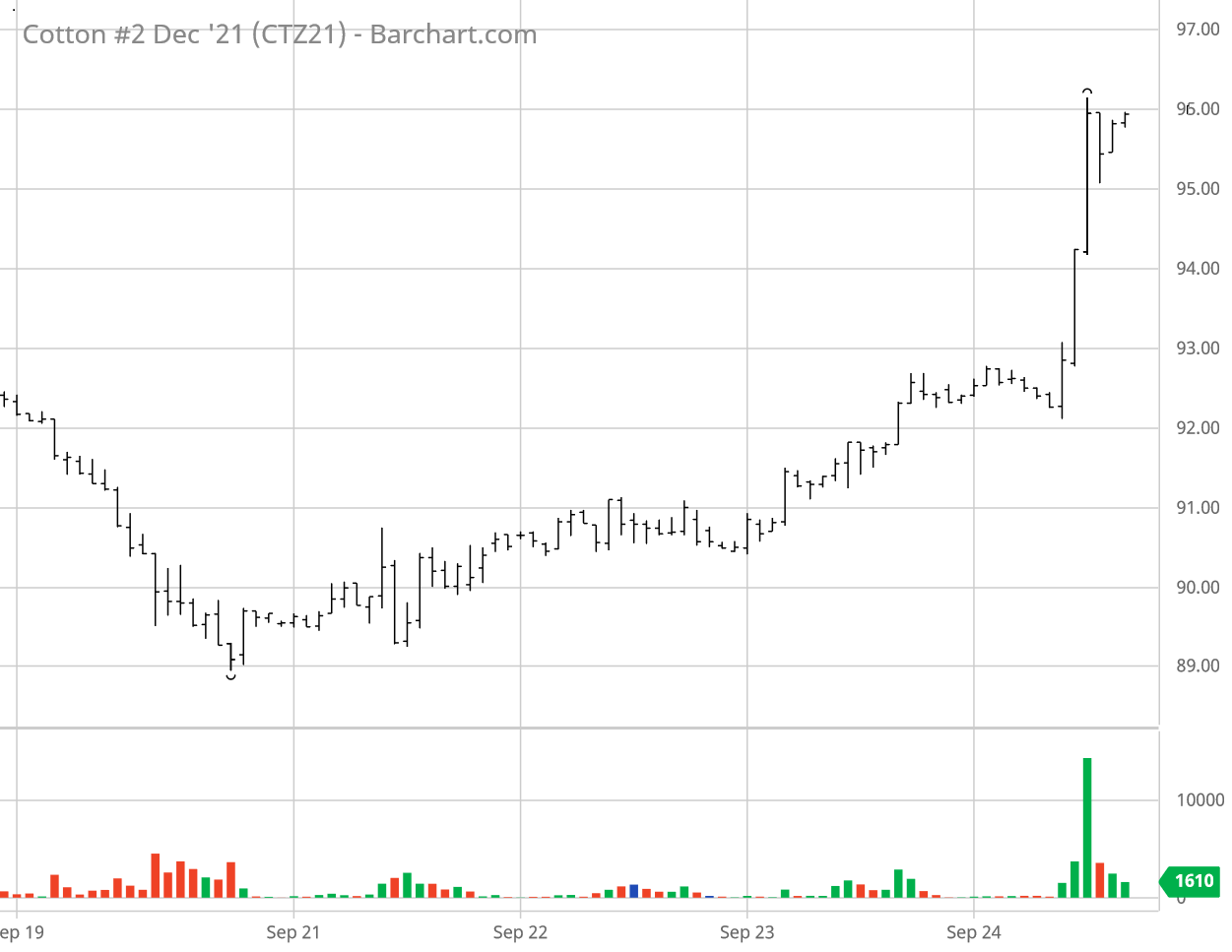

For the week ending Friday, September 24, Dec’21 ICE cotton futures took a 3+ cent dip as part of an apparent risk off market reaction on Monday. By Thursday the cotton market had appeared to make all that back, but then Friday showed some fireworks to the upside (see chart above courtesy of Barchart.com). Friday’s settlement of the Dec’21 contract was 95.99 cents per pound, up 3.53 cents on the day.

Continuing influences this week include reportedly inactive physical trading, lower post-holiday Chinese prices, mixed world prices, a sideways-gyrating U.S. dollar, “risk off” stock and commodity market selling on Monday, and then stabilization/recovery over the balance of the week. U.S. cotton certified stock levels continued to erode after peaking in late June, which is perhaps more evidence of good export demand. Cotton-specific fundamental factors this week included speculative long liquidation on Monday, strong U.S. cotton export sales in the preceding week, continuing good U.S. cotton condition ratings, good maturation weather, and perhaps a burst of mill fixations on Friday.

Open interest in ICE cotton futures declined in Monday’s sell-off and then stabilized. Indeed, the regular Tuesday snapshot (through September 21) showed long liquidation in ICE cotton futures with 10,782 fewer hedge fund longs, week over week, which was reinforced by 3,757 additional hedge fund shorts. In addition, the same CFTC report also showed 4,237 fewer index fund longs, week over week.

The movement of ICE cotton futures has implications for potential hedging strategies. The price volatility in Q1 and Q2 is a reminder why it is risky to hedge by selling futures — but it’s also made some option premiums more expensive. As new crop Jul’22 cotton futures risen in the last few months, a near-the-money 85 call option has increased in value. On September 23, a near-the-money 85 call option on July’22 settled at 9.45 cents per pound. This is pretty expensive, reflecting a whole lot of time value between now and June, 2022. Had it been purchased in the previous months, the current uptrend illustrates the insurance aspect of call options. In general, a call option represents upside price risk protection, in combination with cash contracting or selling futures. Looking further out, the rising new crop Dec’22 futures contract has resulted in an out-of-the-money 80 cent put option premium declining from fourteen cents in January to under seven cents by September 23. If Dec’22 futures keep rising, this and similar put option wills become increasing affordable down-side price insurance. That is, once purchased, it will buffer unexpected declines in Dec’22 futures by increasing in value.

For more details and data on Old Crop and New Crop fundamentals, plus other near term influences, follow these links (or the drop-down menus above) to those sub-pages.

Πηγή: tamu.edu