John Robinson, Extension economist, cotton marketing, Texas AgriLife Extension

USDA’s month-over-month adjustments in August’s World Agricultural Supply and Demand Estimates reflected much tighter adjustments to the 2025-26 world cotton balance sheet.

Supply side adjustments included 1.73 million fewer bales of beginning stocks, mainly in Brazil, China and the U.S., compared to July. World production was lowered by 1.8 million bales, month over month, 77% of which was in the U.S. World imports were down 1.1 million bales from the previous month. Altogether, the world supply was reduced 4.63 million bales, which is a large adjustment.

On the demand side, world consumption was trimmed only 130,000 bales compared to July, mostly in Turkey and India (offset by an increase in China). World exports were cut 1.1 million bales to match the cut in world imports. The supply-side cuts dominated those on the demand side, so the bottom line was a historically large 3.41 million-bale cut in world ending stocks, month over month. Such an adjustment would normally be price supportive according to economic theory and history.

Updated U.S. supply and demand

The August WASDE report also included very bullish supply-side adjustments to the U.S. new-crop balance sheet, compared to the previous month’s numbers. To begin with, U.S. beginning stocks were cut 100,000 bales, month over month. The combination of lowering U.S. planted acreage (down 840,000 acres) and raising abandonment (up 3.5%) combined to cut harvested acres by 1.3 million. Even with an increase in yield at 53 pounds per harvested acre, resulting U.S. production was reduced by1.4 million bales to 13.21 million bales.

On the demand side, U.S. exports were cut a half-million bales to account for the reduced supply. The bottom line of this was a 1 million-bale reduction in U.S. ending stocks to 3.6 million, which is an historically bullish adjustment as well as a price supporting level.

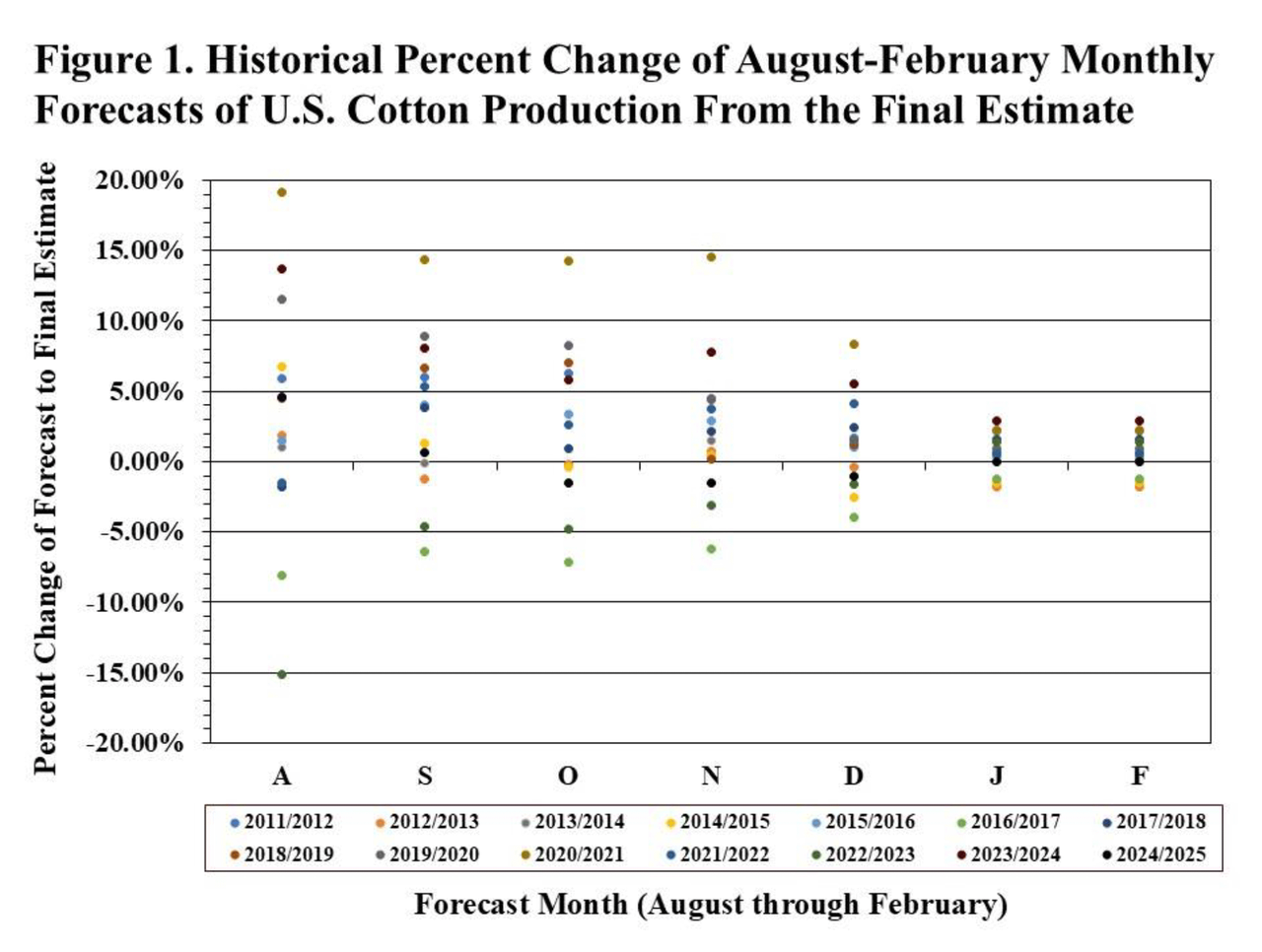

Of course, the August forecast of U.S. production has a lot of time to be adjusted. Figure 1 shows that, historically, the August forecast can vary up to 15% from the final number. As USDA collects more survey data, as well as forecasts of ginned bales and counts of classed bales, this information will refine the forecast over the successive months.

For additional thoughts on these and other cotton marketing topics, visit my weekly online newsletter at cottonmarketing.tamu.edu.

For additional thoughts on these and other cotton marketing topics, visit my weekly online newsletter at cottonmarketing.tamu.edu.

Robinson is an ag economist for cotton at Texas AgriLife Extension.

Πηγή: farmprogress.com