Cotton futures prices peaked in early May at around 95 cents per lb, the highest level for over two years. Since then cotton futures have declined by 10 cents per lb as heavy rainfall in west Texas around Lubbock (the area typically produces a fifth of the US cotton crop) led traders to anticipate a larger harvest. According to the USDA 36% of Texas’s cotton fields have been planted, the rainfall allowing farmers to plant more cotton seeds and helping those seeds already sown to survive. The rain is especially welcome after recent harvests have been buffeted by drought. Meanwhile increased demand from China, the top cotton consumer and the US, the largest apparel market means that supplies could hit a 23 year low later in the summer, according to projections from the USDA.

The prospect of El Niño appearing later this year (the chances of it appearing put at 70% by some meteorologists) could disrupt cotton prices. The potential effects of El Niño rainfall patterns on global cotton production range from drier weather in Australia and central India and wetter weather for the US Cotton Belt. According to Societe Generale cotton prices have often jumped by more than 60% in previous episodes. Although the central issue for the US and the effect on the cotton market would be the timing of El Niño it could be even more influential if it comes early enough to result in weak monsoon rains over India. India plants a lot more cotton than the US and variable rainfall there can cause swings in production causing large price movements.

Another factor that has been weighing on the market is fears over an impending release from ChinaΆs cotton reserves. Some estimates suggest that as much as three million tonnes, or almost 30% of ChinaΆs strategic stockpile of cotton could be released during the 2014/15 season beginning 1 August. These fears might be overblown however after recent data showed that China had recently placed a large order of US cotton, the USDA having to play catch up in its estimate of how much China is likely to import this season.

Although demand for cotton is strong it is increasingly competing with polyester for market share among textile and clothing manufacturers. When cotton futures soared to over 200 cents per lb in early 2011 many manufacturers switched to cotton/polyester blends. With cotton now less than half that value there has been little sign that cotton consumption bouncing back. Indeed, with polyester at around 65 cents per lb in Chinaand consumers increasingly content with cotton/polyester blends many in the market appear pessimistic that the market will return to pre-2011 consumption levels of demand.

Meanwhile, cotton merchants are waiting months to take delivery of cotton from US warehouses, tightening supplies according to reports in Reuters . Some warehouse operators have sought to release stock at the slowest possible rate when demanded in order to cash in on storage fees. In times of high demand and low supplies, like now, those rates can be too long to meet the just-in-time demands of mill who carry minimal stocks. According to Reuters major cotton users are hunkering down until next season, when fresh supplies will arrive on the market.

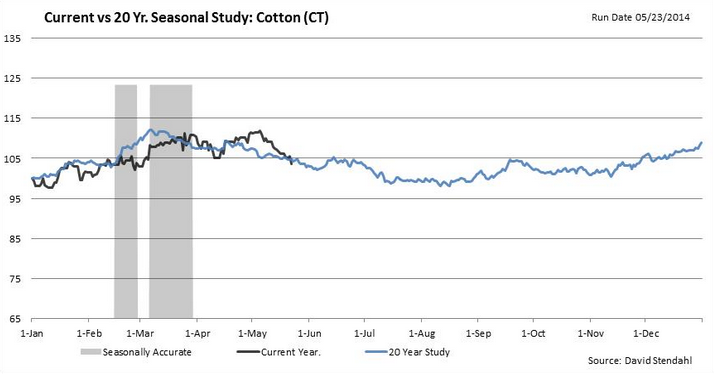

Cotton futures prices have followed seasonal price trends closely so far in 2014. Based on data from the last 30 years cotton prices could well continue to fall, perhaps bottoming out in July/August. Cotton prices tend to peak in the spring just as planting takes place and the risk of weather damage is greatest and then reach a trough between July and September as the crop is harvested. As in previous years the risks focus on the weather (particularly the likelihood of drought in the US, but also rainfall and flooding in India and Australia) and ChinaΆs policy towards its cotton reserve and nearer term purchases may divert prices from seasonal trends.