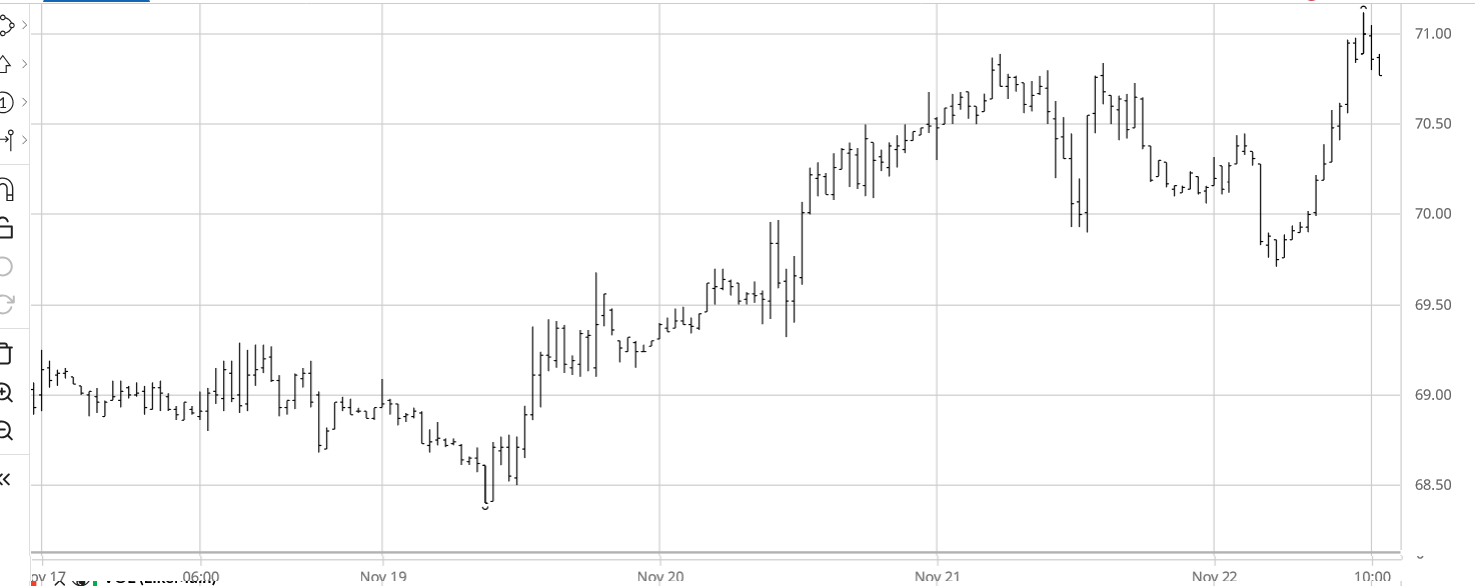

For the week ending Friday, November 22, the most-active Mar’25 ICE cotton futures contract stabilized from the previous week’s decline, then modestly trended up back over 70 cents to flirt with the 71 level (see chart above courtesy of Barchart.com). The Mar’25 settled Friday at 70.77 cents per pound, while the new crop Dec’25 settled the week at 71.71 cents per pound. Chinese cotton prices followed a flat/static day-to-day pattern across the week, as did the A-Index of world cotton prices.

In other markets, nearby CBOT corn and KC wheat futures gyrated in a sideways pattern across the week while CBOT soybean futures had more of a down-trend. U.S. dollar index traded flat before ending the week in a modest up-trend. Other macro influences (i.e., GDP, inflation, and interest rate policy) were typically mixed in their implication.

Cotton-specific influences this week included a relative boom in weekly U.S. export sales. The pace of 2024/25 export shipments remained below the needed weekly average pace to reach USDA’s target level of exports, though this is not unusual for this supply-dominated time of the year. In terms of weather, this week saw continued rainy harvest weather over the central and eastern portions of the Cotton Belt. The latter mainly has implications for quality (e.g., poorer color grades, more bark, etc.) and discounted cash prices.

For the week ending November 21, the day-to-day shifts in open interest in ICE cotton decreased. Together with the modestly rising price settlements across the week, this pattern had the appearance of some short covering. However, as of Tuesday, November 19 (released Friday, November 22) the weekly snapshot of speculative positioning showed bearish adjustments with 3,830 fewer (liquidated) hedge fund longs and a 4,260 contraction in the index fund net long position. This was further reinforced by 13,027 additional hedge fund shorts, week over week.

For more details and data on Old Crop and New Crop fundamentals, plus other near term influences, follow these links (or the drop-down menus above) to those sub-pages.

Πηγή: TAMU