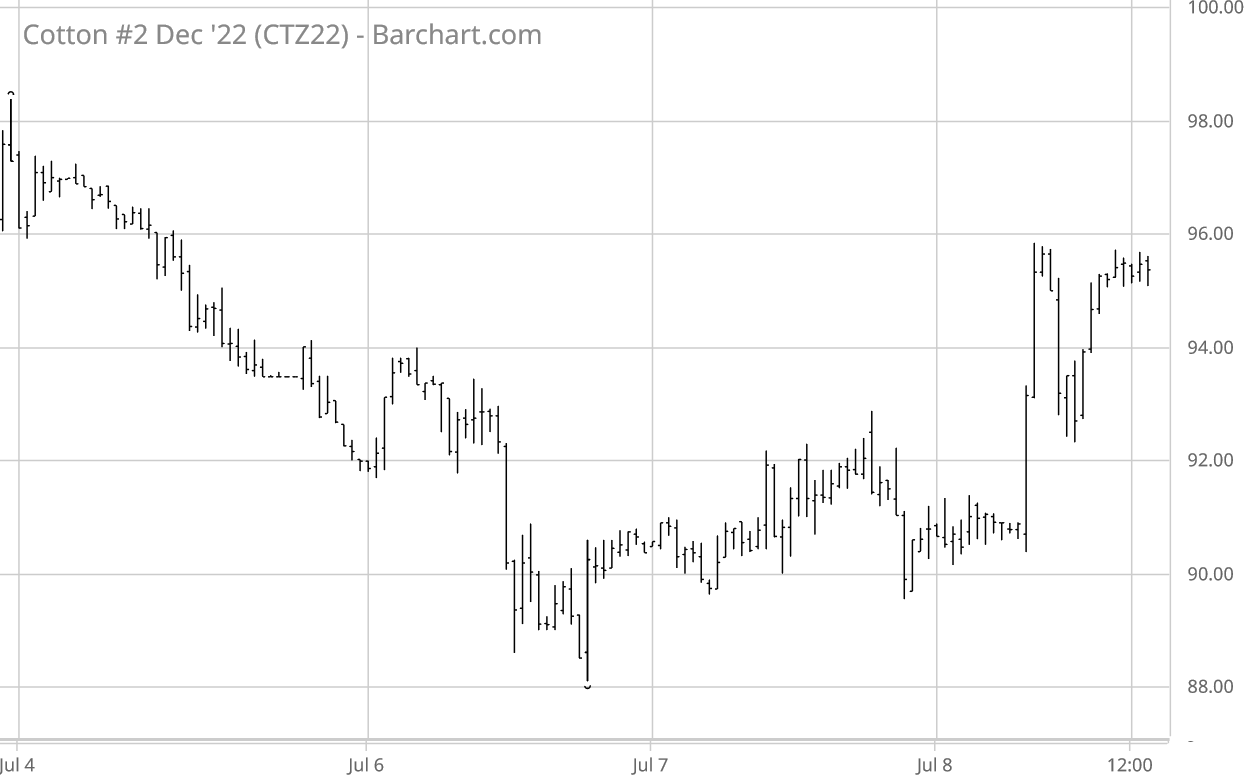

The holiday-shortened week ending Friday, July 8 saw ICE futures slip a little more from the previous week’s bottoming action, followed by a bounce and partial recovery (see chart above courtesy of Barchart.com). Chinese cotton prices and the A-index were mixed-to-lower this week.

Cotton-specific influences this week included some moisture in spots, but not enough to dent generally hot/dry conditions, The week saw a continuation of seasonally weak demand, strong new crop cotton export sales, and strong export shipments. U.S. squaring and boll setting progress was on par with recent history.

ICE cotton futures open interest was mostly declining across the week, in concert with more long liquidation (at least earlier in the week). The regular Tuesday snapshot (through July 5) showed more expected bearish positioning with 4,449 fewer (liquidated) hedge fund longs, reinforced by 4,362 new outright hedge fund shorts, week over week. The index fund longs actually increased, but only by 2,082 contracts, week over week.

CBOT new crop corn and soybean futures, as well as KC wheat futures all followed a similar fall-then-slower recovery pattern across the week as did ICE cotton futures. The U.S. dollar index climbed to 20 year highs across the week.

For more details and data on Old Crop and New Crop fundamentals, plus other near term influences, follow these links (or the drop-down menus above) to those sub-pages.

Πηγή: TAMU