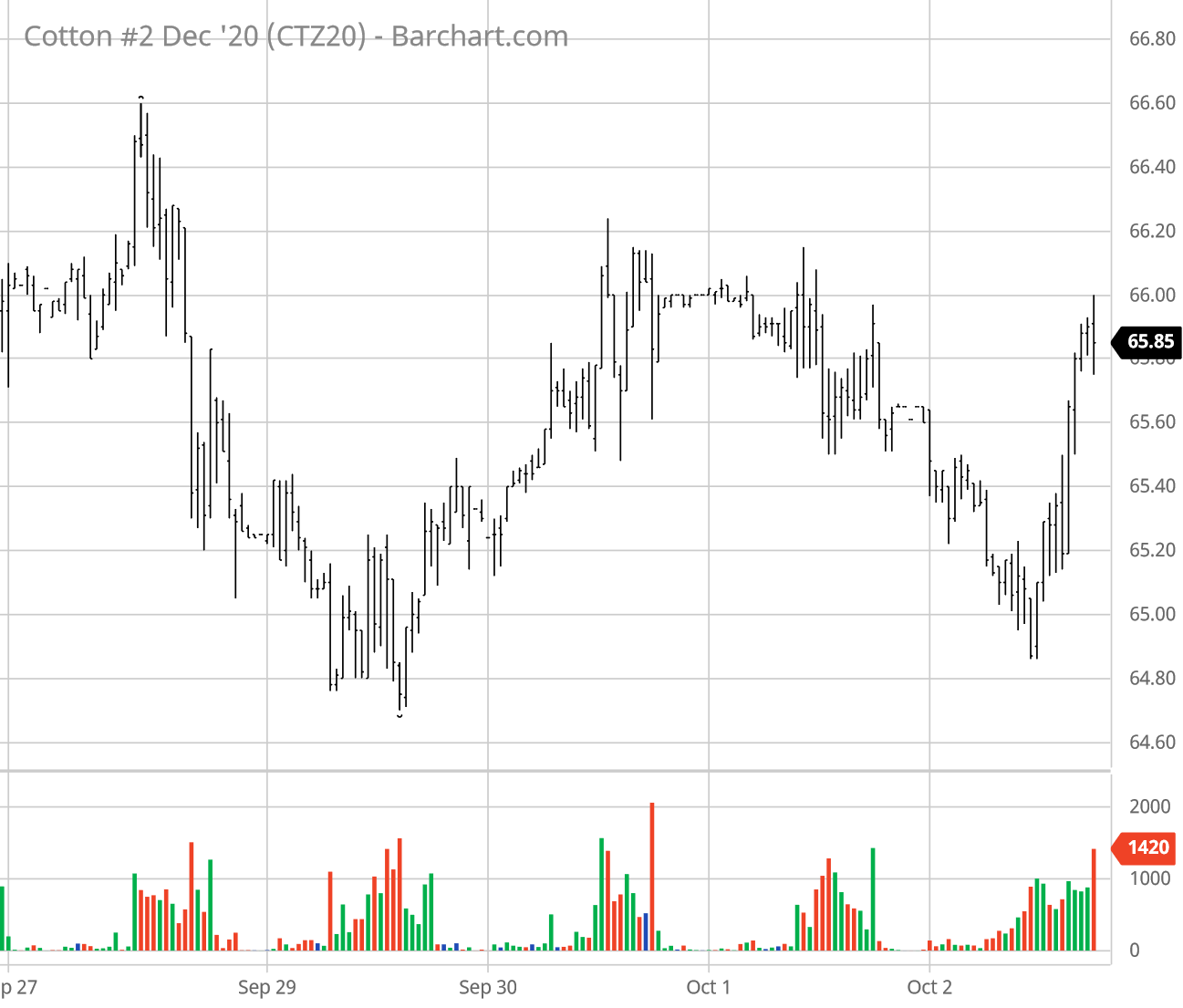

For the week ending Friday, October 2, the most active ICE Dec’20 cotton contract traded sideways in a several large gyrations (see graph above courtesy of Barchart.com). Friday’s settlement of 65.95 cents per pound was only 29 points above the previous Friday. Open interest (through October 1) followed a steadier uptrend than daily price settlements.

The September 29 snapshot of Commitment of Traders data showed modest changes week-over week. Tthe index fund net long position rose about two thousand contracts. However, the hedge fund net long position was barely changed, with only about 400 new longs and less than 50 covered shorts. The U.S. dollar slid and then bottomed out this week, generally in the opposite direction of stock markets, both being influenced by concerns about a slowing economic recovery and expanding pandemic.

Fundamental factors this week included continued recovery in weekly crop condition ratings, cooler weather across the Cotton Belt, and stronger export net sales numbers (corresponding with last week’s 65-66 cent futures range). Commercial U.S. cotton demand remains reportedly slow (see here, pp. 2-5 for an oft-repeated official statement “The COVID-19 Pandemic continues to negatively affect cotton demand and disrupt supply chains.”). Certified stocks continued to recover. Chinese and world cotton prices were mixed through September 24.

In my opinion, the cotton market can’t avoid the long term bearish implications of USDA’s 2020/21 balance sheet. The longer term damage to cotton consumption by the COVOD-19 pandemic will surely take many months to resolve. In the near term, ICE cotton futures keep bouncing off the 65-66 level, on remaining production uncertainty, Chinese state buying, and unprecedented money flows in the financial sector, created by the Federal Reserve. There is also the possibility of commercial buying from Chinese mills in response to 1) newly available import quota, and 2) potential impacts from sanctioning cotton exports from Xinjiang. But all that remains to be seen.

I think that the normalization of cotton’s global supply chain and consumers’ willingness to buy more apparel may take a while. Hence a return to profitable market price levels may not happen during 2020. (I do see the possibility of higher prices for the ’21 crop, but partly for bad reasons like La Niña drought.)

From a marketing standpoint, both old crop and new crop cotton prices remain at the low level of the federal program price support. In government-speak, the adjusted world price (AWP) remains below the 52-cent loan rate. This makes for positive loan deficiency payment (LDP) rates for those who sell their cotton in the cash market (being careful to maintain beneficial interest).